It's not the first time an Australian jobs report shows employment growth rise five times more than expected. Whether it will be revised downwards or not, it is undoubtedly reflecting partial strength in the nation's labour market. Australia added a net 58.8K jobs in September; over four times expectations, the highest increase in 3 ½ years and the 3rd biggest jump over the last 15 years. Remarkably, 40K of the 58.8K increase emerged from full time jobs, while only 18.6K was from part time employment. The 231.7K increase jobs in the first 10 months of the year showed the its biggest annual gain since 2010.

The unemployment rate surprisingly fell to an 18-month low of 5.9% from 6.2%, while the labour participation rate actually rose to 65.0% from 64.9%.

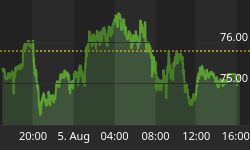

The Aussie had already been boosted in the days prior to the release of the jobs report, amid increased signals the RBA would stand pat on rates next month, due to upside surprise in Nov Westpac consumer confidence (6-month high at 101.7), last week's release of Sep retail sales and other improved sentiment surveys such as the ANZ Roy Morgan Weekly indices.

The Aussie jobs report is a manifestation of the dichotomy between the housing boom in Southeastern states of Victoria and New South Wales, where jobs rose 26,100 and 18,700 respectively, while in the recession hit mining state of Western Australia, unemployment rose to 6.4% from 6.1%.

More Capex Declines ahead

If you think the Aussie jobs report is a prelude to an ongoing stabilisation in the overall economy, then think again. Neither is the all-clear sign on commodities. Chinese fixed-asset investment rose at an average annual rate of 10% in the first 10 months of 2015, its slowest since 2000. Industrial production growth is back to six-year lows.

Mining capital expenditure more than quintupled since 2000, reaching $30bn a year to $160bn. As capacity soared, global iron production rose 125% according to Marathon Asset Management. Once demand failed to meet supply, commodity plummeted with the help of a resurging US dollar.

Just as oil prices are pressured by global production of 95.48 mn/barrel/day, exceeding demand of 93.86 mn/barrel/day (not to mention Iran's intentions to double production), mining capacity has yet to withdraw its excess for prices to stabilize. This requires more cuts in capex.

You don't need to be a regular reader of this column to know I've been calling for sharp cuts in capital expenditure by miners and energy exploration companies for quite a long time. It started on Dec 23 of last year in my 2015 Preview here, followed by July 17 and Sep 22. It went on but I'll spare you.

Falling capex will remain a net negative to global growth, exceeding the positives of cheaper energy/metals. The resulting decline in prices will also be made possible with the help of further Chinese currency devaluation. Considering that China went from importing 50% of most commodities to seeing its imports plummet by 50%, the demand and price impact has yet to play out.