Drawn in by the lure of higher yields and floating interest rates, U.S. investors have been throwing money at heavily indebted companies thus fueling explosive growth in leveraged loans as an asset class.

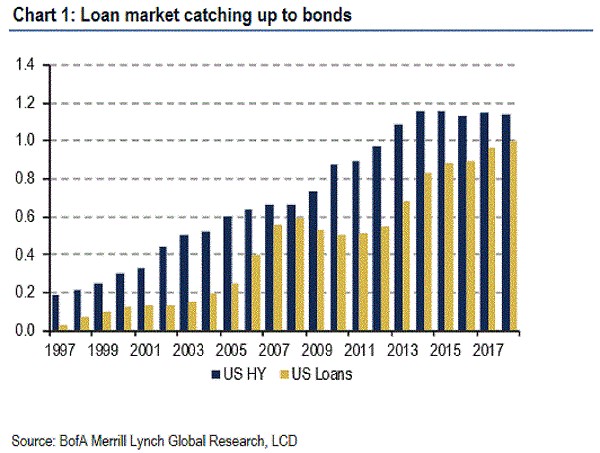

The leveraged loan market has more than doubled since the financial crisis of 2008, exceeding $1 trillion and nearly catching up to the high-yield bond market. Levered loans expanded at a brisk 49-percent clip in 2017.

A good 15 percent of these risky loans are in the hands of mom-and-pop investors from near zero in 2010. Regulators are worried that excessively leveraged financial markets increase their risk of default that could hurt these investors in a market downturn.

(Click to enlarge)

Source: Bloomberg

Like their junk bond cousins, leveraged loans provide private equity firms and companies with shaky credit money to do things like pay dividends, refinance borrowings, fund corporate buyouts and so on. The loans are negotiated lending agreements between large banks and corporate entities and are usually secured using company assets such as property and equipment.

The word “leveraged” refers to the fact that the loans are made to heavily indebted and junk-rated companies. These banks then syndicate or chop up the loans and sell them to retail investors, hedge funds, mutual funds, pension funds and insurance companies.

Leveraged loans are highly profitable to banks, which is the reason why in the past they have been pushing back hard on any proposed tightening of restrictions.

But the bonanza now looks set to continue under president Trump's administration. The president has plans to ease restrictions that curb lending by regulated banks. Such a move will put the U.S. at odds with Europe, where regulators have been doubling down on lending restrictions.

Smoke and Mirrors

(Click to enlarge)

Source: Bloomberg

Leveraged loans have outperformed junk bonds in the year-to-date, returning 1.9 percent vs. 0.3 percent by high-yield credit. This has resulted in a situation where money has been flowing out of bonds and into the leveraged loans market.

Leveraged loans typically pay higher interest rates to reflect the risk of lending to an already indebted company. These contracts typically have floating rates--something investors love because it provides them with an opportunity to escape the negative effects of rising interest rates. Related: The Worst Trades In History

Unfortunately, floating rates are not always what they are cracked up to be, and pricing these contracts is frequently an exercise in smoke and mirrors.

Contrary to what many investors think, the coupon that leveraged loans pay is based not on Treasury rates but rather on Libor (London Interbank Offered Rate)--the notorious interbank lending rate that is frequently manipulated--and also a contractual spread over Libor.

In fact, yields for leveraged loans have not kept up pace with 10-year Treasury yields with the latter climbing significantly faster. As investor appetite for junk loans grows, the spread that borrowers have to pay has been shrinking. Companies have been taking advantage of falling spreads to refinance earlier loans.

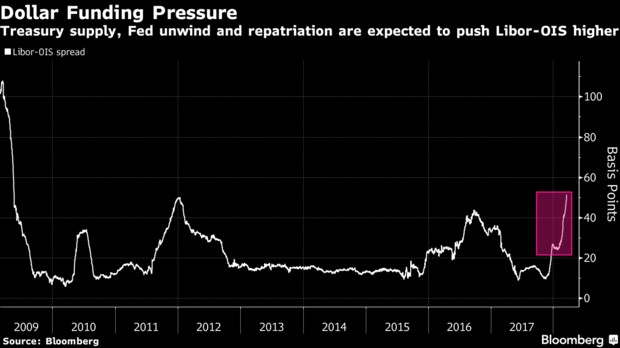

Credit Risk

Another red flag--rising borrowing rates. Short-term borrowing costs in the U.S. have climbed to their highest level since 2008, while widening LIBOR–OIS spreads indicate potential risks within the credit markets.

The Libor-OIS spread provides a gauge of credit market conditions, with high spreads signaling stress in the financial markets. The spread has widened dramatically since the February 8 Congressional deal on the U.S. debt ceiling.

(Click to enlarge)

Source: Bloomberg

By Fred Dunkley for Safehaven.com

More Top Reads From Safehaven.com: