The massive Equifax data breach exposed another growing menace in cyberworld and the need to keep an eagle eye on your finances-- identity theft. Fraudsters purporting to be Equifax employees would place fake calls, social media posts, texts and email to unwitting customers in a bid to steal their personal details including addresses, birth dates, Social Security numbers and driver’s license numbers.

Some 15.4 million Americans fell victim to identity theft in 2017 with the average victim losing $1,038 for a cumulative total of $16 billion.

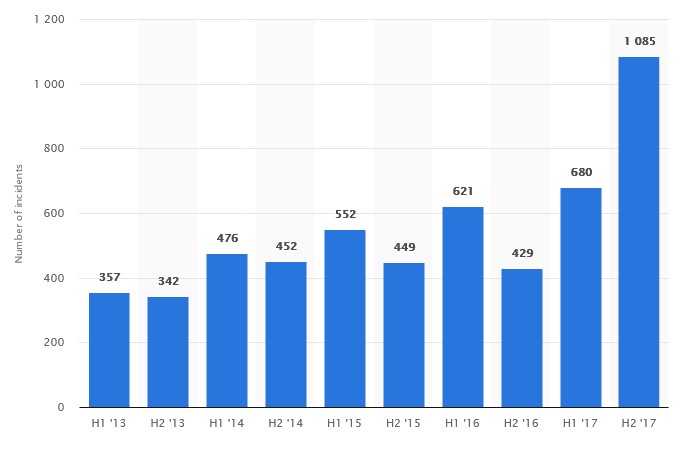

(Click to enlarge)

Source: Statista

But the problem is hardly confined to the U.S. and other developed markets. Stolen and forged identities is becoming a big problem in the fledgling ecommerce markets of emerging economies in Latin America, Asia and Africa.

According to threat solutions company ThreatMetrix, fraudsters have been hijacking identities to open new accounts and using them in fraudulent activities.

Identity-based attacks have increasingly been originating from Brazil, Egypt, Ukraine, Vietnam and South Korea, with 280 million bot-based attacks targeting global ecommerce websites coming from the countries.

Attacks on mobile accounts soared during the first quarter of 2018 after climbing 150 percent.

Related: The Hundred Trillion Dollar Global Debt Crisis

Kenya has also emerged as an economic crime hotspot with the country's stock market regulator Capital Markets Authority (CMA) reporting that hackers have been stealing client information and using it in fraud.

Attacks Getting More Sophisticated

Many Americans are well acquainted with credit card theft with nearly half reporting at least one such incident over the past five-year period. What you might not know is that your credit card information can be stolen from right under your nose without your card ever leaving your possession.

In many instances, credit card thieves don't steal your credit card directly from you but rather from someone along the card processing chain in a particularly egregious form of crime known as “card-not-present” fraud.

Thieves can get hold of your credit card information through one of several methods including:

• Hacking into businesses which handle credit card information

• Using a credit card skimmer to capture your information usually at the point of sale

• Installing viruses and malware in your computer

• Good old-fashioned dumpster diving

Once the thieves get your credit card information, they can use it to make online purchases, create a clone of your card or simply sell it. A thief who uses the information to open a new cellphone or TV service is likely to do plenty of damage to your credit score with the victim remaining oblivious to the incident.

Related: Stock Bulls May Be Preparing For A Break Out

Account takeover fraud--a type of fraud where thieves use stolen information to access your account--was one of the fastest growing categories of cybercrime after recording a 31 percent increase in 2017.

Meanwhile, intermediary new-account fraud has exploded in recent times, with 1.5 million attacks reported in 2017--a 200 percent increase compared to the previous high in 2015.

This type of fraud is becoming a big threat in P2P payments and involves fraudsters who monetize compromised existing accounts to facilitate moving money out of the victim's account.

Other types of account takeovers such as loyalty/reward account theft, brokerage account heists and crytpowallet hijacking have also been increasing rapidly.

By Alex Kimani for Safehaven.com

More Top Reads From Safehaven.com: