Storm clouds appear more ominous by the day. Both home and abroad, financial markets are becoming increasingly unsettled and we would argue vulnerable. So far this week, the Dow has added almost 1%, although the S&P500 has declined 2%. The Utilities added almost 5%, increasing year-to-date gains to 28%. The economically sensitive issues are performing well, with the Morgan Stanley Cyclical index adding better than 2%, and the Transports more than 1%. The Morgan Stanley Consumer index is unchanged. The financial sector remains very strong with the S&P Bank index adding almost 3% and the AMEX Broker/Dealer index increasing 1%. The Broker/Dealer index now sports a 55% year-to-data gain. Elsewhere, with a downgrade and increasing worry of deteriorating fundamentals, Intel has been under heavy selling pressure, fueling a 6% decline in the NASDAQ100 and a 7% drop in the Semiconductor index. The Morgan Stanley High Tech index has lost almost 5%, decreasing its year-2000 gain to 16%. For the week, The Street.com Internet index is unchanged, while the NASDAQ Telecommunications index has declined 5%. A bit of air has come out of the speculative Biotech bubble, with the AMEX Biotech index dropping 11%, as its year-to-date gain drops to 80%. The small cap Russell 2000 and the S&P400 mid-cap indices have both declined about 1% so far this week. "Personal Loans" was one of the strongest S&P500 sectors today, gaining 4% on news that Citigroup is purchasing Associates First Capital. We are tempted to say, "they just don"t seem to learn." Only time will tell if Citigroup has better success than Conseco has had with GreenTree Acceptance, Bank One with FirstUSA, and First Union with The Money Store. It was a virtual buyers" panic for the subprime and consumer lending stocks today.

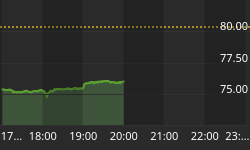

With inventories at the lowest levels in 24-years, energy prices continue their almost daily rise. Crude oil jumped $1.07 a barrel today to $34.90, a new 10-year high. Bloomberg quoted the CFO of oil and gas exploration company Apache: ""Relative to any point in the last 20 years I have never seen supply and demand as tight as it is today. You could see some significant prices surges" to $40 to $50 a barrel." Natural gas gained more than 2% on news of slack inventories, breaking above $5 for the first time ever. Natural gas began the year below $2.50. Platinum, after trading just above $400 during January, added almost $10 today to close at $610. Aluminum has gained $100 (7%) in just eight sessions, closing today at a six-month high.

In what should be an unmistakable sign of developing global financial instability, the euro today suffered its largest-ever decline against the dollar – dropping almost 2.5%. This dislocation, however, is not isolated to the euro. The Swiss franc declined to a an 11-year low, the UK pound a 7-year low, and the Australian dollar fell to near a 2-year low before recovering. For the session, 2% declines were suffered by the euro, Swiss franc, Hungarian forint, Swedish Krona, Greek drachma, Danish Krone, and the Czech Koruna.

U.S. and global credit markets continue to look vulnerable. Japanese bond prices sank for the fifth straight day as yields rose to the highest level in more than one year. Here at home, so far this week two-year U.S. Treasury yields have increased 2 basis points, the five-year 3 basis points and the 10-year and long-bond 4 basis points. Mortgages have slightly outperformed as yields have increased about 5 basis points. Spreads are largely unchanged, with agency spreads narrowing slightly. Corporate spreads for iA strong consensus has developed that subscribes to the view that the U.S. economy is in the midst of a meaningful slowdown orchestrated by Federal Reserve tightenings. We remain quite skeptical. For one, we are not convinced that the interest rate sensitive automobile and housing sectors are experiencing weakness despite the widespread perception. Keep in mind that last week"s report on new home sales came in much stronger than expected, with the inventory of new homes sinking to an 18-month low. Interestingly, the homebuilders have been the strongest S&P500 groups over the past five sessions, surging almost 14% while increasing quarter-to-date gains to 34%. And then today there was another increase in the Mortgage Bankers Association"s weekly application index. The key purchase application component jumped 3% to 307.4. For comparison, the purchasing application index was about 20% lower near 255 this time last year. Not easy to see weakness,

It is our view that home price inflation has actually been increasing. This view is supported by yesterday"s Conventional Mortgage Home Price Index, released by Freddie Mac. "Home-price appreciation rates increased from the pace shown in the first quarter of this year, and once again we are seeing gains in home values in every Census Division that are beating the overall inflation rate," said Amy Cutts, senior economist at Freddie Mac.

"Home values continue to rise, at an annualized rate of 6.9 percent nationwide in the second quarter of 2000, according to the Conventional Mortgage Home Price Index released today by Freddie Mac. The index showed that annual house-price appreciation also increased 6.9 percent from the first quarter of 1999 through the second quarter of 2000. Home values in the New England states grew at an astounding annualized rate of 11.1 percent, improving upon the strong growth of 10.2 percent shown last quarter (36.2% for 5 years). The West North Central states came next, posting a robust 8.7 percent annualized growth rate (33.1% for 5-years), followed by the West South Central states, which showed a strong annualized gain of 8.5 percent (25.2% for 5 years).

