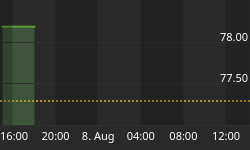

Ten-year Treasury yields jumped 11 bps this week to 2.66%, moving decisively above the key 2.60% technical level - to the highest yields since July 2014. Two-year yields ended the week up seven bps to 2.07%, the high going back to September 2008. Five-year Treasury yields jumped 10 bps to 2.45%, the high since April 2010. Has the long-delayed bond bear market finally commenced - with barely a whimper? Markets fretted over a potential spike in yields over recent years. I suppose You Can Only Worry For So Long.

The S&P500 has gained 5.1% in three weeks. If this return is lacking, one could have made 6.5% in the Dow Transports, 6.9% in the Nasdaq100, 6.8% in the Nasdaq Composite, 7.0% in the KBW Bank index or 9.5% in the Semiconductors (SOX) - all in the 2018's first 13 trading sessions.

With equities deep into parabolic melt-up, let's not expect market participants to be all too fixated on Treasury yields at a mere 2.64%. Why worry over where market yields might be in a few months, not with huge gains to harvest on an almost daily basis in equities markets. No reason to worry about the ECB winding down QE later this year. No basis for fretting a few Fed rate increases spread over many months. Clearly, the Bank of Japan is in no hurry either. Government shutdown - no issue. With tax cuts achieved, gridlock is fine. Liquidity abounds - might abound forever. Meanwhile, the reality is that global bond markets could be ending a three-decade bull market that changed the world.

January 17 - Financial Times (Kate Allen): "Governments are set to increase their borrowing from private investors this year for the first time in four years as central banks step back from the market, underlining market concern that the era of ultra-low bond yields appears vulnerable. The net debt of developed nations is expected to rise this year, chiefly driven by an increase in US bond sales, according to... JPMorgan Chase. The European Central Bank is scaling back its bond-buying programme and the Federal Reserve is shrinking its balance sheet... The Fed is set to roll off $222bn of its holdings of Treasuries this year, the analysis shows, while the ECB's purchases of eurozone sovereign debt will drop to $221bn from $622bn last year. The US will raise a net $828bn of new issuance after the effects of the scaling back of quantitative easing are taken into account, according to JPMorgan — up from $357bn in 2017."

January 16 - Bloomberg (Sid Verma): "A 'dramatic' increase in U.S. bond supply over the next year risks unhinging global markets from their bullish foundations, warns Torsten Slok at Deutsche Bank AG. The supply of U.S. government debt will almost double to $1 trillion this year to finance a widening budget deficit as the Federal Reserve whittles down its holdings. Unless new buyers emerge, the overhang could be far-reaching. 'If demand for U.S. fixed income doesn't double over the coming years then U.S. long rates will move higher, credit spreads will widen, the dollar will fall, and stocks will likely go down as foreigners move out of depreciating U.S. assets,' the chief international economist at the German lender wrote... 'And this could happen even in a situation where U.S. economic fundamentals remain solid.'"

Markets have grown comfortable with uncertainty. I would posit that markets have come to adore myriad uncertainties. After all, they ensure the certitude of interminable aggressive monetary stimulus. As the bullish thinking goes, it's wasted energy to contemplate a spike in yields when, obviously, central banks won't tolerate one. Waiting anxiously to perform another act of heroism, QE can be revived in an instant.

Unless something dramatic transpires, global central bank balance sheet growth will slow significantly in 2018. At the same time, governments are geared up to issue more debt. Central banks accommodated years of ("counter-cyclical") massive deficit spending, and now big deficits are the (structural) norm.

Supply/demand dynamics will be shifting substantially, yet bond prices are expected to adjust slightly. The U.S. will be financing a huge fiscal deficit as the Fed pares back its balance sheet. Moreover, there's an unusual degree of uncertainty surrounding future U.S. fiscal deficits. Tax cuts pay for themselves with bountiful prosperity, or perhaps this a replay of the late-nineties Bubble Mirage that had the U.S. paying off all its debt. There's a scenario - a not outlandish one at that - where the Bubble bursts and deficits skyrocket toward $2.0 TN. For now, there is also the risk of trade battles coupled with a global economic boom and market Bubbles that create unusually uncertain inflation prospects.

Extraordinary: The end of an unparalleled bull market that saw $14 trillion of experimental "money" printing, along with zero/negative rates, push global yields to historic lows, in the face of unprecedented government debt issuance and record corporate debt sales. There is as well the issue of unquantifiable speculative leverage and derivative exposures, along with a now enormous ETF complex untested in bear market dynamics. Reasons aplenty to take a cautious approach with long-term bonds globally.

When it comes to uncertain 2018 prospects, China joins bond yields near the top of the list. Similar to their approach with bonds, equities buyers are today comfortable with China and feel no compunction to ponder beyond the present. Markets over recent years fretted over a Chinese financial accident. I suppose You Can Only Worry For So Long.

January 12 - Reuters (Fang Cheng and Kevin Yao): "China's bank lending halved in December as the government kept up its campaign to curb financial system risks, but banks still managed to dole out a record amount for the year amid the tighter scrutiny. Chinese authorities are trying to walk a fine line by containing riskier types of financing and slowing an explosive build-up in debt without stunting economic growth. Banks extended 584.4 billion yuan ($90.46 billion) in December, data from the People's Bank of China (PBOC) showed..., well below expectations of 1 trillion yuan and November's 1.12 trillion yuan. But banks lent a record 13.53 trillion yuan of new loans in 2017."

