| Current Level | 5 Days | 1 Year | 5 Year | |

| Gold | 424.30 | -0.5% | 6.3% | 50.8% |

| Silver | 7.00 | -2.0% | 0.1% | 36.7% |

| S&P | 1,142.62 | -3.3% | 1.2% | -23.9% |

| ISEQ | 6,081.39 | -1.1% | 12.5% | 13.2% |

| FTSE | 4,891.60 | -1.8% | 8.3% | -23.3% |

| EUR/USD | 0.78 | 0.9% | -6.6% | -25.2% |

| OIL | 50.49 | -5.3% | 34.4% | 109.2% |

Weekly Markets

Precious Metals

The precious metals were mixed if largely unchanged for the week.

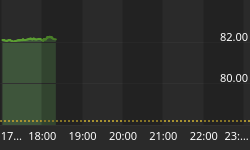

Gold was down 0.5% for the week: It was down $2.20 from $426.50 to $424.30.

Silver was down 1.9% for the week giving up much of last week's 2.44% increase: Silver was down from $7.14 per ounce to $7.00 even.

Platinum (July) was up 0.5% for the week at $866.0 per ounce.

Palladium (June) was up 0.3% closing at $199.55 per ounce.

Many analysts were surprised by the precious metals lack of upward movement given the significant declines in the equity and bond markets due to the poor retail, consumer confidence, inflation and trade deficit figures. "It does start to question the longer-term health of the US economy," said James Moore, analyst at TheBullionDesk.com. Moore added that gold's status as an inflation hedge "suggests 500 US$ an ounce is still an attainable target this year."

The precious metals seem to be continuing the process of consolidation and have been in a tight range for some time. Goldseek.com pointed out how gold's closing prices the past 4 Friday's were March 24 - $424, April 1 - $425.30, April 8 - $426.50, April 15 - $424.30. Normally such a lack of volatility portends a large move to the up or down side.

Gold's 50 day moving average is at $429.88 and a convincing close above that number may lead to a rechallenge of it's recent 17 year highs at $455.

Gold's has support at it's 200 day moving average at $421.75 and strong support at $410.

Once again investing guru Dennis Gartman, author of 'The Gartman Letter' and frequent contributor on CNBC, has nailed his colours to the mast regarding his belief that gold is now in a long term bull market in all currencies. This is significant as Gartman is no 'goldbug'. In fact he is the darling of Wall Street and is highly respected and followed by large hedge funds and financial institutions.

He had this to say regarding gold's attractiveness to investors globally but especially to American and European investors: "With each passing day, given the problems incumbent in the EUR as Europe moves toward the constitutional referenda in the Netherlands and France, we can make the stronger, and ever stronger, case that Gold/EUR shall move higher even as the dollar itself gains relative to the EUR. Gold shall become a more "reservable" asset as central banks who might have been interested in diversifying their assets away from the dollar now find the EUR less and less attractive, and find gold somewhat more so."

Gartman argues that gold will benefit from the flaws inherent in the Euro and other fiat paper currencies. He believes that the EUR is suspect as a currency given the abrogation of the 'Stability Act' and the unlikelihood of an EU Constitution being ratified. While Gartman believes that the trade deficits will not impact the dollar negatively, one would think that the US$ may remain under pressure due not solely to the trade deficits but rather due to the massive and unprecedented Triple Deficits - the trade, budget and current account deficits, especially in an inflationary and rising interest rate environment.

Gartman's case against the Euro is summed up in an article entitled 'French No could trigger euro chaos' in the anti-EU British Daily Telegraph. It is important as it reflects a broad strand of opinion on Wall Street and in wider financial circles and has important ramifications regarding lack of confidence in all faith based paper fiat currencies going forward. Gartman and many on Wall Street believe that this lack of faith in the Euro and some other government printed, debt based currencies will leave gold as the single remaining international currency.

Adam Hamilton of Zeal Intelligence believes the recent correction in the gold bull market is now over and gold will soon rally dramatically based on the historical record and short term negative sentiment for gold due to the recent correction. This is particularly the case because of the Gold Futures Commitment of Traders report which shows 'longs' fearful recently and a lot of liquidation. From a contrarian viewpoint this may mean the recent pullback and consolidation are ending.

