With $600 billion in global remittances at stake, the technology behind how people the world over move their money has never been so crucial—and at this very moment, we’re on the edge of a showdown between banks and fintech start-ups that could see some other tech giants weigh in as the kingmakers.

Global remittances—the money people send home from abroad—are a huge and growing market segment.

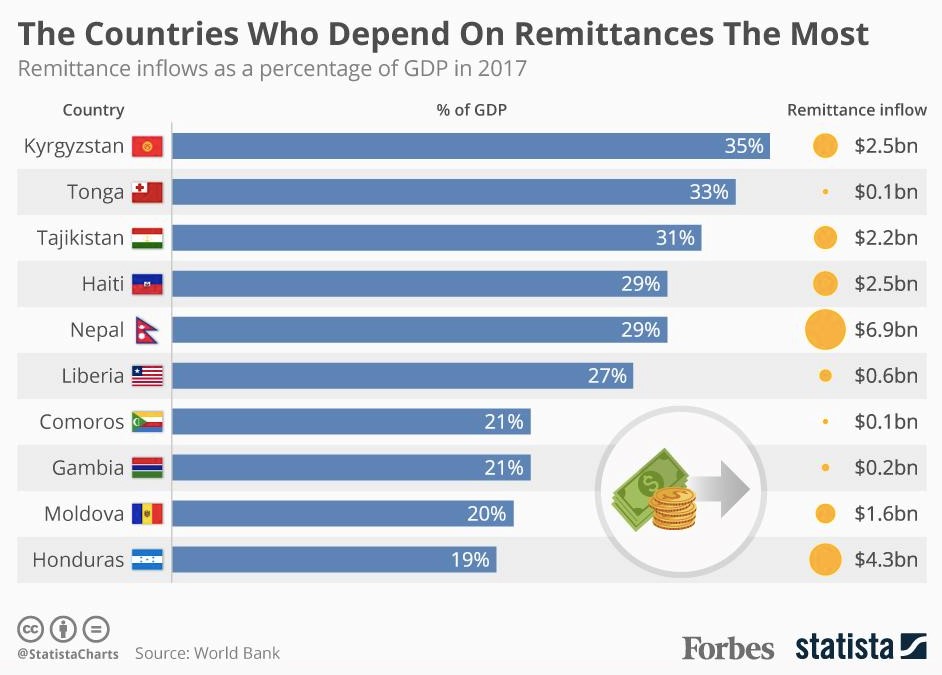

In 2016, these remittances totaled $573 billion. Last year, they hit $613 billion—a 7-percent increase over the previous year, according to the World Bank. For 2018, global remittances are expected to grow another 4.6 percent, reaching $642 billion.

(Click to enlarge)

According to a new Moody’s Investors Service released Wednesday, the average cost of sending $200 across borders last year was 7.2 percent. That’s a rate worth getting excited about for banks, but fintech start-ups are threatening the banking laggards.

A rate of over 7 percent for a cross-border transaction means that this playing field is wide open for anyone savvy enough to jump on the tech train and undercut the competition.

This game is already very real, and Moody’s says the winners will be those who embrace the digital revolution in fintech the fastest, asserting that “the bank of the future” will thrive by catering to customers’ evolving digital expectations.

“Customers will gravitate to providers that best meet their demands for convenience, personalization and affordability, with privacy and data security a growing competitive differentiator,” Moody’s said in a news release. Related: PayPal On Edge As FinTech Startups Gain Momentum

Right now, this playing field has three types of players and potential players: banks themselves, fintech startups like Square, Alipay and WeChat Pay, and big consumer tech companies like Google, Apple and Facebook.

The first might be taking their banking status for granted, even in this fast-moving digital age. The second are already severely threatening banking’s hold on global remittances. The third haven’t really entered the game but are surely eyeing the $600-billion-plus opportunity as tech giants.

Banking laggards will be left behind quickly.

“Agile incumbent banks, that consistently assert digital leadership, will thrive and prosper, while laggard banks that lack the vision or resources to develop competitive digital strategies will be disrupted,” Moody’s noted.

In the meantime, startups like Square have jumped in to fill the gaps by offering more customer-focused, responsive and efficient channels for remittances.

“In the face of these threats, successful incumbent banks will be those that, either on their own or in collaboration with others, pursue aggressive digital transformation to become more efficient and responsive to evolving customer demands,” Moody’s analyst Fadi Abdel Massih said in a statement. Related: Japan Looks To Break Its Addiction To Cash

So the one way that big banks can face off against these strappy fintech startups, the suggestion seems to be, is to work in collaboration with a tech giant—like Google, Apple or Facebook.

The name of the game right now is disruption, and everyone will be watching movements on this $600-billion segment very closely.

The first recent sign of this was Walmart’s April announcement with MoneyGram International that they would be rolling out “Walmart2World” service, a low-cost international money transfer service aimed at taking a slice of the remittances pie.

If Moody’s is right, other deals like this should follow quickly because it’s a market segment too big to pass up. But where are the banks?

By Michael Kern for Safehaven.com

More Top Reads From Safehaven.com:

{kind=link}