Total Social Financing (TSF) dropped in December to a weaker-than-expected 1.140 TN yuan (estimates 1.500), or about $178 billion. This was down 30% from both November and from December 2016. The fourth quarter marked a significant slowdown in TSF. Quarterly growth in TSF averaged 5.216 TN yuan ($815bn) during the first three quarters of 2017, but then dropped to 3.795 TN yuan ($593bn) during Q4. For the year, growth in TSF (which excludes government borrowings) was 9.2% ahead of 2016 levels to 19.443 TN ($3.038 TN). Yet for the first three quarters of 2017 TSF was expanding at a rate 16.3% above comparable 2016. The fourth quarter actually saw the growth in TSF 12.7% below that of Q4 2016.

Financial institution loans to Chinese households surged 21% in 2017, with lending remaining strong through year end. Lending to corporations slowed markedly last year, with December lending half of November's level. Mortgage loans dominate Chinese household borrowings. And with housing prices inflated after years of easy finance, China is becoming increasingly susceptible to a self-reinforcing downturn in both apartment prices and mortgage Credit growth.

China traditionally begins the year with blockbuster Credit growth. January lending data will provide some indication of whether the fourth quarter slowdown was chiefly seasonal or rather the beginning of a more determined effort by Beijing to rein in Credit excess. Chinese regulators this month toughened their crackdown on off-balance sheet "shadow" lending.

January 14 - Bloomberg: "China's banking regulator pledged to continue its crackdown on malpractice in the $38 trillion industry in 2018, vowing to tackle everything from poor corporate governance and violation of lending policies to cross-holdings of risky financial products. The China Banking Regulatory Commission unveiled its regulatory priorities for the year... Inspecting the funding source of banks' shareholders and ensuring they have obtained their stakes in a regular manner. Examining banks' compliance with rules restricting loans to real estate developers, local governments, industries burdened by overcapacity, and some home buyers. Looking into banks' interbank activities and wealth management businesses."

Chinese exports were up 10.9% in December. China ran a $54.69 billion trade surplus in December, the largest since January 2016. Foreign reserves rose to a larger-than-expected $3.140 TN, the highest level in 16 months. Fourth quarter GDP was reported at a stronger-than-expected 6.8% - putting 2017 growth at an above target 6.9%.

Chinese 10-year yields closed Friday at 3.98%, the high going back to October 2014. With the global economy humming along and global finance bubbling along, it's not an inopportune time for Beijing to finally assume an assertive stance in reining in Credit. They will, of course, seek to avoid a shock. Beijing will, as well, focus on assuring productive Credit is readily available to sustain economic expansion. Productive enterprises should be supported, while speculative endeavors will be starved of finance. Easy to plan, not so straightforward to execute (Federal Reserve 1928/29).

"Houses are built to be inhabited, not for speculation," President Xi proclaimed back in October during the 19th Party Congress. The problem is that tens of millions of Chinese have made fortunes in real estate. Hundreds of millions more aspire to. Not only has housing become the epicenter of Chinese speculative excess, mortgage Credit has inflated to the point of becoming a majority of total Credit growth - as well as a prevailing source of finance for the real economy. It all evolved into a full-fledged mortgage Credit Bubble, surely an expanding black hole of malinvestment, fraud and bank losses.

January 19 - Reuters: "China's yuan-denominated outstanding housing loans rose 20.9% from a year earlier to 32.2 trillion yuan ($5.03 trillion) at end-December, China's central bank said... Outstanding individual mortgages at the end of December grew 22.2% to 21.9 trillion yuan..."

January 18 - Bloomberg: "China's home sales surged to a record high last month, despite a prolonged government campaign to curb property speculation. Sales by value, excluding affordable housing, jumped to a record 1.45 trillion yuan ($225 billion) in December, gaining 21% at the fastest pace in six months... Earlier today, home price data pointed to a similar acceleration. The upswing comes even as officials have sought to tame resurgent buying sentiment in a market that's seen home prices skyrocket. The resurgence defies predictions that China's property market will slow amid China's moves to tackle excessive leverage and maintain curbs on purchases."

January 16 - Wall Street Journal - "China's Hot Housing Market Begins to Cool" (Dominique Fong): "China's housing market has defied gravity and government restraints for two years, floating on a tide of bank loans and speculation. Until now. In Beijing and Shanghai—two of the country's largest markets—and other megacities, sales have stalled and prices have dropped, falling slightly in some pockets and dramatically in others. Demand has dried up in these areas as a result of government measures including higher mortgage rates, higher down-payment requirements and limits on buying a second or third home. Would-be sellers are increasingly putting plans on hold in hope that prices will rebound."

January 16 - Reuters: "China's banking regulator chief warned that a 'black swan,' or an unforeseen event could threaten the country's financial stability, official People's Daily reported... Guo Shuqing said that while risks in the financial system are manageable, they are still 'complex and serious.' Since his appointment as the head of the China Banking Regulatory Commission early last year, Guo has introduced a flurry of new rules to reign in lender risks including from curbs on shadow banking activities to the crackdown on loan fraud. Guo said the dangers stem from the pressure of rising bad debt, imperfect internal risk systems at financial institutions, the relatively high levels of shadow banking activities and rule violations."

It's curious to see Chinese housing transactions and prices plateau (in key markets) in the face of rampant mortgage Credit excess. Markets' lack of concern notwithstanding, we can remind ourselves that this is China's first mortgage boom - and a rather long and spectacular one at that. And I'm all too familiar with the view that Beijing is adept at managing oh so many things. Yet they've sure made a historic mess of mortgage finance - the extent of which will begin to surface as soon as lending slows. It's one of history's great ongoing manias, one that these days barely garners attention in The Age of Equities and Cryptocurrencies.

At this point, it's not clear how Beijing possibly succeeds in reining in housing speculation without bursting an epic apartment Bubble (makes bitcoin look so tiny). With global yields on the rise and Chinese regulators on the case, the Chinese apartment market could be a critical development to monitor in 2018. Hard for me to believe there's not a black swan holed up in there somewhere. And that goes for global bond markets as well.