Also bullish for gold is the fact that the often trumpeted but never happening IMF gold sales were officially ruled out at the G7 meetings this weekend. John Snow, the US Treasury Secretary told the IMF policy committee on Saturday selling gold stocks to pay for debt relief was the wrong approach. He was echoed by the Canadian Finance Minister Ralph Goodale who told Reuters "So whatever the merit of the argument might be, it's not going to pass."

This comes in the wake of blunt statements by the Chairman of the bipartisan US Joint Economic Commitee, Rep. Jim Saxton, R- N.J., that the mooted IMF gold sales would be stopped by both the US Congress and George Bush.

The gold sales proposal, like most reporting on gold and the precious metal markets in general, is one of the most poorly reported and thus not understood stories in the financial world today. Much of the world's and in particular the British financial press portrayed the situation as 'bad' America not helping the Third World again. The Guardian in Britain was at the vanguard of this hypocritical claptrap continually attempting to portray Mr Brown and Mr Blair as valiant anti-poverty crusaders battling against the bad greedy Americans on behalf of the Third World. While the US did oppose the gold sales and for sound economic reasons it was barely reported that ECB chief Jean Claude Trichet also came out on behalf of the ECB as against the gold sales. The German Central Bank agreed with the ECB chief. The Bundesbank said it is firmly opposed to the idea that the International Monetary Fund sell some of its gold reserves to finance debt relief.

(More on 'The IMF, Gold Bullion Reserve Sales and the Developing World' in our Weekly Commentary section)

Oil

Oil was down by 5.31% or $2.83 to $50.49 for the week continuing it's recent decline. The decline came ahead of this weekend's G7 meeting that will be discussing the economic impacts of high energy prices.

Finance chiefs of the G7 nations are resigned to future high oil prices saying that the world must adjust to consistently higher cost of energy, reported Reuters. Officials regard costly oil as one of the biggest risks to global economic growth. But US Treasury Secretary John Snow said that the G7 are preparing for an era of more costly energy and could handle recent rises that topped $58 per barrel.

At a press conference following a meeting of group of Seven finance chiefs, Snow aimed to put the best face on an outlook the G7 agreed was buffeted by a "headwind" from costlier oil. Snow's Treasury officials reiterated: "Even with the drag, the sense is the global economy will continue to grow at a strong clip."

Reuters reported how expectations that oil may remain above $50 per barrel this year are increasing the perceived risks of "stagflation," a combination of high inflation and economic recession, some analysts say. Few forecast a return to the acute economic pain of the 1970s. But with crude oil prices still above $50, more analysts are seeing symptoms and warning that even a mild case of stagflation could be painful. For 2005, the average world oil price will be about $52.23 a barrel, IMF analysts forecast earlier this month. On Friday, crude oil was trading around $50.15 per barrel in New York, while U.S. stocks were around five-month lows.

The recent deterioration in relations between the two Asian behemoths, Japan and China continued. They are now disputing each other's claims over possible new oil sources in the East China Sea as competition for energy supplies mounts. The rising oil prices and increased global demand is increasing geopolitical tensions globally. These energy tensions add to the already tense relations between the countries due to the Chinese accusing the Japanese government of historical revisionism in belittling, censoring by omission and covering up the Japanese brutal torture, rape and killing of civilians in China and throughout Asia, including the 1937 Nanjing Massacre of 300,000 unarmed men, women and children.

The Chinese are also opposed to Japan being granted a seat on any reformed UN Security Council. This does not bode well for global trade and as Stephen Roach of Morgan Stanley has warned may lead to protectionist measures which when begun have a habit of escalating into damaging tit for tat retaliations.

Contrary to misguided reporting regarding a slowdown in the Chinese economy reducing demand for oil and other commodities, the International Energy Agency said that "China's oil demand is estimated at 6.88 mln barrels per day (bpd) in 2005, up 7.9 pct over 2004."

China may have experienced a very slight slowdown recently but this will result in phenomenal GDP growth of some 8% down from the IMF's estimate of 9.5% growth in 2004. Most economists also believe that China is capable at growing at on average 8% per annum until 2010.

This is hardly a recipe for a significant reduction in demand sufficient to derail the nascent bull markets in oil, precious metals and commodities in general due to the gradual emergence of affluent middle classes in China, India and throughout Asia.

Other Commodities

Reuters Commodities Research Bureau's Index fell by 1.8% to 298.83. The CRB's year to date gains are 5.2%. Since hitting a low of 182.83 in October 2001 it is up nearly 70%.

The Reuters CRB Index ( the 17 basic components include hard tangible assets such as Metals, Textiles and Fibers, Livestock and Products, Fats and Oils, Raw Industrials, Foodstuffs). One of the CRB index's greatest strengths is the fact that there is an equal weighting of all of its 17 components. This weighting assures that no price increase in any single commodity, like oil, can significantly skew the entire index. Significant moves in the CRB are only possible when the majority of its component commodities are moving in unison with a particular primary trend. Oil, silver and gold only account for 3/17th of the entire index.

The Goldman Sachs Commodities Index dropped 2.2%. The GSCI is a world production-weighted commodity index which next year will be composed of 24 liquid exchange traded futures contracts. The GSCI includes energy, industrial metals, precious metals, agricultural and livestock products. It is up 16.3% year to date.

Doug Noland of Prudent Bear Mutual Funds in the Commodities Watch section of his 'Credit Bubble Bulletin' highlighted the following important commodity stories.

April 14 - Bloomberg (Claire Leow and Grace Nirang): "Indonesia, Southeast Asia's only OPEC member, may become a net oil importer this year as projects led by ConocoPhillips, Unocal Corp. and PetroChina Co. fail to stem falling output, helping to boost fuel prices to records. The country may turn to importing a net 61,000 barrels a day this year from net exports of 27,000 barrels a day in 2004."

April 11 - Bloomberg (Xiao Yu and Helen Yuan): "China's steel imports may rise 15 percent this year to 240 million metric tons to feed expansion by Chinese steelmakers, said Qi Xiangdong, deputy secretary general of the China Iron and Steel Industry Association."

April 13 - Bloomberg (Christopher Donville and Darrell Hassler): "China, the world's second-biggest consumer of aluminum, may become a net importer of the metal this year because of increasing demand and limited ability to produce more, Alcan Inc. Chief Executive Travis Engen said."

April 12 - Bloomberg (Cherian Thomas): "India's industrial production had its smallest gain in almost two years in February as exports slowed and a shortage of coal curbed steel and energy output. Output at factories, utilities and mines rose 4.9 percent from a year earlier compared with growth of 7.5 percent in January."

April 15 - Bloomberg (Anand Krishnamoorthy): "India's automobile sales rose 14 percent in March after Hero Honda Motors Ltd., the nation's biggest motorcycle maker, and Maruti Udyog Ltd., the biggest carmaker, boosted sales."

Currencies

The U.S. dollar index was marginally higher by 0.05 points on the week to 84.50 showing surprising strength in the face of poor economic news.

It fell from a 2 month highs as it lost 0.52 points to 84.50 on Friday.

The euro index rebounded from 2 month lows as it gained 1.04 points to 129.12 on Friday, but is still down by 0.07 points on the week. The yen gained 0.50 points to 92.85 on Friday and is higher by 0.58 points on the week.

The British pound was up slightly against the greenback. On the downside, the South African rand and Iceland krona declined about 2%, the Chilean peso 1.7%, and the Polish zloty 1.6%.

The U.S. currency slipped against the euro after weaker-than-expected retail sales data on Wednesday but soon rebounded, as it did on Tuesday after the U.S. trade deficit hit a new monthly record.

"We've had two bad U.S. numbers in the past two days and euro has plummeted after both of them," said Lee Ferridge, senior proprietary trader at Rabobank. "The market is worried that there are big sellers out there that you can't explain and people are reluctant to be long on the dollar given the speed of the moves in the past few days -- and you can't blame them," he added.

"Our view is that the dollar's rally has been driven by speculative investors buying back short dollar positions, not real money flows," said Ryan Shea, market strategist at State Street. He said disappointing corporate results and falling Treasury yields reflected market unease over U.S. growth prospects, and did not expect the dollar to remain strong for long. Barclays Capital agreed: "A second consecutive close-to-close decline of more than one percent by U.S. equities raises a warning flag that recent dollar strengthening may be nearing its peak," it said in a research report.

Bonds

The 10-Year Treasury note yield made traded lower all day Friday and made a new 7 week low as it lost 0.087 points to 4.271% as the June 2005 US Treasury bond rallied on poor economic prospects and gained 1 1/32 to 113 18/32. For the week, the yield is lower by 0.45% and the bond is higher by 2.19%.

