"Why Asia should be on your list..."

In this edition we will cover the various major currencies as they compare to the dollar, what's been driving them, and our short and long term outlook.

It's been an exciting couple of months for the currencies with the Dollar finally staging an enormous rally against all the majors to the despair of most "gurus." As the Euro danced around 1.36, the noise from all the new found currency geniuses forecasting a "dollar collapse" couldn't be louder -- although it is odd that two years prior, when the trend began, they were nowhere to be seen. No matter, with everyone and their mother short the dollar for one reason or another and Dollar-bear articles appearing in Newsweek and Times, it was a great time to be a contrarian and look for the reversal.

Before we begin, I would urge everyone to dispel many of the notions that they may have gathered from a variety of Gold-Bug articles, or other so called guru's, about what exactly drives the currency markets. I have seen many writers tout deficit spending as the major reason for the coming "dollar collapse" while completely ignoring interest rate moves, when the prior has low historical correlation, and the later is considered to be one of the most predictive. Currencies are probably one of the most fundamentally complex instruments to value and predict, not only because their value is always relative to other currencies, but because their reactions are sometimes fickle and counter-intuitive. I would urge readers to read as much as they can from as many sources as possible before making considerable currency investments.

One of the main drivers of currency markets are interest rates. The following is a brief explanation so that we are all on the same page. When the Fed is raising or lowering rates, they are controlling the short term rates or "Over-night Lending Rates" often referred to as the Central Bank Rate. However, since not all currencies have the same rate, there is usually an interest rate spread between any two currencies (crosses) - and because of this, an investor can borrow a low yielding currency and invest in a high yielding currency which is called a 'carry trade.' For instance, the Euro now yields 2.00% annualized while the Yen yields 0% -- so if you borrowed (sold) yen, and invested (bought) Euros, and held for a year, you would make the interest rate differential of 2.00% -- sort of like a dividend. However, just like with stocks and dividends, you are also subject to the gains or losses in the underlying cross. These rates, and the expected future movements of these rates, have a huge impact on longer term currency trends since funds tend to naturally flow from low return environments to high return. Stronger economies are not only more likely to spur more demand for their currencies as investors invest in their markets, but are also more likely to raise rates to contain inflation, and are more likely to sustain those higher rates. This flow can reverse if investors feel uneasy in a certain high yielding currency, and may wish to swap into a "safer" currency such as the Swiss Franc. All this depends on the current sentiment and risk aversion of traders.

One of the main drivers of currency markets are interest rates. The following is a brief explanation so that we are all on the same page. When the Fed is raising or lowering rates, they are controlling the short term rates or "Over-night Lending Rates" often referred to as the Central Bank Rate. However, since not all currencies have the same rate, there is usually an interest rate spread between any two currencies (crosses) - and because of this, an investor can borrow a low yielding currency and invest in a high yielding currency which is called a 'carry trade.' For instance, the Euro now yields 2.00% annualized while the Yen yields 0% -- so if you borrowed (sold) yen, and invested (bought) Euros, and held for a year, you would make the interest rate differential of 2.00% -- sort of like a dividend. However, just like with stocks and dividends, you are also subject to the gains or losses in the underlying cross. These rates, and the expected future movements of these rates, have a huge impact on longer term currency trends since funds tend to naturally flow from low return environments to high return. Stronger economies are not only more likely to spur more demand for their currencies as investors invest in their markets, but are also more likely to raise rates to contain inflation, and are more likely to sustain those higher rates. This flow can reverse if investors feel uneasy in a certain high yielding currency, and may wish to swap into a "safer" currency such as the Swiss Franc. All this depends on the current sentiment and risk aversion of traders.

Trade imbalances can also effect a currency, but not in the manner that many expect. Here is a concise explanation from FXCM - "Country trade balances (the difference between imports and exports) can also affect the profitability of a carry trade. We have shown above that when investors have low risk aversion, capital will flow from the low interest rate paying currency to the high interest rate paying currency. This however, does not always happen. To understand why, think about the situation in the United States. The US currently pays historically low interest rates, yet it attracts investment from other countries, even when investors have low risk aversion (i.e., they should be investing in the high interest rate countries). Why does this occur? The answer is because the US runs a huge trade deficit (its imports are greater than its exports)—a deficit that must be financed by other countries. Regardless of the interest rates it offers, the US attracts capital flows to finance its trade deficit. The point of this example is to show that even when investors have low risk aversion, large trade imbalances can cause a low interest rate currency to appreciate."