For the Week:

The S&P500 gained 0.9% (up 5.1% y-t-d), and the Dow rose 1.0% (up 5.5%). The Utilities slipped 0.5% (down 5.5%). The Banks gained 1.0% (up 7.0%), and the Broker/Dealers added 0.4% (up 6.5%). The Transports declined 0.6% (up 6.5%). The S&P 400 Midcaps rose 0.7% (up 4.1%), and the small cap Russell 2000 increased 0.4% (up 4.0%). The Nasdaq100 advanced 1.1% (up 6.8%).The Semiconductors surged 3.8% (up 9.5%). The Biotechs added 0.5% (up 6.9%). With bullion down $6, the HUI gold index fell 2.2% (up 2.4%).

Three-month Treasury bill rates ended the week at 140 bps. Two-year government yields rose seven bps to 2.07% (up 18bps y-t-d). Five-year T-note yields gained 10 bps to 2.45% (up 24bps). Ten-year Treasury yields jumped 11 bps to 2.66% (up 25bps). Long bond yields gained eight bps to 2.93% (up 19bps).

Greek 10-year yields fell six bps to 3.80% (down 27bps y-t-d). Ten-year Portuguese yields jumped 19 bps to 1.98% (up 4bps). Italian 10-year yields declined two bps to 1.96% (down 5bps). Spain's 10-year yields fell six bps to 1.44% (down 12bps). German bund yields dipped one basis point to 0.57% (up 14bps). French yields declined a basis point to 0.84% (up 6bps). The French to German 10-year bond spread was unchanged at 27 bps. U.K. 10-year gilt yields were unchanged at 1.34% (up 15bps). U.K.'s FTSE equities index slipped 0.3% (up 0.6%).

Japan's Nikkei 225 equities index gained 0.7% (up 4.6% y-o-y). Japanese 10-year "JGB" yields added one basis point to 0.085% (up 4bps). France's CAC40 increased 0.2% (up 4.0%). The German DAX equities index rose 1.4% (up 4.0%). Spain's IBEX 35 equities index added 0.2% (up 4.3%). Italy's FTSE MIB index rose another 1.4% (up 8.7%). EM markets were mostly higher. Brazil's Bovespa index jumped 2.4% (up 6.3%), and Mexico's Bolsa gained 1.1% (up 0.7%). South Korea's Kospi index rose 1.0% (up 2.1%). India's Sensex equities index surged 2.7% (up 4.3%). China's Shanghai Exchange gained 1.7% (up 5.5%). Turkey's Borsa Istanbul National 100 index added 0.4% (down 0.2%). Russia's MICEX equities index advanced 1.1% (up 8.4%).

Junk bond mutual funds saw outflows of $3.076 billion (from Lipper).

Freddie Mac 30-year fixed mortgage rates gained five bps to 4.04% (down 5bps y-o-y). Fifteen-year rates rose five bps to 3.49% (up 15bps). Five-year hybrid ARM rates were unchanged at 3.46% (up 25bps). Bankrate's survey of jumbo mortgage borrowing costs had 30-yr fixed rates down five bps to 4.28% (up 4bps).

Federal Reserve Credit last week declined $1.1bn to $4.404 TN. Over the past year, Fed Credit contracted $9.2bn. Fed Credit inflated $1.593 TN, or 57%, over the past 272 weeks. Elsewhere, Fed holdings for foreign owners of Treasury, Agency Debt gained $4.0bn last week to $3.356 TN. "Custody holdings" were up $186bn y-o-y, or 5.9%.

M2 (narrow) "money" supply jumped $20.5bn last week to $13.858 TN. "Narrow money" expanded $599bn, or 4.5%, over the past year. For the week, Currency increased $2.3bn. Total Checkable Deposits surged $97bn, while Savings Deposits dropped $74.7bn. Small Time Deposits were little changed. Retail Money Funds declined $3.8bn.

Total money market fund assets dropped $20.1bn to $2.816 TN. Money Funds gained $150bn y-o-y, or 5.6%.

Total Commercial Paper gained $7.5bn to a near five-year high $1.119 TN. CP gained $151bn y-o-y, or 15.7%.

Currency Watch:

The U.S. dollar index slipped 0.4% to 90.572 (down 1.7% y-o-y). For the week on the upside, the Mexican peso increased 2.2%, the South African rand 1.4%, the Australian dollar 1.0%, the British pound 1.0%, the Norwegian krone 0.7%, the New Zealand dollar 0.5%, the Swiss franc 0.5%, the Brazilian real 0.3%, the Singapore dollar 0.3%, the Japanese yen 0.3% and the euro 0.2%. For the week on the downside, the Canadian dollar declined 0.3% and the South Korean won slipped 0.1%. The Chinese renminbi gained 1.01% versus the dollar this week (up 1.60% y-t-d).

Commodities Watch:

The Goldman Sachs Commodities Index slipped 0.6% (up 1.8% y-t-d). Spot Gold declined 0.5% to $1,332 (up 2.2%). Silver lost 0.6% to $17.036 (down 1%). Crude declined 93 cents to $63.37 (up 5%). Gasoline added 0.8% (up 4%), while Natural Gas declined 0.5% (up 8%). Copper fell 1.0% (down 3%). Wheat was down 1.8% (down 1%). Corn jumped 1.8% (up 1%).