Two-year Treasury yields ended the week down 24 basis points to 3.49%. Five-year government yields declined 27 basis points to 3.87% and long-bond yields dropped 17 basis points to 4.59%.

General Motors Corp. bonds in euros plunged in London trading. The extra yield, or spread, over government debt of similar maturity that investors require to hold GM's 5 3/8 percent bond maturing in June 2011 widened to 7.99 percentage points from 6.02 percentage points yesterday, according to Merrill Lynch prices ... The yield ... soared to 11.05 percent from 9.13 percent.

Business Week reported how Ford, GM bonds flirt with junk status. Should this happen it will likely raise the cost of borrowing to corporations globally. The FT reported how GM downgrades spark rise in credit derivative trading.

Stocks

The Dow Jones Industrial Average was down 3.6% for the week: From 10,461.40 to 10087.51.

The S&P 500 Index, of more significance than the DOW, was down 3.27%: From 1,181.20 to 1,142.62.

The Nasdaq composite was down 4.56% for the week: From 1999.35 to 1908.15

The major indices were all down significantly for the week and are now at 5 month lows. Friday's decline in the DOW of 191 points was it's largest drop 1 day since March 2003. The DOW was down nearly 400 points for the week and it was the first time it had posted triple-digit declines for three consecutive sessions running since January 2003.

This was due to an increasing belief amongst many that the US economy, the world's largest economy is beginning to slowdown with the affect that this will have on the US consumer and corporate earnings going forward. The market may have paid heed to warnings from the OECD, IMF and World Bank regarding the health of the US economy and the retail sales, inflation, consumer confidence and the trade deficit figures which were all far worse than expected.

The declines for the week happened on heavy volume which is of importance and may indicate a significant change in trend and reassertion of the primary trend since 1999 which as can be seen from the long term chart of the DOW is down. This long term trend will remain in place unless the DOW closes above it's highs of 11,722 on January 14 of 2000. This bull market advance greatly exceeded that experienced in the great bull market of the 1920's.

The long term chart shows the extraordinary and unprecedented surge in the DOW in the late 1990's. From 1995 to 1999 the DOW surged relentlessly from 4,000 to over 11,000. This is nearly a 200% return in just 4 years. Various studies have shown that long term returns from stock markets have averaged between 7 and 10% depending on a variety of factors considered.

Factored into these average returns must be brokerage fees and the ravages of inflation. Also, to get to that average you have to look at nearly a century of stock market performance, and over such a long period of time it is easy to overlook long stretches of losing performance by the stock market for anywhere from 15 - 24 years.

Investing is about evaluating risk over the long term and some investment experts predict long-term returns from the stock market will be worse during the next 30 years due to a wide range of issues including the so called pensions timebomb and demographic factors.

The Transports plunged 6%despite the recent decline of oil prices.

The more defensive Utilities were down 1%.

The Morgan Stanley Consumer index was down about 1%.

The Morgan Stanley Cyclical index was down 7%.

The small cap Russell 2000 and S&P400 Mid-cap indices were down 5% and 4% respectively.

The NASDAQ100 was down 4% and the Morgan Stanley High Tech index was down 6%.

The Semiconductors were down 8%.

The Street.com Internet Index and NASDAQ Telecommunications indices were down 5% and 4% respectively.

The Broker/Dealers were down 4% and the Banks were down 2%.

Biotechs have been very volatile of late but one of the bright spots of the week being up 1.%.

It was the third straight triple-digit decline, which last occurred in January 2003. The sell-off was blamed on increasing worries that the US economy - the locomotive for the global economy - could hit a "soft patch" worse than the slowdown of last spring and summer, which followed spikes in gasoline and energy prices.

Senior U.S. Treasury officials said later that the global economy has enjoyed a "sweet spot" for the past few years -- with steady growth, low inflation and relatively stable energy prices -- and that now the big industrial economies must take steps to preserve growth. "Good times don't last forever," the officials said.

IBM was down more than 8% on Friday alone and is down a massive 10 days in a row.

The world's largest computer company, issued a nasty surprise to investors last night, saying profits and revenues were considerably below expectations in the first quarter due to sluggish sales.

Bringing out its results after New York's stock market closed, and two days ahead of schedule, IBM reported a profit from continuing operations of $1.41bn (£750m), or 85 cents a share, compared with $1.36bn, or 79 cents a share, a year earlier. Analysts had expected profits of 90 cents a share.

Sam Palmisano, the chairman and chief executive of IBM, which is nicknamed Big Blue, said: "After a strong start, we had difficulty closing transactions in the final weeks of the quarter, especially in countries with soft economic conditions."

Hit by low-cost computer manufacturers in Asia, IBM has agreed to sell its laptop business to China's Lenovo. Analysts said sales of IBM's ThinkPads probably fell ahead of that sale.

The Washington Post reported how GM Woes Drag Down Markets. This drag was not confined to US markets. As an indication of the importance of GM to markets globally AE Brazil reported how Brazilian markets were affected by talk of GM being reduced to junk bond status and going bankrupt - Brazil stocks fall as global factors cast long shadow.

GM's continued and there was even talk of bankruptcy as reported by New Ratings: General Motors 10bp Wider On Chapter 11 Talk.

Commentary

The IMF, Bono, Brown and the Developing World

The often and continually trumpeted but never happening IMF gold sales were officially ruled out at the G7 meetings this weekend. John Snow, the US Treasury Secretary told the IMF policy committee on Saturday selling gold stocks to pay for debt relief was the wrong approach. He was echoed by the Canadian Finance Minister Ralph Goodale who bluntly told Reuters that "it's not going to pass." "It's not just going to fly with enough countries" and "does not have a snowball's chance of passing the IMF management committee."

Canada has been among gold-producing nations that have argued against the proposal, in part because they fear it would depress markets and prices for the precious metals. Goodale says Canada has shown the way for other wealthy nations to simply forgive debt and debt-service costs for poor countries, rather than fooling around with gold sales.

"It's not going to work, we're investigated it ... look folks, belly up to the bar, assume your responsibilities and let's eliminate that debt servicing charge and not use the gold as an excuse for doing nothing," said Goodale. "Gold is not the issue. Debt is the issue." said Goodale. Thank goodness for his lack of forked tongue speak, candour and honesty on this issue.

This comes in the wake of equally blunt statements by the Chairman of the bipartisan US Joint Economic Commitee, Rep. Jim Saxton, R- N.J., that the mooted IMF gold sales would be stopped by both the US Congress and George Bush.

Congressional approval would be required for the sales of IMF's member countries bullion reserves or assets. JEC Chairman Rep. Jim Saxton, R-N.J., said he favors IMF debt relief through write-offs financed out of the IMF's other resources. "The potential profits on IMF gold sales rightfully belong to the original donor countries and their taxpayers," he said. "These IMF gold sales would amount to a hidden appropriation from the donor countries that were the original source of the gold." Saxton said the IMF failed to implement the proper lending safeguards and accounting controls for making such loans. "Not surprisingly, some of its loans have gone bad, and the consequences should not be papered over," he said. "The IMF's mistaken forays into development lending have proven counterproductive, and should not be repeated." Brown's proposal which was claimed to be in order to aid debt forgiveness in the Third World would require an 85% majority to pass. The U.S. has veto power as they hold more than a 15% vote.

The gold sales proposal, like most reporting on gold and the precious metal markets in general, is one of the most poorly reported and thus not understood stories in the financial world today. Much of the world's and in particular the British financial press portrayed the situation as 'bad' America not helping the Third World again. The Guardian in Britain was at the vanguard of this hypocritical claptrap continually attempting to portray Mr Brown and Mr Blair as valiant anti-poverty crusaders battling against the bad greedy Americans on behalf of the Third World.

While the US did oppose the gold sales and for sound economic reasons it was barely reported that ECB chief Jean Claude Trichet also came out on behalf of the ECB as against the gold sales. The German Central Bank agreed with the ECB chief. The Bundesbank said it is firmly opposed to the idea that the International Monetary Fund sell some of its gold reserves to finance debt relief.

Trichet said there was no agreement within the IMF on the proposal by UK Chancellor of the Exchequer Gordon Brown to use its gold to write off debt, and the ECB would urge caution. "As regards our own position, we would certainly be cautious in this respect," he told reporters at the ECB's monthly press conference. "As central banks we say that development assistance should normally be financed through budgetary resources ... rather than through the use of monetary assets," Trichet said. Trichet said if the IMF did sell gold, the proceeds might be better used to shore up its own finances given the bad state of the French and German economies. Debt relief, he said, should come out of national budgets, not asset sales, a sentiment in line with criticism from Germany's Central Bank.