Homeowners in the Pacific states saw home values increase by an annualized 8.1 percent during the period (30% for 5 years), matching the increase enjoyed by homeowners in the Mountain states who also saw annualized gains of 8.1 percent (29.3% for 5 years). The prices of homes in the East South Central states grew at a slower rate than the national average at 6.5 percent (26.9% for 5 years) while the Middle Atlantic states grew at a slightly slower annualized rate of 6.1 percent (24.2% for 5 years). The South Atlantic posted an appreciation rate of 5.8 percent (26.7% for 5 years) and the East North Central states finished last with an appreciation rate of 5.2 percent annualized rate (31.6% for 5 years) of growth in home prices."

And with such strong housing wealth effects, we are not surprised with continued robust consumer spending. We see that the Tokyo-Mitsubishi weekly index has retail sales increasing at a rate of about 1.2% from last month, with same-store sales 4% above very strong sales this time last year. The Redbook survey of same-store sales corroborates strengthening retail sales.

We follow monthly auto sales very closely as this data provides quite timely information on a key area of consumer demand. After digging through the August car sales reports, it is obvious that the consumer spending spree is anything but over. Quotes from two Japanese manufactures certainly support the view of continued strong auto sales.

"We've seen no evidence of a slow-down in what is, obviously, a very competitive buyer's market. Consumers remain confident and motivated. They know what they want and they are shopping the best deal." Jim Press, Toyota executive vice president.

"When you're hot you're hot, and in August we were sizzling. The big percentage increases were in light trucks, and we also sold more than 42,000 Accords (a new August record), 34,000 Civics and nearly 13,000 Acuras." Dick Colliver, American Honda executive vice president.

In fact, despite all the talk of the big slowdown in consumer spending August new car sales came in at a brisk annualized pace of 17.5 million units. This was an acceleration from July"s 17.2 million unit rate, and slightly ahead of an exceptionally strong August of 1999. U.S. car buyers" infatuation with imported vehicles continues as U.S. manufacturers saw their market share drop 63.7% (from 65.9% last year). Meanwhile, the Japanese share jumped to 30.1% from last year"s 28.3%. Certainly not the makings of a slowdown, Honda reported its BEST month of U.S. sales in it history, beating the previous record set last August by better than 5%. Year-to-date, Honda sales are running 15% above last year. Toyota had its BEST August ever, with sales 6% ahead of year ago levels. Lexus posted its BEST month ever, with sales surging 20% above a year ago. Nissan sales increased almost 3%, with its luxury Infinity line seeing year-over-year sales jump 12%.

BMW had its BEST month of U.S. sales ever, posting a 22% increase from last year. Mercedes-Benz posted its BEST August and third-best month ever, with sales running 25% above last August. Volkswagen had its BEST month in 26 years, with sales 6% above last year. At Volvo, "our business was very solid across all car lines. Compared to last August, we are up 20% and for the year by 15%." Jaguar sales jumped 47% from last August. August sales were up 11% at Audi, with year-to-date sales surging 32%.

For the U.S. nameplates, Ford set a new August RECORD. New August RECORDS were established for the Explorer and Lincoln lines. Chrysler had its "STRONGEST August in the corporation"s history," with its BEST ever month for both sports-utility vehicle sales and minivans. Total truck sales jumped 16% from last year, with Jeep Cherokee sales increasing 12% and a record month of Dodge Truck sales, also increasing 12% from last year. And while GM posted 5% declines for both auto and truck sales, these are verses very strong comparisons from a year ago. Last month was in fact the second-best August for GM trucks, and the BEST August for Chevrolet and Pontiac Trucks.

Mitsubishi had its BEST August on record, with sales increasing 6%. Kia had its BEST ever month in the U.S., with sales increasing 25%. Sales at Hyundai were 32% above last year, with year-to-date sales already surpassing 1999"s total. Suzuki sales surged 24%, for it BEST August in 12 years.

And in regard to the perception of a slackening in the labor market : "Employers" need for additional workers is far from satisfied according to the Employment Outlook Survey conducted quarterly by Manpower Inc., global leader of workforce management services and solutions…Of nearly 16,000 firms interviewed, 32% plan employment increases, 7% expect decreases, 57% anticipate no change and 4% are uncertain. The results herald the strongest year-end demand in the 25-year history of the poll."

Also arguing against the economic slowdown analysis, today the National Association of Purchasing Managers Non-Factory index jumped 4 and one-half points to 60, indicative of strong growth. "In August, NAPM's Non-Manufacturing Business Activity Index continued its long-term growth trend and indicated a faster rate of growth than in July," Kauffman said. "New Orders, Backlog of Orders, Export Orders, and Employment all increased at faster rates in August than in July, while Imports and Inventories increased at the same rate as in July, and Prices increased at a slower rate than in July. Supplier Deliveries were slightly slower in August than in July, with an increased rate of slowing. The Non-Manufacturing Inventory Sentiment Index indicated that purchasing executives felt a lesser degree of discomfort with the level of inventories in August than they did in July…Increased business activity in August was reported by 32 percent of purchasers, an increase of 6 percentage points from the 26 percent reporting more activity in July."

And complementary to our view that excessive demand continues to fuel this dangerous boom is our expectation of increased inflationary pressures. We certainly sense heightened inflation concerns globally. These are a few of the headlines from international business stories we have come across over the past two days: "Inflation in Indonesia may exceed target; euro under pressure as inflation worries grow; Malaysia wary oil subsidy cuts may spur inflation; (Philippine) August inflation inches up; Australian confidence up, but inflation looms; Fear Oil Could Ignite (Canadian) Inflation; U.K. Bonds Fall - Weakening Currency Heightens Inflation Concern

Times they are a changin"….