Trump Administration Watch:

January 20 - Bloomberg (Laura Litvan, Erik Wasson and Anna Edgerton): "The U.S. government officially entered a partial shutdown early Saturday as Senate Democrats and a handful of Republicans blocked a House-passed bill to fund the government after the two parties failed to break their deadlock over immigration. As the midnight passed, senators kept haggling over whether a funding extension shorter than the four-weeks passed by the House might provide a bridge for negotiations. With Democrats mostly unified in their opposition and defections in the Republican ranks, Senate Majority Leader Mitch McConnell couldn't muster the 60 votes needed to get the temporary funding measure to the floor before the deadline to act."

January 18 - Reuters (Richard Cowan and Susan Cornwell): "The White House on Wednesday threw its support behind a Republican proposal to avert a government shutdown at week's end with a one-month extension in funding, but it was unclear whether there were enough votes to pass it in Congress. Congress has been struggling for months to reach an agreement to fund the government, which is currently operating on its third temporary funding extension since the 2018 fiscal year began on Oct. 1. The latest measure expires on Friday."

January 16 - Wall Street Journal (Andrew Browne): "The last time Washington mobilized for a trade war, Ronald Reagan was president and Japan the adversary. Today, the White House is readying the same big guns—a mix of tariffs and quotas—aimed mainly at Chinese imports. It has in its sights everything from steel to solar panels and washing machines. A record Chinese annual trade surplus with the U.S., announced last week, is the potential catalyst for hostilities after a year of bluster from President Donald Trump. A trade war isn't a certainty, but if it comes, it will look nothing like the battles that raged in the 1980s over Japanese semiconductors, cars and TV sets."

January 18 - Reuters (Jeff Mason): "President Donald Trump said... the United States was considering a big 'fine' as part of a probe into China's alleged theft of intellectual property, the clearest indication yet that his administration will take retaliatory trade action against China. In an interview with Reuters, Trump and his economic adviser Gary Cohn said China had forced U.S. companies to transfer their intellectual property to China as a cost of doing business there. The United States has started a trade investigation into the issue..."

January 19 - Reuters (Michael Martina and Kevin Yao): "As influential voices within the U.S. business community warn China that U.S. President Donald Trump is serious about tough action over Beijing's trade practices, there is little sense of a crisis in the Chinese capital, where officials think he is bluffing. In Beijing, many experts think Washington is unwilling to pay the heavy economic price needed to upset prevailing trade dynamics between the world's two largest economies. Hanging over trade relations are several inquiries into whether steel and aluminum imports... are harming U.S. national security, possible tariffs on imported solar panels, as well as an investigation into potential Chinese abuse of intellectual property."

January 17 - Reuters (Jeff Mason and David Lawder): "U.S. President Donald Trump... said that terminating the North American Free Trade Agreement would result in the 'best deal' to revamp the 24-year-old trade pact with Canada and Mexico in favor of U.S. interests. Lawmakers as well as agricultural and industrial groups have warned Trump not to quit NAFTA, but he said that may be the outcome. 'We're renegotiating NAFTA now. We'll see what happens. I may terminate NAFTA,' Trump said..."

Federal Reserve Watch:

January 19 - Bloomberg (Rich Miller): "Federal Reserve policy makers are openly voicing their willingness to accept above-target inflation even as price pressures are beginning to build. 'Let me be clear: A small and transitory overshoot of 2% inflation would not be a problem," William Dudley, president of the Federal Reserve Bank of New York, said... 'Were it to occur, it would demonstrate that our inflation target is symmetric, and it would help keep inflation expectations well-anchored around our longer-run objective.' Such talk suggests that the central bank won't respond willy-nilly to mounting price pressures with significantly stepped-up interest rate increases."

January 19 - Bloomberg (Jesse Hamilton): "The Federal Reserve is working to relax a key part of post-crisis demands for drastically increased capital levels at the biggest banks, according to people familiar with the work, a move that could free up billions of dollars for some Wall Street giants. Central bank staffers are rewriting the leverage-ratio rule -- a requirement that U.S. banks maintain a minimum level of capital against all their assets -- to better align with a recent agreement among global regulators... The people said the Fed effort is drawing opposition from the Federal Deposit Insurance Corp., an agency with authority over banking rules that's still led by a Barack Obama appointee."

U.S. Bubble Watch:

January 16 - Wall Street Journal (Martin Feldstein): "Year after year, the stock market has roared ahead, driven by the Federal Reserve's excessively easy monetary policy. The result is a fragile financial situation—and potentially a steep drop somewhere up ahead. To deal with the Great Recession, the Fed cut interest rates to a historic low. The short-term federal-funds rate hit 0.15% in January 2009 and stayed there until the end of 2015. In a strategy aimed at reducing long-term rates, the Fed under then-Chairman Ben Bernanke promised to keep short-term rates close to zero until the economy fully recovered. The Fed also began buying long-term bonds and mortgage-backed securities, more than quintupling its balance sheet from nearly $900 billion in 2008 to $4.4 trillion now. Mr. Bernanke explained that this 'unconventional' monetary policy was designed to encourage an asset-substitution effect. Investors would shift out of bonds and into equities and real estate. The resulting rise in household wealth would push up consumer spending and strengthen the economic recovery."

January 19 - Bloomberg (Brandon Kochkodin): "Volatility was one of the never-ending talking points of 2017... The Chicago Board Options Exchange Volatility Index, or VIX, finished the year with the lowest average daily level on record. During the course of the year, we saw the market's fear gauge set a new record low when it closed at 9.14 on Nov. 3. Want more perspective? Try this: Arrange all the trading days this millennium from lowest to highest by the value of the VIX that day. The first 41 entries on that list would all be from 2017! Fully 80 of the top 100 calmest days since the turn of the century were in this past year. It's not as if there wasn't anything to worry about. The Federal Reserve's Partisan Conflict Index, a measure of political disagreements with data stretching back to 1981, hit its highest point on record in March. The country endured the most expensive hurricane season. Threats of a federal government shutdown came and went. Not even a nuclear showdown with North Korea could raise investors' collective pulse."

January 16 - Reuters (Claire Milhench and Marc Jones): "Investors have raised their stock allocations to two-year highs and cut cash positions to five-year lows, with a majority expecting the equity bull run to continue into 2019, a survey by Bank of America Merrill Lynch (BAML) showed..."

January 17 - CNBC (Jeff Cox): "Stock market optimism among professional investors just keeps on surging, and is now at the highest levels since before the crash of 1987. Bullishness, or the belief that the market is heading higher, is now at 66.7% in the latest Investors Intelligence survey, a widely followed gauge of sentiment among investment newsletter authors. That's the highest level since early April 1986..."

January 17 - Bloomberg (Craig Torres): "Almost all of the 12 Federal Reserve districts reported 'modest to moderate gains' in economic activity at the start of 2018, a Federal Reserve survey showed. The central bank's Beige Book economic report... said the Dallas Fed bank was the exception, reporting 'a robust increase.'"

January 17 - Bloomberg (Katia Dmitrieva): "U.S. factory production rose for a fourth straight month in December, capping the strongest quarter since 2010 and underscoring a resurgence in manufacturing that's primed for further advances, Federal Reserve data showed..."

January 16 - Reuters (Uday Sampath and Siddharth Cavale): "U.S. shoppers spent a record $108 billion snapping up discounts on Amazon and other websites during the 2017 holiday season, with more people using smartphones and tablets, Adobe Analytics said... Adobe, which collects its data by measuring 80% of all online transactions from the top 100 U.S. web retailers, said the amount was 14.7% higher than last year's total."

January 16 - Bloomberg (Joanna Ossinger): "Volatility can't stay this low forever -- or so investors have been saying for what feels like forever. They may have finally found their moment. As the market rallies, 'volatility isn't that low anymore,' Pravit Chintawongvanich of Macro Risk Advisors said..., adding that the Cboe Volatility Index (VIX) curve is flattening. The VIX rose as much as 22% on Tuesday to as high as 12.41, the highest level in six weeks. That is still around 30% below the average of 18.1 since the bull market started in 2009. The correlation of S&P 500 Index stocks to each other has been increasing as the market rallies, the reverse of what's typically seen, and this gain over the past two months points to broad buying of equities -- a ''melt up' so to speak,' Chintawongvanich wrote."

January 17 - Bloomberg (Martin Z Braun): "New York City is still reaping the benefits of the real estate boom. The city set a value of $1.26 trillion for its more than one million properties for the fiscal year beginning in July, an increase of 9.4% over the previous period that promises to boost the government's tax collections. 'This year's roll confirms increases in the real estate market and additional construction activity in New York City, which is not just concentrated in Manhattan,' Jacques Jiha, the city's commissioner for the department of finance, said..."

January 17 - Wall Street Journal (Leslie Scism): "Long-term-care insurance was supposed to help pay for nursing homes, assisted living and personal aides for tens of millions of Americans when they became unable to take care of themselves. Now, though, the industry is in financial turmoil, causing misery for many of the 7.3 million people who own a long-term-care policy, equal to about a fifth of the U.S. population at least 65 years old. Steep rate increases that many policyholders never saw coming are confronting them with an awful choice: Come up with the money to pay more—or walk away from their coverage. 'Never in our wildest imagination did we consider that the company would double the premium,' says Sally Wylie, 67, a retired learning specialist..."

China Watch:

January 18 - New York Times (Keith Bradsher): "The pace of growth in China's economy accelerated last year for the first time in seven years as exports, construction and consumer spending all climbed strongly. At least, that's what the government says. In reality, the pace of growth in China's economy is anybody's guess. Various signals suggest China's growth did speed up last year, which could give the government the room it needs to tackle an accumulation of serious financial, environmental and social problems this year... The National Bureau of Statistics announced... that the economy expanded 6.9% last year, up slightly from 6.7% in 2016 and breaking a trend of gradual slowing that began in 2011."

January 18 - Bloomberg: "China home prices rose in the most cities in six months even as the government prolonged its campaign to curb property speculation. New-home prices... in December rose in 57 of 70 cities tracked by the government, compared with 50 in November... Prices fell in 7 cities from the previous month and were unchanged in six."

January 14 - Reuters (Michael Martina): "China will step up oversight in the banking sector this year to reduce financial risks, the country's banking regulator said, stressing that long-term efforts would be needed to control banking sector chaos. The China Banking Regulatory Commission (CBRC) said... that its priorities included increasing supervision over shadow banking and interbank activities. 'Banking shareholder management, corporate governance and risk control mechanisms are still relatively weak, and root causes creating market chaos have not fundamentally changed,' the CBRC said."

January 17 - Bloomberg: "A slump in Chinese government debt may worsen, with inflation picking up as breweries, dairies and others raise prices, and energy costs climb amid a government crackdown on coal. Cui Li, Hong Kong-based head of macro research at CCB International Holdings Ltd., expects inflation to rise to 2.5% this year, a marked increase from 2017 when China's consumer price index averaged 1.6%. 'Food prices will rise, raw material costs are passing through, and pollution curbs have intensified -- I don't think the market has yet fully priced in the impact of inflation,' said Cui. She expects China's 10-year government bond yield to range between 4.3 and 4.5% by the end of the year versus 3.97% Thursday."

January 16 - Bloomberg: "China's central bank boosted injections via open-market operations to the most in two months to counter seasonal tightening of liquidity. The People's Bank of China pumped in a net 270 billion yuan ($42bn) on Tuesday, as sales of reverse-repurchase agreements more than offset maturities. That's the most since Nov. 16..."