The gold mining sector, one of South Africa's most important industrial sectors, is on it's knees due to the very low gold prices of recent years. The low gold price of recent years has not been helped by Mr Brown's continual use of judicious sound bites regarding sales of the IMF's gold reserves. Nevertheless, this threat of extra supplies of gold coming onto the market has not stopped gold's advance of some 75% in recent years but many precious metal analysts believe it would be a lot higher were it not for these much touted but very elusive gold sales.

Also against the proposal were senior executives in the gold mining industry particularly in South Africa where the low gold price of recent years has devastated the mining industry with consequences for employment in South Africa and throughout Africa and the Developing World. Once the cornerstone of the economy, South Africa's gold production is expected to continue falling in 2005 after slumping 9% in 2004 to its lowest level since 1931. The South African Chamber of Mine's Chief Economist Roger Baxter said that 10 mines employing around 90,000 miners and accounting for half of the country's output are marginal or loss-making at the current rand gold price. Baxter said that while the local gold industry had focused on improving productivity and reducing costs, it is being swamped by costs over which it has no control - such as water, steel, labour and especially fuel.

Historically low precious metal, base metal, natural resource and commodity prices have wrought terrible damage to developing world economies in recent years as unlike more industrialised economies, developing world economies are very dependent on their natural resources and on their exports from these sectors.

The fact that gold production in the major gold producer in the world, South Africa, and indeed globally is in decline and has been for some years means that the burgeoning supply demand deficit will likely be filled by higher gold prices in future years.

What Gordon Brown, who seems to be single handedly spearing this misguided campaign, should explain is why sales of some of the> IMF's 3,217 tonnes of gold are necessary to fund Debt Relief in Africa. As the gold bullion is vastly undervalued at just some $5 billion, nearly 90% below today's market prices of $45 billion wouldn't it be eminently more easier, practical, sensible and prudent to revalue the gold and with the subsequent dollar revaluation of the gold forgive the debt to the develpoing world countries in dollar terms. Most of the debt irresponsibly loaned to corrupt dictators (who used it to buy armaments, fund extravagant lifestyles and open up bank accounts in Switzerland and other offshore locations) and crippling many develpoing countries is denominated in dollars anyway.

This is the same Gordon Brown who sold 395 tonnes of the UK gold reserves at the very bottom of the market at an average price of $275 per ounce. Accruing about £2.3 billion to the UK exchequer. Economists calculate that he would have made almost £3 billion had he waited until today.

At the time he was accused of trying to take Britain into the European single currency by stealth after surprising the City with an announcement that he was selling more than half of the country's gold reserves, leaving Britain the lowest bullion holdings of any major country as reported in the Daily Telegraph.

At the time floods of irate British citizens choked telephone lines to protest against the Labour government's decision to sell some of the UK's gold reserves. "This is a staggering response, far beyond anyone's initial expectations," said Haruko Fukuda, chief executive officer of the World Gold Council. "It underlines the fact that the vast majority of the UK's citizens do not want the government to sell Britain's gold reserves, which are the rock upon which this country's economy rests in times of crisis," Fukuda continued.

As Sir Henry Tapsell said of Brown's misguided gold sales: "The whole point about gold, and the quality that makes it so special and almost mystical in its appeal, is that it is universal, eternal, and almost indestructible. The minister will agree that it is also beautiful. The most enduring brand slogan of all time is: 'As good as gold.' The scientists can clone sheep and may soon be able to clone humans but they are still a long way from being able to clone gold, although they have been trying to do so for 10,000 years.... The chancellor may think that he has discovered a new Labour version of the alchemist's stone, but his dollars, yen, and euros will not always glitter in a storm, and they will never be mistaken for gold."

As Sir Henry Tapsell said of Brown's misguided gold sales: "The whole point about gold, and the quality that makes it so special and almost mystical in its appeal, is that it is universal, eternal, and almost indestructible. The minister will agree that it is also beautiful. The most enduring brand slogan of all time is: 'As good as gold.' The scientists can clone sheep and may soon be able to clone humans but they are still a long way from being able to clone gold, although they have been trying to do so for 10,000 years.... The chancellor may think that he has discovered a new Labour version of the alchemist's stone, but his dollars, yen, and euros will not always glitter in a storm, and they will never be mistaken for gold."

