U.S. equity futures are flat, alongside European and Asian stocks as global markets recovered some ground on Tuesday after oil prices stabilized and as trade war fears subsided with attention still squarely focused on Trump's Putin summit, even as global tech stocks, Nasdaq futs and FAANGs - or is that FAAGs now - felt the pressure from yesterday's NFLX earnings bomb. The dollar rebounded from overnight lows if still down for the 4th day ahead of a bevy of earnings and before Fed Chair Jerome Powell's much-anticipated testimony to the U.S. Congress.

The MSCI’s world equity index was broadly unchanged, with energy companies in Europe and Asia recovering ground from early losses caused by the previous day’s turbulence in commodity markets. Brent crude initially fell for a second day after a 4 percent slump on Monday, as Libyan ports reopened, and traders eyed potential supply increases by Russia and other producers, but they recovered to trade up 0.5 percent.

(Click to enlarge)

Europe's Stoxx 600 Index was up 0.1 percent with miners outperforming while telecommunications and utility shares fell. In Europe, technology stocks fell 0.4 percent, tracking the decline in Nasdaq futures which were hit after Netflix reported a shocking miss and sharp drop in subscriber growth.

"It’s been a fairly sluggish and unexciting start to the week for markets. Whether things get more interesting or not probably depends on what Fed Chair Jerome Powell has to say when he testifies today in front of the Senate Banking Committee," said DB's Craig Nichol.

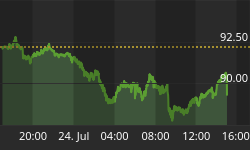

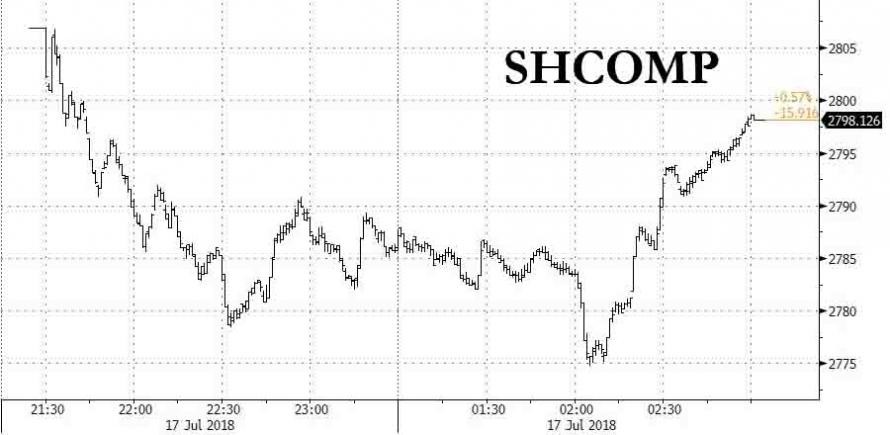

Earlier in Asia, the MSCI index of Asia-Pacific ex-Japan fell 0.4 percent, ending two days of gains amid concern over growth in China. Japanese stocks outperformed in Asia, helped by the yen which held close to its weakest level since January. The Shanghai Composite resumed its slide, and despite a last hour rescue attempt, ostensibly by the National Team, it still closed below 2,800 for the first time since July 11.

(Click to enlarge)

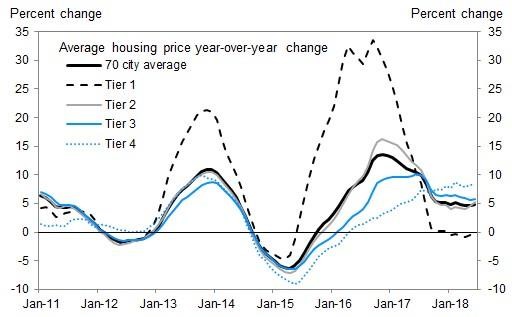

Overnight, China's NBS reported 70-city housing price data which showed that average commercial home price appreciation was 0.8 percent in June, the fastest pace of appreciation since October 2016. Out of the 70 cities NBS monitors, more cities saw housing prices increase in June compared with May.

(Click to enlarge)

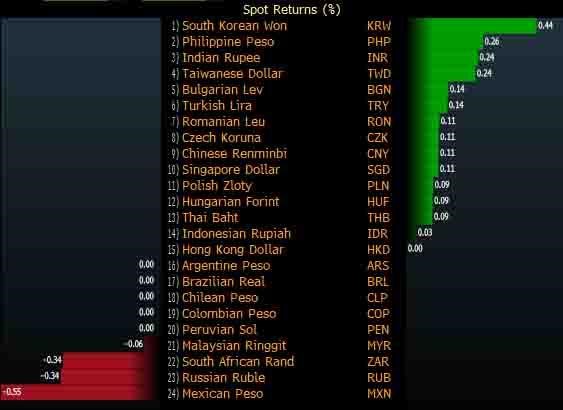

The barometer of Chinese risk sentiment, the Yuan, initially rose despite the PBOC fixing the currency lower by 0.09 percent to 6.6821, the lowest in 11 months, and below the consensus estimate, however it since gave up much of the gains and tracking the late session dollar strength, slid back to 6.7. The yuan also declined against a trade-weighted basket of currencies to the lowest since Dec. 20 amid signs of a slowing economy.