January 17 - Wall Street Journal (Nathaniel Taplin): "Why did sentiment on China improve so much in 2017? Progress in taming long-running structural problems, such as the country's excess manufacturing capacity and mushrooming off-balance sheet debt, deservedly caught investors' attention. The driving force behind that progress was the same factor that should now give investors pause: The primacy of Xi Jinping. Mr. Xi's five-year campaign to consolidate power has left him in firm control of China's fractious bureaucracy. He has started to do what his predecessors couldn't, bringing slippery local officials and state-owned banks and firms to heel. But his success entails a sea-change in how to view China: The biggest risk may no longer be a weak Beijing, but a strong Xi administration which local officials are terrified to defy. That brings up ghosts of a darker time."

January 18 - Bloomberg (Denise Wee): "It's been a bad week for bonds of the debt-laden Chinese conglomerate HNA Group Co., with stock trading halts at four units adding to investor concerns. One of the securities sold by HNA Group International Co. that matures in 2019 slid as much as 4.2 cents this week -- the biggest weekly fall in six months -- to a record low of 84 cents on the dollar. The company's bonds due 2021 shed 3.3 cents this week to 79.5 cents, also near the lowest ever."

January 18 - Bloomberg: "A local state-owned company in China's Inner Mongolia, a region that recently admitted having inflated key economic data, has suffered a credit rating downgrade. Fitch Ratings cut Inner Mongolia High-Grade Highway Construction and Development Co.'s long-term foreign- and local-currency issuer default rating to BBB- from BBB, citing the local government's revision of its fiscal figures... That follows its downgrade of an internal assessment of the creditworthiness of the Inner Mongolia region... Investors are growing more concerned about local credit risks as the government steps up efforts to curb leverage and two regions have admitted faking data."

January 15 - Bloomberg: "China is escalating its clampdown on cryptocurrency trading, targeting online platforms and mobile apps that offer exchange-like services... While authorities banned cryptocurrency exchanges last year, they've recently noted an uptick in activity on alternative venues. The government plans to block domestic access to homegrown and offshore platforms that enable centralized trading, the people said... Authorities will also target individuals and companies that provide market-making, settlement and clearing services for centralized trading..."

January 16 - Financial Times (Yuan Yang, Lucy Hornby and Emily Feng): "China is plugging the last holes in its 'Great Firewall' internet censorship apparatus, hampering global groups' ability to operate in the country. Five international companies and organisations told the Financial Times that access to the global internet from their Chinese offices has been disrupted in recent months. Some of the companies blamed Chinese telecoms providers, saying the groups blocked crucial software used to bypass censorship. China aggressively censors the internet, cutting off locals' access to Facebook, Google, YouTube and much more, to control what news and facts reach its population."

Central Bank Watch:

January 16 - Bloomberg (Piotr Skolimowski): "The European Central Bank should adjust its policy guidance before the summer and shouldn't have any problems ending net asset purchases in one swoop after September, Governing Council member Ardo Hansson said... While the Estonian policy maker judged the ECB's current stance as broadly appropriate, he argued... that there was a 'need for action in our communication.' 'There are certainly good reasons to reduce the importance of the net purchases in our communication soon -- also with a view to a potential end to these purchases,' he said. If growth and inflation continue to evolve broadly in line with the ECB's latest projection, it would 'certainly be conceivable and also appropriate to end the purchases after September,' he said."

January 16 - Bloomberg (Jana Randow): "Bundesbank President Jens Weidmann said that analysts' expectations that European Central Bank interest rates won't rise before the middle of next year are reasonable. 'Those expectations seem to be grosso modo in line with the current forward guidance of the ECB Governing Council, which says that interest rates will only increase well beyond the end of net asset purchases,' he said..."

January 17 - Bloomberg (Piotr Skolimowski and Alessandro Speciale): "The European Central Bank's second-highest official waded into the debate over euro-area monetary stimulus after some policy makers expressed concerns over the single currency's recent gains. Vice President Vitor Constancio cast his lot with Governing Council members Francois Villeroy de Galhau and Ewald Nowotny, who argued over the past two days that a stronger euro may harm ECB efforts to return inflation to the goal of just under 2%."

January 14 - Reuters (Leika Kihara and Stanley White): "Bank of Japan Governor Haruhiko Kuroda offered a positive view on the economy and inflation..., sending the yen to a four-month high against the dollar on simmering speculation it may exit its ultra-loose monetary policy earlier than expected. Financial markets ignored Kuroda's reminder that the BOJ will maintain its massive stimulus in a sign of how nervous investors have become on when it might follow the footsteps of other central banks in dialing back crisis-mode stimulus."

January 17 - Reuters (Balazs Koranyi and Jan Strupczewski): "Euro zone officials could pick a new European Central Bank vice president within weeks, kicking off two years of flux at the top of one of Europe's most vital institutions and previewing a tussle to replace ECB chief Mario Draghi in 2019. Germany is seen as eager to claim the presidency at last, two decades after the ECB's creation, but the hawkish views of its obvious candidate, Bundesbank chief Jens Weidmann, will count against him in some member states, euro zone sources say."

January 14 - Reuters (John Revill and Angelika Gruber): "Three years after the Swiss National Bank shocked currency markets by scrapping the franc's peg to the euro, it faces the toughest task of any major central bank in normalising ultra-loose monetary policy. If it raises rates, the Swiss franc strengthens. If it sells off its massive balance sheet, the Swiss franc strengthens. If a global crisis hits, the Swiss franc strengthens. And the abrupt decision to scrap the currency peg on Jan. 15, 2015, means it still has credibility issues with financial markets."

January 19 - Bloomberg (Masaki Kondo): "Investors in Australia's bonds are boosting bets the central bank will join its global peers in shifting toward a more hawkish policy stance. The extra yield on the nation's benchmark three-year bonds over the central bank's overnight cash rate jumped to 75 bps Friday, the widest since May 2010. Retail sales and employment both grew at more than twice the pace economists predicted, according to the latest data published this month."

Global Bubble Watch:

January 17 - Bloomberg (Daniel Moss): "This is going to be an exciting year for monetary policy. In fact, it already is, thanks to Europe and Japan. Investors were taken aback last week when the Bank of Japan bought fewer bonds and the European Central Bank revealed -- shock, horror -- its language would have to evolve with the euro region's economy. Both developments, and the reaction, were welcome. They say a lot about the strength of global growth and how it still surprises many people... The next potential flashpoint is the Jan. 25 meeting of the ECB's governing council. It's too soon to expect a shift in communications then, but individual council members are off and running."

January 19 - Financial Times (Gillian Tett): "The $160bn Bridgewater hedge fund produced a chart last year about modern politics that was alarming for at least two reasons. First, the number crunching revealed that the proportion of votes garnered by populist, anti-establishment candidates in the west, such as US President Donald Trump, France's Marine Le Pen and Jeremy Corbyn, leader of the UK Labour party, exploded from 7% in 2010 to 35% in 2017. Second, the chart showed that the only time an increase of this magnitude occurred in recent memory was in the 1930s, when another financial crisis led to populism. That time, the swing prefigured the rise of nationalism and led to war. Could history repeat itself? The global elite increasingly fears so. The World Economic Forum on Wednesday released its annual survey of the main concerns of its members."

January 17 - Bloomberg (Adam Haigh): "One of the world's largest money managers says you should fear the lack of fear in markets. Investors in global equities are enjoying the best start to a year in at least three decades, cutting back on cash positions and plowing more money into riskier assets. However, just as many expect this bull run to last even longer than previously expected, Pacific Investment Management Co. says now is the time for caution. 'The fact that the fear is gone is the main reason why we should be worried,' Joachim Fels, a global economic adviser at Pimco, told Bloomberg... 'That means most investors are now pretty fully invested and that means they will want to get out if the markets start to correct -- exacerbating the downdraft."

Fixed Income Watch:

January 18 - CNBC (Patti Domm): "The bond market is in the process of making an important move, and stock traders are keeping a wary eye on it. On Thursday afternoon, the benchmark 10-year Treasury yield crept close to 2.63%, a level it came near last year but has not really traded above since 2014. The yield was above 2.62% in afternoon trading Thursday. 'The pain point comes at 2.63%, where everybody believes that's the breakout, and everyone will be keying on that,' said Art Hogan, chief market strategist at B. Riley FBR. 'This is a more-than-three-year range that we're attempting to break out of here.'"

January 16 - Financial Times (Roger Blitz, Leo Lewis and Robin Harding): "Global bond investors are casting a nervous eye at Japan. As a wave of selling washed across debt markets last week, the disclosure that the Bank of Japan had trimmed the volume of longer bonds it purchased was seized upon as the trigger for a move higher in yields that prompted veteran investor Bill Gross to again call the end of the three-decade bull run for the $14tn US Treasury market. The intense interest in a standard operation in the BOJ's quantitative easing programme revealed how sensitive investors are to any perceived changes at a juncture when the European Central Bank is halving its monthly bond buying and the Federal Reserve is tightening policy... Bret Barker, a portfolio manager with asset manager TCW, says the blowback into the US Treasury market reflects how central bank easing through the BoJ targeting a zero yield for the 10-year Japanese government bond, as well as debt purchases and negative rates from the ECB, has acted as an anchor for global interest rates. 'If those anchors are released...that should increase volatility and raise longer rates in the US,' he says."

January 17 - Bloomberg (Sophie Caronello): "China and Japan's combined share of Treasuries fell to about 36% of all foreign-held U.S. government debt in November, the lowest level in about 18 years. China, the biggest foreign holder of U.S. bonds, notes and bills, saw its total drop 1.1% to $1.18 trillion from the previous month... Japan's holdings dropped 0.9% to $1.08 trillion, the lowest in more than four years."

January 16 - Bloomberg (Carrie Hong, Annie Lee, Lianting Tu, and Narae Kim): "The boom in Asia's dollar bond market is ratcheting up a notch, with investors placing orders for five times as much debt as has been sold so far this month. Chances of a steeper path higher for global interest rates that's lifted government bond yields this year is doing little to damp the appeal for debt from Asian companies outside Japan. The ferocious appetite in 2017, in part due to the hunger from investors chasing higher yields, is extending into January with Chinese property companies finding a flurry of buyers wanting to get their hands on newly issued debt... After a record $322 billion of dollar bond issuance from the region in 2017, Asian firms are off to the strongest ever start to a year. Year-to-date sales have reached $19.3 billion..."

Europe Watch:

January 18 - Bloomberg (Alessandro Speciale, Piotr Skolimowski, and Carolynn Look): "Jens Weidmann hit back at criticism of Germany's current-account and budget surpluses by International Monetary Fund Managing Director Christine Lagarde, saying that increasing public spending would be the wrong way to go. The Bundesbank president kicked off a joint conference by the two institutions by insisting that Europe's largest economy doesn't need more expenditure, though he agreed that it should be better planned. Public outlays should shift away from consumption and toward targeted investment, he said."

January 14 - Bloomberg (Jeff Black, Stephen Engle, and Enda Curran): "Germany's central bank has decided to include the Chinese yuan in its own reserves, in a further boost to the international status of the currency. ...Bundesbank board member Andreas Dombret said the decision was taken last year following an investment of 500 million euros ($611 million) by the European Central Bank... 'The renminbi is used increasingly as part of central banks' foreign-exchange reserves -- for example, the ECB included the RMB but also other European central banks did so,' Dombret said..."