If Mr Brown believes that gold reserves should be sold for debt relief purposes than why didn't he use the funds accrued from his UK gold reserve sales for debt relief purposes. Why are the IMF's gold reserves to be used for debt relief purposes when the UK's gold reserves were not? When did he have his eureka moment?

Most debt relief and charity groups have argued that if the IMF revalued its gold reserves, that would free up billions of dollars to cut debt for the worst-off nations. Yet instead of proposing this Brown continues to float the red herring of IMF gold sales which he has no power to make happen and he must realise are very unlikely to ever happen.

Gordon Brown should explain why the debt relief could not be funded out of the British national budget and why if aid to the Third World is such a high priority for his government, will Britain not reach the UN target of 0.7% of GDP until 2013. EU countries have long been committed to spending 0.7 per cent GDP on development aid, but only Norway, Denmark, Luxembourg, the Netherlands and Sweden currently meet this target. Britain (0.34 per cent) is only halfway to meeting their commitments in this regard.

In October 2004, Gordon Brown said that the IMF had decided in 1999 on a revaluation of their gold reserves in order to forgive debt. What has changed in the interim? Why wasn't this followed through on and if the aim of the much mooted gold sales is to help the developing world why would gold sales be the best way to achieve this and why are gold sales the only solution continually proposed by Mr Brown?

Freeing poor countries from their debt burden would allow them to spend that money to fight preventable diseases, improve education and health systems and make other reforms This is obviously one of the most important issues facing humanity today. Disingenuous public statements by Mr Brown should desist.

Actions speak louder than words. Maybe Bono can have a word in Mr Brown's ear?

Opinions

"...from a portfolio diversification standpoint, holding gold has proven to be an excellent investment. We at the BIS hold a considerable amount of gold and in recent years have benefited considerably on a valuation basis from the rise in the price of gold."

Robert Sleeper, Head of the BIS Banking Department, 'How Central Banks Manage their Finances' Bank for International Settlements (The Central Bank's Central Bank)

"With each passing day, given the problems incumbent in the EUR as Europe moves toward the constitutional referenda in the Netherlands and France, we can make the stronger, and ever stronger, case that Gold/EUR shall move higher even as the dollar itself gains relative to the EUR. Gold shall become a more "reservable" asset as central banks who might have been interested in diversifying their assets away from the dollar now find the EUR less and less attractive, and find gold somewhat more so."

Dennis Gartman, Gartman Newsletter

"Gold-it is unlike all other elements on earth. Virtually indestructible, this precious metal has been the source of countless fables and has mobilised the growth of nations and financial infrastructures worldwide. Human beings have been utilizing gold as both a form of currency and an investment for thousands of years.

As an asset class, gold is unique. Durable and highly liquid, the economic forces that determine the price of gold are different from the economic forces that determine the price of many other asset classes such as equities, bonds or real estate. A potential safe haven from the uncertainty of economic events, political unrest and high inflation, gold offers investors an attractive opportunity to diversify their portfolios-potentially reducing overall portfolio risk and ultimately preserving portfolio wealth.

Unlike paper, gold is an imperishable asset. And unlike equities or bonds, the value of which is dependent on the issuer's ability to pay in the future, gold-does not depend on anyone else's ability to pay. Over time, gold has tended to maintain its purchasing power, especially during periods of economic or political upheaval. It has often been quoted that "With an ounce of gold a man could buy a fine suit of clothes in the time of Shakespeare, in that of Beethoven and Jefferson, in the Depression of the 1930s." In fact, analysis suggests that the real value of gold may fluctuate in the short term, but that it has consistently returned to its historic purchasing power parity with respect to other commodities over the very long term. Consequently, over a long period of time, gold may be an effective tool for preserving wealth.

During periods of economic and political instability, when the value of many other assets may have fallen dramatically, gold has commonly remained a store of value. Statistical analysis shows that the price movements in gold tend not to move in tandem with those of traditional asset classes, such as equities and real estate. Historically, gold has shown low to negative correlation with equities and other conventional asset classes. Although the aim of diversification is to hold a wide array of assets that perform differently from one another under various market conditions, studies have suggested that developed equity markets tend to become more closely correlated during periods of market turbulence. Conversely, commodities tend to become less correlated with major asset classes during such periods.