In conclusion, the three main factors driving currency trends are interest rate expectations, economic performance (relating to capital flows and rate expectations), and investors risk aversion. I would encourage readers to research more on these subjects to become more familiar with how capital flows between countries.

The Dollar - The initial dollar decline began as a reaction to the sharp rate cuts by the Fed as the internet bubble toppled over like a house of cards. Rates dropped from around 6% all the way down to 1% in the span of about three years. The decline was also driven by a certain amount of hype, as the Euro began to establish itself as a major currency that many felt had "new reserve currency" written all over it. Although the dollar initially needed to be devalued, a 30% decline over the course of three years is a huge move by any measure - and in my opinion was an over-reaction. The dollar remains the world's dominant reserve currency and is still the basis of most commodity and oil market transactions (hence the Petrodollar). Moreover, the U.S. Fed is one of the few central banks that have been raising rates -- most have either done nothing while some have even cut rates. Rising U.S. rates will continue to exert positive pressure on the dollar as long as investors believe that the Fed will continue to raise, or at least maintain, those rates.

The Dollar - The initial dollar decline began as a reaction to the sharp rate cuts by the Fed as the internet bubble toppled over like a house of cards. Rates dropped from around 6% all the way down to 1% in the span of about three years. The decline was also driven by a certain amount of hype, as the Euro began to establish itself as a major currency that many felt had "new reserve currency" written all over it. Although the dollar initially needed to be devalued, a 30% decline over the course of three years is a huge move by any measure - and in my opinion was an over-reaction. The dollar remains the world's dominant reserve currency and is still the basis of most commodity and oil market transactions (hence the Petrodollar). Moreover, the U.S. Fed is one of the few central banks that have been raising rates -- most have either done nothing while some have even cut rates. Rising U.S. rates will continue to exert positive pressure on the dollar as long as investors believe that the Fed will continue to raise, or at least maintain, those rates.

Looking into the future, however, the U.S. economic outlook is a bit more uncertain. Statistics have been mixed at best, and with a number of world economies showing signs of slowing down, it seems like only a matter of time before we begin to see more serious signs of an economic slow down here in the U.S. Many are already calling for the Fed to stop raising rates and feel that the Fed will once again 'over-shoot.' There is also evidence that foreign investment in dollar denominated assets has slowed considerably to the extent that deficit funding has become an issue. Since a large part of this rally was due to the Fed's tightening and an economic recovery, any indication to the contrary will certainly be a negative for the dollar. This could take a couple months to pan out, however, so I think the short term dollar picture will remain positive while the long-term picture is still shaky.

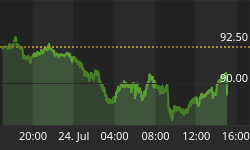

Technically, the dollar is showing some very nice strength with a lot of traders getting run over thinking it was going to pullback more along the way. My initial target was around 90-92 which is right below the 2004 highs. Although anything is possible, I suspect that a pullback at these levels is more likely then a rip through the highs - it would probably be a pullback to buy. If the pull back is weak and choppy, I think we will go through the highs and eventually roll up to 95 which is the 38% retracement of the entire down trend.

The European Crosses - Although it may be a mistake to bundle the European currencies together (Euro, British Pound, Swiss Franc), since their short term issues differ considerably, my long term views and sentiments about them are similar. Over the past 3 years, the Euro has risen not so much on European news and data, but on U.S. news, labeled as the anti-dollar. Similar to how Kerry was accepted by many for simply not being Bush. As the Euro rallied, actual news from Europe was virtually ignored as traders fixated on U.S. economic reports and uncertainties. Sentiment has most certainly shifted in the past couple of months as it seems that any European news is bad news, and bad U.S. news is of no real interest. This is a classic example of the sentiment shift during trend changes.  So much so, in fact, that after being viewed as the successor to the dollar only a few months ago, there is now open speculation about the future viability of the Euro. As level headed investors, we must ignore such panic machines and look at the facts. First of all, the European Monetary Union is a separate entity from the European Union and by itself won't necessarily share the EU's fate - although it will continue to be associated with the uncertainty. People in Europe are well accustomed to the Euro and appreciate how much easier and more stable exchange is because of it. In short, the Euro isn't going anywhere. Even if the worst case scenario pans out in Italy, and they switch back to the Lira, I very much doubt the rest of Europe would follow suit. This doesn't mean that all is well however.

So much so, in fact, that after being viewed as the successor to the dollar only a few months ago, there is now open speculation about the future viability of the Euro. As level headed investors, we must ignore such panic machines and look at the facts. First of all, the European Monetary Union is a separate entity from the European Union and by itself won't necessarily share the EU's fate - although it will continue to be associated with the uncertainty. People in Europe are well accustomed to the Euro and appreciate how much easier and more stable exchange is because of it. In short, the Euro isn't going anywhere. Even if the worst case scenario pans out in Italy, and they switch back to the Lira, I very much doubt the rest of Europe would follow suit. This doesn't mean that all is well however.

European growth has been fairly lackluster, never really recovering from the last recession. Despite Britain's impressive economic growth early on, it is also beginning to show signs of slowing. Recently the BOE had two dissenting "rate cut" opinions which sent Pound investors scrambling to sell. Pressure has also been mounting for the ECB to lower rates in light of stagnant to worsening economic conditions. Although rate cuts are unlikely, in light of a rising rate dollar, it is obvious that many investors have decided to make the switch back over to the Dollar which suddenly looks good again. The Swiss Franc, although considered a safe haven by many, has also had a tough time economically with mediocre growth.

Overall, my outlook for Europe remains fairly negative. Not only do the chances of further rate increases seem unlikely due to the lackluster recovery and tame inflation (especially now that Britain is slowing), but aging and debt ridden socialistic systems along with the uncertainty of E.U. politics are all going to make investors think twice before committing their wallets. Because of this, I don't see any solid fundamental plays in these currency markets and think that the best way to play them will be on a short to medium term technical basis which will be covered daily on our website. Let's move on to some crosses that I think are much more exciting as fundamental plays.

The Asian Crosses - Although this category really consists of only one tradable currency, the Yen, its fate is so deeply intertwined with that of the emerging Chinese Yuan that you cannot discuss it without the other. Since the bursting of the Japan bubble in the early 90's, the Japanese have been battling a 15 year bear market. Their markets and economic statistics have gained some ground but are still on the slow side. Although I think that Japan will recover from this bear market eventually, the real story here is China. China has been the number one growth story of the last five years, and Japan has been in an ideal situation to exploit the well being of its neighbor. The following are some significant points to consider.

- The average bear market lasts around 15 years. Although signs of recovery are only now beginning to appear, the long term chart of the Nikkei average is intriguing and can be checked out here.

- Japan is almost completely dependent on imported oil and energy. Unlike other large economies whose oil companies make money on higher prices and help dampen the blow, Japanese consumers are bearing the full brunt of it. However, if anyone can afford it, it's the thrifty Japanese who have one of the highest savings rates around. Question remains whether oil is going to draw from the already lackluster consumer spending or from savings. Investors should also be wary of the recent spats between China and Japan over energy located in the gulf between them. The website atimes.com is one of the few sites that covers news like this, but it has the potential to develop into a serious issue. Both countries have been searching for new sources of energy and oil - it may only be a matter of time before they, or some other country, gets in their way politically.

- Along with higher oil prices and robust growth from neighboring China, Japan is finally experiencing positive inflation (if just barely), a plus for a country that has been battling deflation for a long time. In fact there is actually some talk about raising rates! Japan has been sitting on 0.0% short term rates for many years now, and is entertaining the notion of moving towards a positive rate environment.

- Short interest on the Yen is massive since it has been on the short end of a lot of carry trades due to its 0% rates. A more public move towards positive rates could really rattle traders and we could see some serious short covering.

- China is moving slowly but surely towards eventually floating its currency with some recent improvements in the China banking story. On June 17th Bank of America made a bid for a 9% stake in the CCB (China Construction Bank) which is cheered on by many who see foreign investment and managerial oversight in Chinese Banks as being the way out for the struggling state owned banks. Asia Times writes "Such hands-on foreign management has pointed to a new way to shore up China's dire banking situation, and may turn out to be a realistic way for future progress. The foreign involvement also suggests how difficult it would be for China to create modern banks without the employment of modern management and accountability as well as well-defined ownership."

(http://www.atimes.com/atimes/China/GG02Ad05.html) - Although traders have gleefully been buying up the USD/JPY cross due to the carry trade potential, they are fearful of announcements or moves by China towards floatation which most think will cause all of the Asian currencies to rise with the tide. It is important to remember that in the competitive currency devaluation that has been going on in Asia, the countries are devaluing more because of each other then pressure from it's major buyer the United States. All the Asian countries worry that if they let their currencies rise, then they'll be priced out by their neighbors. However, if China begins floating their currency, the other countries would be more than happy to stop spending so much money on devaluing and start making more from their U.S. exports - as long as they all do so together.

- One of the best times to get into a long term currency trade is during the turn-around period when rates, economic performance, and capital flows are all beginning to look up. A lot of people are caught on wrong side of the new trend, and these can usually be ridden for quite some time.

All these factors make Asian currencies and investments very intriguing. The question remains as to timing. I don't know if these factors are going to come together this year, next year, or in five years -- and until (if) they do, anything can happen. It is, however, a classic case of everyone being on one side of the market and very few people considering the other side. I usually have a good feeling I am right when everyone disagrees with me, as they did in December when I called for a Euro top. So although I wouldn't start buying Yen right here since the Yen is in an established medium-term downtrend, I will be looking for entries over the next couple months, taking into consideration the movement in the Nikkei. The USD/JPY has really shot up recently as traders are scrambling out of dollar shorts (hoping we would break previous highs). I would wait for a confirmed downtrend (lower lows) before throwing on a longer term short. I would also point out that the Yen has been performing well verses the European currencies, such as the EUR/JPY cross which we are shorting on the bounce.

The Commodity Crosses

With a booming commodities market, it is no surprise that the value of strong commodity producing countries has risen right along side it. If a country produces a lot of commodities and the prices rise, then other countries need to buy more of that countries currency to buy the same amount of goods in order to cover the higher price, therefore the value of the currency increases. The two most popular commodity currencies are the Canadian Dollar which is highly correlated with oil prices, and the Australian Dollar which follows the metals. Both currencies have preformed very well over the past three years and both have retained much of their strength in the face of a dollar rally. The Canadian dollar in particular remains very strong due to higher oil prices despite the recent political turmoil. There has been quite a bit of political drama involving the prime minister and various budget issues that will continue to make investors wary - however I often find that when it's political issues pulling a currency against a trend, it often reaches unreasonable levels and can make for great trades when the issue resolves itself. I know that a lot of hedge funds have been hammering short the USD/CAD looking for a resolution. Economically, Canada has done pretty well although it is intrinsically linked to the U.S. - if the U.S. gets weaker, they'll get dragged down with them.

With a booming commodities market, it is no surprise that the value of strong commodity producing countries has risen right along side it. If a country produces a lot of commodities and the prices rise, then other countries need to buy more of that countries currency to buy the same amount of goods in order to cover the higher price, therefore the value of the currency increases. The two most popular commodity currencies are the Canadian Dollar which is highly correlated with oil prices, and the Australian Dollar which follows the metals. Both currencies have preformed very well over the past three years and both have retained much of their strength in the face of a dollar rally. The Canadian dollar in particular remains very strong due to higher oil prices despite the recent political turmoil. There has been quite a bit of political drama involving the prime minister and various budget issues that will continue to make investors wary - however I often find that when it's political issues pulling a currency against a trend, it often reaches unreasonable levels and can make for great trades when the issue resolves itself. I know that a lot of hedge funds have been hammering short the USD/CAD looking for a resolution. Economically, Canada has done pretty well although it is intrinsically linked to the U.S. - if the U.S. gets weaker, they'll get dragged down with them.

As for the Australians, their economies have been performing admirably as well and the central bank has kept the rate high to the joy of many carry traders. The metals, and particularly gold, have been driving forces for this currency and have helped keep it bid in the face of the dollar rally. As the Euro started falling, gold broke its Euro correlation and actually rose with the dollar to the joy of many gold-bugs. Look for the two to break out of their consolidations together.

As for the Australians, their economies have been performing admirably as well and the central bank has kept the rate high to the joy of many carry traders. The metals, and particularly gold, have been driving forces for this currency and have helped keep it bid in the face of the dollar rally. As the Euro started falling, gold broke its Euro correlation and actually rose with the dollar to the joy of many gold-bugs. Look for the two to break out of their consolidations together.

Technically and fundamentally, I like both of these currencies and am looking at both USD and EUR crosses with these guys. If the commodity bull continues to rage, as I suspect it will over the long term, these currencies will continue outperform

*Conclusion*

It has been a wild ride in the currency markets - just the way we like it. Because of its volatility, we cover the longer term time frames here in the newsletter. It's at those time frames were we can combine fundamental and technical analysis. Shorter term trades and follow ups on these ideas are blogged at www.runetrading.com.

I would also like to issue a quick lesson, or a warning so to speak. Every week, I read a variety of articles covering everything from Google to Euro futures to gold. What often gets on my nerves are writers who are so ridiculously perma-bullish or bearish on whatever they are covering, that when it goes their way, they gleefully highlight how right they are, and how this is just the beginning of a parabolic move, and when it goes against them, they write about the ridiculousness of the market, why it's just a temporary move, or how manipulated that market is. Every week they'll post the same updated chart with an arrow pointing straight up or down from where we currently are as a 'forecast' of where the market should go. I'm not saying that these people don't post good ideas sometimes, or have faulty analysis, but I am saying that they can be amazingly stubborn on their 'recommendation' when everything is pointing to the contrary. I know a number of currency analysts who have publicly maintained their "kill the dollar and buy the euro" stance every single day, all the way down. To them, every up day is the beginning of the new rally, and every down day is just a temporary set back. Sure, they may be right eventually, as those who will forever tout one side of the market tend to be, the problem is that if you follow this mentality, you can end up riding out huge loses or losing all your profits just because you refused to see a very blatant change in the direction of the trend. I am not saying that longer term investors should be jumping out every day the market looks like it might go against them, but I am saying that every investor should have an idea of not only where they are going to get out (if it starts riding against them) but what exactly the signals of that trend change might be, so you are not blind to them when they appear. Whether it's the NASDAQ turn in 2000 or the beginning of an oil rally, it's almost more important to know what to look for to exit your trade than it is to enter it. Don't be that lop-sided trader - trade your money not your pride.

I would also like to issue a quick lesson, or a warning so to speak. Every week, I read a variety of articles covering everything from Google to Euro futures to gold. What often gets on my nerves are writers who are so ridiculously perma-bullish or bearish on whatever they are covering, that when it goes their way, they gleefully highlight how right they are, and how this is just the beginning of a parabolic move, and when it goes against them, they write about the ridiculousness of the market, why it's just a temporary move, or how manipulated that market is. Every week they'll post the same updated chart with an arrow pointing straight up or down from where we currently are as a 'forecast' of where the market should go. I'm not saying that these people don't post good ideas sometimes, or have faulty analysis, but I am saying that they can be amazingly stubborn on their 'recommendation' when everything is pointing to the contrary. I know a number of currency analysts who have publicly maintained their "kill the dollar and buy the euro" stance every single day, all the way down. To them, every up day is the beginning of the new rally, and every down day is just a temporary set back. Sure, they may be right eventually, as those who will forever tout one side of the market tend to be, the problem is that if you follow this mentality, you can end up riding out huge loses or losing all your profits just because you refused to see a very blatant change in the direction of the trend. I am not saying that longer term investors should be jumping out every day the market looks like it might go against them, but I am saying that every investor should have an idea of not only where they are going to get out (if it starts riding against them) but what exactly the signals of that trend change might be, so you are not blind to them when they appear. Whether it's the NASDAQ turn in 2000 or the beginning of an oil rally, it's almost more important to know what to look for to exit your trade than it is to enter it. Don't be that lop-sided trader - trade your money not your pride.

Best of luck and Happy 4th of July.

{kind=link}