Japan Watch:

January 19 - Reuters: "The Japanese government raised its assessment of the economy in January for the first time in seven months due to rising consumer spending, an encouraging sign that inflation could start to pick up this year. 'Japan's economy is gradually recovering,' the Cabinet Office said... That marked an upgrade from December, when the Cabinet Office said the economy is on a recovery path. The government also raised its assessment of consumer spending for the first time in seven months after retail sales, household spending, and new car sales gained momentum towards the end of last year."

January 14 - Wall Street Journal (Megumi Fujikawa and Suryatapa Bhattacharya): "The Bank of Japan, after goosing Japanese share prices with a $50-billion-a-year program of stock purchases, now confronts a decision facing many other developed country central banks: when to stop. The Nikkei Stock Average, standing near a 26-year high, doesn't seem in need of special help anymore, and critics say the BOJ's buying distorts the market. The Nikkei has more than doubled in the last five years and is up 24% from a year ago. Yet central-bank officials worry that a premature pullback could send the wrong message by suggesting that the BOJ has given up its commitment to reaching 2% inflation."

January 16 - Bloomberg (Netty Idayu Ismail): "A minor tweak in the Bank of Japan's bond purchases has emboldened investors to bet the central bank is about to wind back monetary stimulus. Going long on the yen is the biggest currency wager for AMP Capital Investors Ltd.'s Nader Naeimi... Options traders are the most bullish on the yen among developed-market currencies. Japan's longest stretch of economic growth in two decades is fueling bets the BOJ will join its global peers and begin normalizing policy as soon as this year. The central bank cut purchases of longer-maturity bonds last week, prompting speculation it will allow 10-year yields to rise above its current target of around zero percent."

January 18 - Bloomberg (Toru Fujioka and Masahiro Hidaka): "A small shift is taking place in internal discussions among Bank of Japan policy makers, with a minority raising the need to eventually start discussing policy normalization, even though they agree the current stimulus program must continue unchanged for some time... Some of them think the change is natural given the improvement in the economy, according to the people, who declined to be named because discussions are private. Japan's extended economic recovery and a slow but steady rise in inflation are creating the need in the medium-term to at least begin talking about normalization, the people said."

January 16 - Bloomberg (James Mayger, Connor Cislo, and Maiko Takahashi): "One of Japan's key targets for addressing its ballooning debt is set to be pushed further into the future when the Cabinet Office updates economic forecasts next week. The primary balance, which measures the government's fiscal position excluding interest payments on its borrowings, was meant to come out of the red in fiscal 2020. Reaching the goal was seen as a first step for Prime Minister Shinzo Abe's administration to arrest debt growth... Yet a best-case projection for a primary balance surplus was reset to 2025 in a revision last year and now it's going to be deferred again, until sometime in the late 2020s..."

Leveraged Speculation Watch:

January 14 - Bloomberg (Nishant Kumar): "Cheese, sunflower seeds and rough rice sounds like an unappetizing mix -- unless you happen to be a hedge-fund manager. A handful of computer-driven funds had a bumper 2017 by betting on the future price of such 'exotic' assets. The success of this type of managed futures strategy, the industry's term for trend-following, is now drawing new entrants despite the risks created by the low levels of liquidity. Hedge funds returns have been battered by central bank monetary policies that have made it more difficult for them to outperform the market... That's prompting some trend followers to move into less crowded markets such as over-the-counter securities, electricity and coal."

Geopolitical Watch:

January 15 - CNN (Emma Burrows, Angela Dewan and Lindsay Isaac): "Russian Foreign Minister Sergey Lavrov has accused the United States of destabilizing the world, airing a list of grievances over the Trump administration's foreign policy. Lavrov dedicated the opening of his annual press conference... to castigating the US, which is expected to soon issue a fresh round of sanctions against Russia over its interference in the 2016 US election. Russia has long denied meddling in the vote. Lavrov criticized the US for issuing regular 'threats' in relation to events in North Korea and Iran, saying they had 'further destabilized' the global situation."

January 13 - Reuters (Andrey Ostroukh): "Iran said... it would retaliate against new sanctions imposed by the United States after President Donald Trump set an ultimatum to fix 'disastrous flaws' in a deal curbing Tehran's nuclear program. Trump said... he would waive nuclear sanctions on Iran for the last time to give the United States and European allies a final chance to amend the pact. Washington also imposed sanctions on the head of Iran's judiciary and others. Russia - one of the parties to the Iran pact alongside the United States, China, France, Britain, Germany and the European Union - called Trump's comments 'extremely negative.'"

January 16 - Newsweek (Jack Moore): "Iran has condemned the U.S. plan to create a 30,000-strong force inside Syria to protect territory held by the Kurdish-Arab coalition that helped oust the Islamic State militant group (ISIS) from most of northeastern Syria. The U.S.-led coalition worked with the Syrian Democratic Forces (SDF), made up of the Kurdish People's Protection Units (YPG) militia and Arab militiamen, to defeat ISIS in Raqqa. Now, Washington is working with the SDF to create the force to secure territory along the northern Syrian border in Turkey."

January 16 - Voice of America (Dorian Jones): "Turkish President Recep Erdogan... stepped up threats to launch a cross-border operation against the Syrian Kurdish militia known as the YPG, which the U.S. backs in the war against Islamic State militants. Ankara sees the YPG as a terrorist organization linked to an ongoing Kurdish insurgency in Turkey. Erdogan used his weekly parliamentary address to his ruling AK Party supporters to say the operation could be imminent. 'Tomorrow, or the day after, or within a short period, we will get rid of terror nests one by one in Syria, starting with Afrin and Manbij,' Erdogan said."