Yieldcos have been, in theory, great tools for financing clean energy projects with cheap stock market capital from a wide pool of investors; but then they got too greedy and the bubble burst.

Now, two years later, they’re back—but this time they’re all grown up and they’re no longer destructively selfish.

So far, this has been a major deal-making year for yieldcos, and buyouts have been the buzzword. Larger yieldcos that have had time to grow are now buying up the smaller ones, and things are looking pretty good in this space.

So what exactly is a yieldco?

Yieldcos are the best way for dividend-focused investors to benefit from the renewable energy trend because you get exposure with few surprises.

A yieldco is a dividend growth-oriented public company that is created by a parent company in a set-up that bundles renewable or conventional long-term contracted operating assets to generate consistent, predictable cash flow. Cash available for distribution each quarter, or year, is allocated to shareholders as dividends.

(Click to enlarge)

When the first yieldco went public in 2013 it was sort of revolutionary, and those that followed have been “reshaping the market for operating renewable energy assets, especially wind and solar PV farms”, according to Dr. Tom Konrad, one of the most well-known voices on income-oriented green stocks, and the editor of AltEnergyStocks.com.

But there was another perception, too: One that thought yieldcos looked more like Ponzi schemes than renewable energy market saviors. Perhaps it was a bit unfair.

Konrad called it a “weird trick”: Yieldcos could grow dividends at double-digit rates even though they had no internal growth or retained earnings. But that trick only works if its stock price is rising so it can sell at higher valuations and increase the money invested per share.

The accounting practices of yieldcos, and what is seen as a conflict of interest in the form of purchasing assets from their own sponsors, make some nervous. But not enough to stem the tide of investment in these new vehicles that spin off assets from larger, parent companies. Related: The Ten Greatest Investments In History

They aren’t Ponzi schemes, but they did get too greedy between 2013 and 2015, says Konrad, and SunEdison’s 2016 bankruptcy made Wall Street unfriendly. Between 2013 and 2015, yieldcos managed to raise only $12.5 billion in capital—collectively. The low intake had a snowball effect, with yieldcos downsizing their future dividend estimates and then investors responding by lowering demand. Then stock prices lower and the vicious cycle spirals out of control.

The emperor was outed for having no new clothes.

But that doesn’t mean the model is broken, and it’s still a good idea for investors who want reliable revenue from long-term utility contracts, says Konrad.

Five of the most notable yieldcos, both for their success and lessons learned, include:

#1 NextEra Energy Partners LP (NYSE:NEP)

One of the biggest successes in this field and the top performer, NEP has seen a 116 percent dividend growth and over 70 percent total return since its June 2014 IPO. It’s financially supported by parent NextEra Energy (NYSE:NEE).

#2 TerraForm Power (NSDQ:TERP) and TerraForm Global (NSDQ:GLBL)

TERP and GLBL were unfortunate enough to have been spun off of parent SunEdison, which filed for bankruptcy and got both of its Yieldcos caught up in an accounting mess and legal disputes.

The TerraForm yieldcos were acquired from SunEdison by Brookfield Asset Management Inc (NYSE:BAM) in 2017, for a combined value of $2.49 billion.

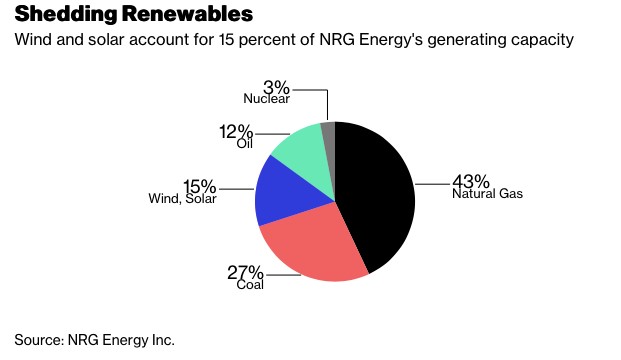

#3 NRG Energy (NYSE:NRG)

Earlier this year, NRG sold its sponsorship stake in NRG Yield (NYSE:NYLD and NYSE:NYLD/A) to Global Infrastructure Partners (GIP). This was a $2.8 billion divestment, and wind and solar accounted for 15 percent of NRG’s generating capacity.

(Click to enlarge)

#4 8Point3 (NSDQ:CAFD)

8Point3 was formed by First Solar Inc. and SunPower Corp., and while its market value was $1.1 billion, Swiss asset manager Capital Dynamics AG said in early February it had agreed to buy it for much less--$977 million.

Related: The Fastest Growing Countries In Emerging Europe

So, welcome to round two of the Yieldco experiment, and this time around the ride should be a much smoother one.

And the benefits are pretty sound. These are corporate entities that hold and generate additional value from operating assets and they’ve got only one layer of taxation because accelerated depreciation benefits of renewable energy assets offset corporate-level tax. In other words, they’re only taxed on distributions to shareholders, much like an MLP (master limited partnership).

Yieldcos may be just the vehicle to gain in popularity at a time when the markets are volatile and correcting and uncertainty has investors looking for safer opportunities. From a financial perspective, buying renewable projects is like purchasing a bond, which makes these stocks safer relative to commodity-driven stocks, such as oil producers.

If it’s dividends you’re after, Yieldcos may be a good way to get into renewables because the projects are typically backed by long-term power purchase agreements.

In the meantime, the Yieldco space seems to be maturing with smart buyouts, according to Konrad, and the original Yieldco model is being tweaked positively.

By Tom Kool for Safehaven.com

More Top Reads From Safehaven.com: