As amazing as it now sounds, companies deemed to be highly risky were able to borrow money from US investors for less than 6% as recently as June 2014. To put this in perspective, 6% is not far from the US government's average 10-year borrowing rate for the past 50 years. And here were frackers, ultra-high-leverage retail chains and various other close-to-the-edge entities slurping up a torrent of cash from yield-starved investors who had forgotten about the other side of the risk/return equation.

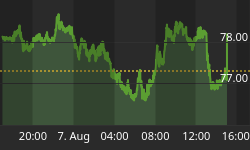

That this hasn't worked out so well is not much of a surprise. But the speed with which it has gone bad is still breathtaking. The following chart from Bloomberg illustrates just how fast an illogical market can be brought back to reality:

Now a growing number of reach-for-yield investors are finding that not only are they down on their bets but they can't get at their capital. Also from today's Bloomberg:

Third Avenue Redemption Freeze Sends Chill Through Credit Market

(Bloomberg) - Investors who piled into the riskiest corners of the credit markets during seven years of rock-bottom interest rates are getting a reminder of how hard it can be to cash out.

With outflows from U.S. high-yield bond funds running at the fastest pace in more than a year, Martin Whitman's Third Avenue Management took the rare step of freezing withdrawals from a $788 million credit mutual fund on Dec. 9. The firm's assessment that meeting redemptions would be impossible without resorting to fire sales has put a spotlight on the dangers for junk-bond investors as the Federal Reserve prepares to lift interest rates as soon as next week.

"It's definitely a dark cloud over the market," said Anthony Valeri, a strategist at LPL Financial, a Boston-based financial-advisory firm. Investor withdrawals "are driving the high yield market now more than anything. Institutions -- hedge funds and mutual funds -- are being forced to get out and unfortunately that's pressuring the entire market."

Growing tumult in credit markets comes eight years after BNP Paribas SA helped spark a global financial crisis by freezing withdrawals from three investment funds because it couldn't "fairly" value their mortgage holdings.

Debt-laden commodity producers have been some of the hardest hit parts of the junk-bond market this year as prices for everything from oil to steel tumbled on signs of oversupply and weak demand from China. The slump is burning investors who relied on lower-rated bonds to boost returns as the Fed kept its benchmark interest rate near zero since 2008.

Many funds have also taken on greater liquidity risk in their hunt for higher yields. The Third Avenue Focused Credit Fund in many instances had purchased 10 percent or more of smaller bond offerings. Such large positions in infrequently-traded debt can make it difficult to exit. That's particularly been the case in recent months as the aversion to commodities-industry borrowers spread to almost any debt that smacked of risk.

The fund, which had $3.5 billion in assets as recently as July 2014, suffered almost $1 billion in redemptions this year through November. Instead of meeting future withdrawals requests with cash, Third Avenue will redeem the fund's shares for interests in a trust that will hold the focused credit fund's assets -- primarily high yield bonds and corporate bank loans -- and liquidate them over time.

"We're looking at some real carnage in the junk-bond market," Gundlach, whose $51.3 billion DoubleLine Total Return Bond Fund has outperformed 99 percent of peers over the past five years, said during a webcast Tuesday. "This is a little bit disconcerting that we're talking about raising interest rates with the credit markets in corporate credit absolutely tanking."

Next up, dividend stocks?

In addition to junk bonds, the hunt for yield has led retirees, pension funds and other formerly conservative investors to pile into high-dividend stocks like energy producers and pipeline operators, on the assumption that not only would they generate cash in the near-term but they would increase their payouts over time.

Or not.

Kinder Morgan's drastic dividend cut may be followed by others

(Bloomberg) - Kinder Morgan Inc.'s decision to slash its dividend may have been the right one for the pipeline operator, but investors should brace for the possibility that other energy infrastructure companies follow in its footsteps.

Kinder Morgan late Tuesday said it will cut its quarterly dividend by 75%, to 12.5 cents from 51 cents, starting in the fourth quarter, a move it had signaled last week. "(Kinder Morgan's) aggressive dividend cuts will open the door to an entire sector to do the same," analysts at Tudor Pickering Holt said in a note Wednesday.

Other "midstream" energy companies -- those in the business of transporting and storing oil and gas products -- with project backlogs will be considering "a similar 'cut near-term distribution and self-fund' strategy," even though that does not mean the model of distributing all cash flow and relying on new capital to fund growth would change permanently, the analysts said.

Shares closed Tuesday at their lowest since the company's initial public offering in 2011. The stock rose on Wednesday, but that rise barely made a dent on losses of 28% so far this month, and a decline of nearly 60% for the year.

Just as "This time it's different" are the four most dangerous words in finance, "What's going to blow up next?" are the six scariest. When once-burned investors and speculators decide they won't be burned again, markets go risk-off almost instantaneously. Babies get thrown out with the bathwater and it's 2008 all over again.