The long term needn't look quite so far off for bullion buyers right now...

Put aside the rise in US interest rates, GDP and Fed tapering talk. Just glance at the rest of this summer's headlines, and you'd think it offered a bull market for 'hard money' gold and silver.

-

Japan is doubling its monetary base inside two years, while the People's Bank of China has taken to one-day injections of almost $3 billion for the financial system, boosting shares after a scary jump in bank interest rates...

-

Wage talks in South Africa's gold mining industry stalled Monday, with management offering 5% where the unions want a raise of 60-100%...

-

Giant banks who swerved around the financial crisis 5 years ago are now risking a crash in summer 2013. Barclays bank - "widely regarded as one of the UK's strongest" according to the BBC - is nearly £13bn short of capital requirements (almost $20bn). Deutsche Bank paid €630m ($830m) in April-to-June alone to settle lawsuits from customers mis-sold rubbish US mortgage investments...

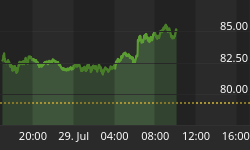

Yet here we are, back down below April's crash low of $1322 in gold and well under $20 for silver. Yes, that's above end-June's three-year lows. Yes, the rebound has been strong so far. But so it should be after prices fell at their fastest pace in three decades. Other big banks are meantime making great money trading the rise in longer-term US interest rates.

Those rates have risen because the US Fed says it's likely to start trimming its money-printing QE program soon. And those cuts only look more likely after the US Treasury said Monday that its deficit - the gap between what Washington spends and receives - has shrunk 40% so far this fiscal year, cutting the amount of new debt it needs to sell to the bond market.

As the trading desks thin out for the summer however, some big-name investors with longer time horizons are buying this drop in bullion. Michael Cuggino, president of the $12bn Permanent Portfolio Family of Funds, thinks gold will rise long-term on rising inflation. "What you're seeing," reckons Mark Mobius, emerging-markets specialist at Franklin Templeton, which now runs $813bn for investors, "is a dissonance between real demand and derivatives. So from a longer-term perspective we believe gold prices will trend upwards."

On that point, Swiss bank UBS - a London market-maker and major world dealer in bullion - calls China's physical demand "strong" and says it "holds the promise of a sturdy price floor" as banks in the world's second largest economy widen access to gold bullion through new savings accounts. And on the US government's shrinking deficit, note that:

-

it's still forecast well over $1 trillion for 2013 as a whole, the fourth largest ever;

-

the relief comes from a one-off payment of $66bn from the state-guaranteed mortgage lenders Fannie and Freddie, nationalized during the 2008 crisis;

-

there's still the annual stupidity of the "debt ceiling" to get through, perhaps with the real fun and games pushed back to November but risking the same kind of panic which helped gold hit $1920 per ounce in summer 2011.

Short term - and this news-packed summer week more than most - precious metals owners who don't like volatility should look away now. But further ahead, there are lots of good reasons to buy gold or silver. Chief among them is the unique exposure it gives Western investors to Asia's long-term growth.

China, for instance, is set to overtake India as the world's No.1 gold consumer this year. Buying perhaps 1,000 tonnes of gold - around 1 ounce in every 4 sold worldwide in 2013 - China is growing its jewellery demand, but not as fast as it's hoarding investment gold bars and coin. So says Marcus Grubb of market-development organization (and BullionVault shareholder) the World Gold Council. And with the Shanghai Gold Exchange delivering 1,000 tonnes in the first half of 2013 alone - more than its users took in all of 2012 - that switch looks a good call already.

Marcus isn't the first person to forecast this switch. We tried it in 2009, as did other better-informed analysts. We were all wrong then. But 2013 looks more certain, as Marcus notes. Because compared to China's surging demand, Indian buying is of course being crimped by the government's attempts to cut demand. So far all it's managed is to crimp supply, boost prices, and unleash a return to smuggling.

Why does this matter to Western investors? First because, behind the noise of US futures trading, physically-settled metal is what counts in the end. And China, like India, continues to buy more gold at rising prices. Secondly, and longer-term, the economic future of Asian households looks a lot like the developed West in terms of disposable income. But unlike the modern West, the first thing which Indian and Chinese families with cash left over at the end of the month choose to do - their primary savings choice - is very often to buy gold.

Take note: The path between the last 20 years of Chinese economic growth and the much-lauded "Chinese century" before us may not prove smooth. Western analysts have long predicted a "hard landing" in China. But the near-term risks look plain (huge local government debts, massive property bubble, misallocation of national funds in pointless infrastructure). The upshot for gold and by extension for silver prices might not be pretty. It's worth reviewing what SocGen's latest Cross Asset Strategy note says on the subject of gold and a China hard landing.

The decline of the West has also long been forecast by misery-guts like ourselves. But rising prosperity in Asia will likely mean stagnant or falling standards of living here, on a relative basis if not absolute. And as we've long suggested, buying a little of what China uses to store its growing wealth makes sense long term.

But blocking out the noise won't be easy meantime.