Additionally, a 2003 study concluded that not only was gold negatively or insignificantly correlated with major asset classes, but that it was largely uncorrelated with macroeconomic variables such as GDP, inflation and interest rates. Including gold in a portfolio potentially lowers overall risk without necessarily decreasing returns. It may reduce the likelihood of large losses during any period, including during periods of market volatility."

Davy's Market Report, January 2005, Davy Stockbrockers

"Mortgage giants Fannie Mae and Freddie Mac could threaten the economy if Congress fails to curb their investment activities."

Alan Greenspan, Chairman of the Federal Reserve

"Fannie Mae, the government-sponsored mortgage association, has been battling a mounting scandal since last year. It has accounting errors of about $11 billion. That's more than nineteenfold Enron's $567 million error." "Fannie Mae's whole mess caused the departure of Chief Executive Officer Franklin Raines and several other top executives. At the same time, Fannie Mae stock has dropped roughly 30 percent: from nearly $80 a share to around $55."

Dan Gainor, 'Fannie Mae's bailout tab', Washington Times

"Imbalances in the world economy and their possible effects on currencies and interest rates may lead to a synchronized fall in property prices in industrialized countries, exacerbating the indebtedness of households and curbing private consumption."

German government official on latest IMF report as quoted in Bloomberg, 'IMF Sees Risk of Dollar Fall, German Official Says'.

"The costs of a breakdown of confidence in the U.S. financial system due to renewed corporate scandals would be huge ... A repetition of such scandals could be even more damaging than before. We're a long way from a complete collapse of our economic system, but you can't multiply that kind of lack of trust and so forth very much before you really begin to get worried about the damage done to the larger financial system and the larger economy ... If it happens enough, the effect on the larger system is just potentially huge."

Jack Guynn, Atlanta Federal Reserve Bank President

"The article is couched in the circumspect language that is typical of ECB pronouncements. But it clearly expresses the bank' concern that historically low interest rates are pumping money into real estate, and that slowing this trend with higher borrowing costs outweighs the risks to economic growth. "The central bank would adopt a somewhat tighter policy stance in the face of an inflating asset market than it would otherwise allow if confronted with a similar macroeconomic outlook under more normal market conditions," the article said. Economists regard skyrocketing real estate prices as risky because of the potential effects when these "bubbles" finally burst. If assets plunge in value, consumers often rein in spending, and drag an economy into recession. The incipient signs of a real estate bubble, though highly uneven across the euro zone, are clearly present in some countries."

Carter Dougherty, ECB shifts focus, worried by rising asset prices, International Herald Tribune

Opinions and Quotes can be found in articles in the News and Commentary sections of www.gold.ie.

Key Events in the Week Ahead

First-quarter earnings season will flow in during the week ahead.

Earnings from big companies like Intel Corp. <INTC.O> and Pfizer Inc. <PFE.N>, as well as key inflation reports, will help determine whether U.S. stocks will continue to skid lower or bounce back next week. Monday kicks off one of the heaviest weeks of the quarterly earnings season and some of the other companies slated to report include General Motors Corp. <GM.N> and Ford Motor Co. <F.N>, Internet companies eBay Inc. <EBAY.O> and Yahoo Inc. <YHOO.O>, financial heavyweight Merrill Lynch & Co. <MER.N> and soft-drink giant Coca-Cola Co. <KO.N>

Concerns about inflation will be either assuaged or exacerbated in the week ahead as the Labor Department releases its two key pricing reports back to back. Tuesday brings the Producer Price Index, which measures wholesale costs. The PPI expected to rise 0.6 percent in March after a 0.4 percent increase in February. With volatile food and energy costs excluded, so-called core PPI is expected to climb just 0.2 percent, up from 0.1 percent in February. Wednesday sees the release of the Consumer Price Index, which measures the prices individuals pay on the retail level. The CPI for March is expected to remain steady with a 0.4 percent increase, but core CPI is expect to climb just 0.2 percent, down from February's 0.3 percent. Given Wall Street's focus on inflation and the Federal Reserve's likely response with interest rates, these two reports will be watched very closely, and the market's reaction is likely to be pronounced.