Fresh four-year highs in monthly US building permits and housing starts at 894K and 872K respectively, are consistent with the 43% and 36% increase in US existing home sales and new home sales from their respective 2010 lows.

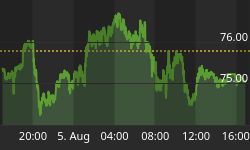

"Good" US data no longer disappoints markets on the fear of discontinuing QE due to the Fed's insistence to target further declines in unemployment (towards 7%) regardless of the trend in non-inflation macro data. The seemingly win-win reaction function between data releases and market performance works in providing buying on-the-dips at key support levels (illustrated below) as well as the testing and eventual breach of this year's highs.

Cross-market correlations continue to take precedence over individual fundamental factors in the functioning of equity, currency and commodity markets. The risk-on/risk-off dynamics, whereby risk currencies (ex-USD & ex-JPY) move in tandem with equity indices and most commodities, are most accentuated when event-risk is either omni-present (looming credit downgrade, eurozone bailout, central bank decision), or thoroughly out of the headline (Draghi's OMT & Fed's QE3 announcement).

A most recent example of the aforementioned correlations is the synchronized pullbacks and rebounds along the June trendline support in equity indices, individual shares, energy and metals.

Determining the causality, or the independent variable initiating the moves is usually the most challenging part of applying Intermarket dynamics, but the recurrent support levels in large/liquid markets such as EUR/USD (24% of +$5trillion /day FX market) and the S&P500 (followed by over $1 trillion in benchmark funds) can be used as a leading signal to help confirm moves or warn of false turns in other markets.

Our positive stance on overall risk appetite throughout the second half of Q3 and the insistence for EUR/USD to visit $1.35 before $1.25 and (and last month on here) for US crude to retest $96.00/barrel before $85.00/barrel is integral to the aforementioned set-up. Falling volatility in the VIX and EUR/USD one-month option volatility is fundamentally backed by traders' unwillingness to buy volatility ahead of a looming policy freight train from the ECB and the Fed's open-ended QE.

For tradable ideas on FX, gold, silver, oil & equity indices get your free 1-week trial to our Premium Intermarket Insights here

Follow us on Twitter @Alaidi