(Click to enlarge)

The Bloomberg Dollar Spot Index fell for a fourth day, while European sovereign bonds were mixed. The DXY index fell 0.1 percent against a basket of six major currencies to 94.409. The index shed 0.25 percent on Monday, nudging away from a two-week high of 95.241 on Friday. The pound advanced after the UK announced record-high employment, raising the odds of an August interest-rate hike by the Bank of England despite the escalating political crisis which threatens to sweep Theresa May from power. The New Zealand dollar jumped after the central bank’s core inflation measure accelerated at the fastest pace in seven years.

Emerging market stocks headed lower for a second day, while their currencies climbed.

Earnings and the Fed are the key remaining catalysts for market sentiment this week, a welcome respite from a background of deteriorating trade relations between the world’s biggest economic powers, at least until Trump's next unexpected tweet. Company results have been mixed thus far, with Deutsche Bank and Bank of America beating estimates, counterbalancing misses by Netflix and Wells Fargo reading.

Today, Fed chair Jerome Powell will testify on the economy and monetary policy before the U.S. Senate Banking Committee and the House of Representatives Financial Services Committee on Wednesday. As outlined in the Fed's monetary policy report released on Friday, he will reiterate the Fed’s stance towards gradual monetary policy tightening. Markets will focus on his views on recent trade tensions.

Some were hawkish: "In short, we expect the chairman to signal optimism on growth and inflation, consistent with continued ‘gradual’ tightening. He will undoubtedly acknowledge some downside risks associated with the administration’s trade warmongering, but he will likely try to avoid sounding critical of the administration" wrote Jim O’Sullivan, chief economist at High Frequency Economics.

Others expected a dovish surprise: "It’ll be a tricky day at the office for Fed Chair Powell, but given the external challenges facing the U.S. economy, it’s hard not to see a more cautious policy being struck today,” said Viraj Patel, currency strategist at ING Groep NV. "This will come as a dovish surprise to markets. A quiet day in Europe means EUR/USD’s focus will be on Powell, we look for 1.17 to hold.... Fed’s policy outlook currently does not take into account a possible trade war - and we don’t feel that this is a valid assumption. It may be remiss for Powell not to talk about the risks."

Also on Tuesday, the Chinese government repeated it would hit its 2018 growth target, one day after it reported slower growth in the second quarter and the weakest expansion in factory activity in June in two years. UBS economists lowered their estimates for Chinese gross domestic product to take into account trade war escalation, warning clients the country’s currency is likely to weaken.

Trading in government bonds was subdued ahead of Powell’s testimony, with the 10Y yield unchanged from Monday at 2.8582 percent. In the Eurozone, government bond yields inched lower by 0.5 to 2 bps, with investors unwilling to push yields any higher before Powell testifies. German Bunds yielded 0.36 percent, while 10Y Gilts paid 1.283 percent, both effectively unchanged.

Commodities climbed after Monday falling to the lowest in 11 months as WTI tumbled to $68 a barrel but has since stabilized.

Related: $1,000 Investment Bible Leaked For $10

Yesterday was actually a rare day where the Treasury curve steepened with 2s10s closing 1.4bps steeper at 26.0bps – a week since we last saw the curve steepen. Benchmark 10y yields rose 3.1bps to 2.859 percent making it 34 trading days in a row that yields remain entrenched in this 2.80-3.00 percent range. At the short end 2y yields ended 1.8bps higher while 30y yields were up 3.0bps by the closing bell. A weaker bond market in Europe was also about as exciting as it got with 10y Bunds +2.3bps higher to 0.359 percent.

A solid U.S. retail sales report combined with some positioning ahead of Powell’s testimony and a stream of bank issuance in the U.S. all appeared to play a role in one way or another in contributing to the bond moves. Equities appeared to be a lot less interested however. Last night the S&P 500 finished -0.10 percent despite banks rallying over 3 percent for the sector’s strongest day since late March. Bank of America surged +4.31 percent following a stronger than expected earnings report and as a reminder we’ve still got Goldman Sachs today and Morgan Stanley tomorrow to cap the large U.S. banks reporting for Q2. Coming back to the broader index, we couldn’t help but notice that the S&P 500 is now yielding less than 3-month T-bills which is an incredible statistic. It’s the first time that has happened since 2008. In fairness T-bills are also yielding more than 30y bonds in 12 European countries so the S&P is hardly on its own. Elsewhere, in Europe yesterday the Stoxx 600 also limped to a -0.25 percent fall with a -4.15 percent decline for WTI Oil on the back of potentially higher Saudi Arabia supply not helping sentiment across equities generally. EM currencies were fairly well behaved however while Gold (-0.27 percent) and the U.S. dollar index (-0.18 percent) edged a bit lower.

This morning in Asia, markets are broadly extending on losses with the Hang Seng (-1.11 percent), Shanghai Comp (-1.13 percent) and ASX (-0.50 percent) all down while the Nikkei (+0.95 percent) is bucking the trend as trading resumed post holidays. Futures on the S&P 500 and Nasdaq are broadly flat despite, after the closing bell in the U.S., Netflix’s share price dropping as much as -15 percent after reporting slower than expected growth in subscriber numbers in Q2 (+5.2m, c.1m less than consensus) and an outlook which suggested a decline in numbers for the current quarter. Elsewhere this morning Reuters noted the average new home prices in China’s 70 major cities rose the fastest in around 2 years, up 1 percent in the month of June versus 0.7 percent in May.

Coming back to the retail sales data yesterday, headline sales were confirmed as rising +0.5 percent mom in the U.S. in June as expected however this was on top of a five-tenths of a percent upward revision to the May print to +1.3 percent mom. Excluding autos and gas, sales printed at a slightly below consensus +0.3 percent mom (vs. +0.4 percent expected) however again there was a big upward revision to May to +1.3 percent mom (from +0.8 percent). The control group component (0.0 percent mom vs. +0.4 percent expected) was more of a wash with June’s miss offset also by May’s upward revision (+0.8 percent from +0.5 percent). Elsewhere the July Empire manufacturing reading came in at a slightly better than expected 22.6 (vs. 21.0 expected) albeit with the prices paid component falling a full 10pts while business inventories printed at +0.4 percent mom as expected. It’s worth noting that the Atlanta Fed revised up their Q2 GDP forecast post that retail sales data to 4.5 percent (from 3.9 percent) - the highest since last month.

Elsewhere there was plenty of focus on the press conference between President Trump and his Russian counterpart President Putin yesterday following their first summit together. Perhaps unsurprisingly the Mueller investigation into potential interference by Russia in the U.S. election was front and centre for those watching with Trump’s refusal to side with U.S. intelligence agencies and instead contradict his own security aides, subsequently criticised by Republican lawmakers including Senator John McCain and House Speaker Paul Ryan.

Meanwhile here in the UK it was another busy day for Brexit headlines. After accepting four earlier amendments and then enduring a night of tight votes as well as a resignation of a junior defence minister (Guto Bebb), PM May’s Brexit customs legislation has now passed its third reading with a vote of 318 to 285 in the lower House. Notably voting on two earlier amendments were fairly close calls with the government winning with 305 vs. 302 votes (14 Tories rebelling) and 303 vs. 300 votes (11 Tories rebelling) respectively. The Taxation bill will allow the government to levy duties on goods after leaving the EU. Looking ahead, the entire draft bill will go to the House of Lords for voting and approval before becoming law. For markets, Sterling traded as high as c0.5 percent up before paring back gains to close +0.10 percent stronger versus the Greenback.

Elsewhere, over at the Fed, Neel Kashkari reiterated his dovish view on rates as he noted “there is little reason to raise rates much further, invert the yield curve, put the brakes on the economy and risk that it does, in fact, trigger a recession”. In part as he pointed to “…if inflation expectations or real growth prospects pick up, the Fed can always raise rates then”. He also went on to say that “this time is different” (with respect to the yield curve) are the four most dangerous words in economics, in his view. Related: UK Stocks Bounce Back From Worst Selloff In Years

Before we look at today’s calendar, yesterday also saw the release of the IMF’s latest Global Economic Outlook. While the Fund made no change to either its 2018 or 2019 global growth forecast of 3.9 percent, the accompanying statement did highlight that “the expansion is becoming less even, and risks to the outlook are mounting”. They went as far as to say that “the rate of expansion appears to have peaked in some major economies and growth has become less synchronised”. Indeed the country-by-country forecasts highlight the widening divergence between the U.S. and other developed nations. The 2.9 percent and 2.7 percent growth forecast for the U.S. in 2018 and 2019 respectively was the same as the April forecast, however the Euro Area was revised down to 2.2 percent in 2018 and 1.9 percent in 2019, a downward revision of two-tenths and one-tenth. Japan and the UK were also revised down two-tenths this year to 1.0 percent and 1.4 percent respectively although forecasts for next year were left unchanged. There were also no surprises for China (6.6 percent in 2018 and 6.4 percent in 2019). Unsurprisingly the looming trade war concerns were cited as the greatest risk with the IMF saying that “the risk that current trade tensions escalate further – with adverse effects on confidence, asset prices, and investment – is the greatest near-term threat to global growth”.

Looking at the day ahead then, as noted at the top the main highlight is likely to be Fed Chair Powell delivering his semi-annual testimony to the Senate Panel in the afternoon. Datawise, May and June employment data in the UK will be a focus (4.2 percent unemployment rate expected), while June EU27 new car registrations and the final June CPI release in Italy are also due in Europe. In the U.S. we've got June industrial and manufacturing production prints along with the July NAHB housing market index release all scheduled. Q2 earnings for Goldman Sachs and Johnson & Johnson are also due. Meanwhile the BoE’s Carney, Bailey and Stheeman will speak on the Financial Stability Report while the Italian Finance Minister Tria will testify before Parliament.

By Zerohedge

More Top Reads From Safehaven.com: