In reaching a deal with Greece, Germany is the last remaining holdout.

Even Greece-skeptic countries like Finland have shifted 180 degrees to become true believers in mathematical nonsense.

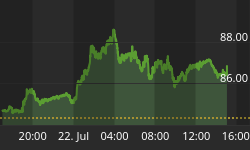

And after bitter fighting and infighting, Greece nears €86bn Accord with Creditors.

Significant concessions by Alexis Tsipras and his negotiators in the past month have encouraged other hawkish eurozone members such as Finland to break with Berlin, which wants to hold out longer to squeeze more reforms from Athens.

Even previously sceptical EU diplomats now say that a full agreement could be reached by the August 20 deadline, when Athens must make a €3.2bn debt repayment to the European Central Bank.

The cautious optimism contrasts sharply with the acrimony at last month's eurozone summit, which came close to ushering Greece out of the currency bloc before agreeing to negotiate a deal. The main elements of the proposed deal include spending cuts, administrative reform and privatisations. Remaining sticking points between Athens and its creditors include details of a €50bn privatisation plan and proposals for raising the planned budget surplus, excluding debt interest, to 3.5 per cent of gross domestic product in 2018 from zero this year.

Officials in Brussels said an early deal was "ambitious but feasible". But they emphasised that while this was the "preferable" way forward, the option of a €5bn bridging loan to give negotiators more time, championed by Berlin, was still on the table.

Germany, the biggest creditor, was late last week still holding out for more reforms from Athens, arguing that a two- or three-week bridging loan was better than hurriedly striking an inadequate three-year deal. Jens Spahn, deputy finance minister, tweeted on Friday: "It is better done thoroughly than hastily."

An EU official said that even if Wolfgang Schäuble, Berlin's hawkish finance minister, dug in his heels, chancellor Angela Merkel would not want Berlin isolated.

Ambitious Yes, Feasible No

The plan certainly is ambitious. And it appears increasingly likely everyone will sign off on the deal, including Germany.

My doubts are not over whether everyone signs a deal, but rather whether Greece can stick to the terms.

I maintain that Greece is surely not going to reach and maintain a current account surplus of 3.5% of GDP in three years.

In fact, Greece is not going to maintain a primary account surplus (surplus excluding interest on debt) of 3.5%. Nonetheless, let's play the "What if?" game.

What If?

If by some miracle, Greece were to hit that fantasyland 3.5% surplus projection, Greece would be in very good position to tell the Troika to go to hell, declare the debts odious (as it did once before) and default.

As long as Greece can maintain a primary account surplus, no one could force it out of the eurozone.

Schäuble hopes to prevent such a default by requiring Greece to put up €50 Billion in assets as collateral for the loan. But realistically, Greece will have a hard time coming up with state assets worth that amount.

Also, agreeing to pledge assets and actually doing it are two different things.

Meanwhile, the cost of the bailout (and potential default) keeps going up, and up and up. A default five years ago may have cost banks €60 billion to €80 billion or so. Now, counting target2 imbalances Greece would default on over €400 billion.

Those who pretend the deal is "feasible" have not looked at the long-term math: To prevent banks from taking an €80 billion hit, taxpayers are at risk for well over €400 billion, counting all Greek liabilities.

IMF Participation

It will be interesting to see how the IMF plays this.

On July 31, the IMF staff reiterated Greece Disqualified for Bailout, Participation Depends on Debt Relief and Reforms.

More than likely, senior IMF officials will keep their mouth shut until the German parliament approves a deal. Then the IMF is very likely to demand haircuts for participation.

Germany's only choice at that point will be to pony up still more money, or agree to a haircut.