Weekly Trader Alert #92

2/20/2007 9:28:04 AM

Overview

This past week was highlighted my mostly benign economic reports, some merger news, and a lot of focus on Fed Chairman Ben Bernanke's two day meeting with members of Congress. Bernanke seems to have the magic touch, not ruffling feathers of Congress people, and being able to say things that don't spook investors. Somehow, he was able to thread the needle on suggesting that inflation is still a risk, but lessening and it doesn't mean that the Fed will raise rates.

This seems to have caused the bullish camp to once again believe that the Fed may lower rates, to compensate for the continued fall of the housing market. No one at the Fed communicated this, but it seems to be the popular theme espoused late in the week.

Let's take a look at the week in review:

Monday: There were no economic reports released.

Tuesday:

Tuesday's sole economic report reflected the trade balance. The trade deficit grew to $-61.2B in December from November's $-58.1B. The deficit peaked in August of 2006. Exports have been at record levels for five months in a row, but imports increased in December, due to higher oil prices, autos, and consumer goods. China's deficit represents 31% of the total.

There was a rumor that Dow component, Alcoa (NYSE:AA) is the target of two different $40B buyout bids from BHP Billington (NYSE:BHP) and Rio Tinto (NYSE:RTP) respectively. This helped the market to open higher and spurred further buying interest on merger prospects.

Wednesday:

Fed Chairman Ben Bernanke addressed Congress Wednesday. His comments were essentially that the economy continues to grow at a moderate pace and that inflation pressures are easing, due in large part to moderating oil prices. This was enough to send interest rates down in the bond market and sent equities soaring. Microsoft (NASDAQ:MSFT) and Intel Corp (NASDAQ:INTC) both rallied strongly and since they are the only stocks listed on all three major indexes, there was a correlation as all three major exchanges advanced.

Thursday:

There were a large number of economic reports released, including the following:

- Export prices rose 0.3% while import prices were flat

- Initial jobless claims jumped to 357K versus an expected 315K

- NY Empire State Index rose to 24.4 versus an expected 11.0

- Net Foreign Purchases increased by $15.6B versus and expected $60B

- Industrial Production fell by 0.5% versus an expected 0.0%

- Capacity Utilization fell to 81.2% versus an expected 81.7%

- The Philly Fed Index came in at 0.6 versus an expected 4.0

Friday:

PPI fell 0.6% (consensus -0.6%) in January, due to a drop in energy prices. Core PPI rate (excludes food and energy) rose 0.2%. This is as expected dropping the year over year rate to 1.8%. This supports the Fed's outlook that inflation pressures are easing. There was more bearish news from housing, as housing starts fell 14.3% to 1.41 mln (consensus 1.60 mln). This is the lowest rate in ten years. Building permits fell 2.8% to 1.57 mln (consensus 1.59 mln). Finally, Michigan Consumer Sentiment was reported at 93.3 versus an expected 96.5.

Oil fell fifty cents from its close a week ago, ending the week at $59.39. Natural gas fell more than thirty-two cents to close at $7.503. Both energy products continue to find support above their uptrend lines.

Last week we stated we believe the Fed is prepared to raise rates yet again if the markets don't react to their jawboning on inflation concerns. The market has, in fact, chosen to react to the hawkish tones of the Fed by worrying that they may raise rates soon. With Bernanke himself convincing investors that the Fed won't be too hasty to raise rates, equities have moved up.

If equities continue to rise unabated, we would expect that the Fed will actually raise rates just to get everyone's attention. However, we could be seeing a pause in that rise, or perhaps even some sort of the oft discussed pull-back. It is unlikely that the markets will make a strong move up next week, as, except for Tuesday, there is little in the way of earnings reports that could influence the market much. It is probably a bit more likely that stocks could drift sideways or downward.

To understand more about our view on the markets, we will have to look at the charts.

Market Climate

The market began the week moving up but lost all those gains on Friday as worries of Fed rate hikes took their toll.

The market underwent further accumulation last week until Friday when there were signs of widespread distribution. One day doesn't make a trend but it is worthwhile to monitor accumulation or distribution for a divergent move to the market as it is an early warning sign that things are out of sync. At this time, there is a correlation to the price movement of the stock market and the signs of accumulation and distribution.

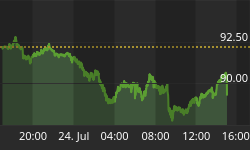

The U.S. stock market composite chart:

It is like deja vu all over again. A week ago, we saw a move lower on Friday. We saw similar weakness the next trading day (Monday this week), and then prices began to move up.

Last Friday, we saw the markets open weaker, but gamely tried to regain lost ground throughout the trading day. Volumes are trending down, while price is trending up. MACD has not yet seen a bearish cross (but it looks like it is setting up for this). RSI is weakening.

Overall, we have little confidence that the uptrend will continue in the short term, and we think it is more likely that we will see a consolidation or a downward move begin this week.

Fundamental Trends

The mining industry is now represented in the leaders by the machinery makers, which are in fourth place. Chemical Fertilizer makers are in second place, with two Food industries in the #1 and #3 spots. Core inflation isn't affected by rising food prices, which have definitely been affecting inflation generally. This is a trend we identified early on.

The steel trade isn't visible in the leaders, but both industries are in the top screen, with Alloys in 7th place.

Three Auto and Truck industries remain in the top screen, with tires and replacement parts in 10th and 11th place and the auto and truck manufacturers moving into 27th place.

There are still three building industries in the top screen.

The US Integrated Oil industry remains in the top screen but falls to 26th place.

The Industry leaders (ranked 1st-5th out of 190) are:

Leaders 2-16-2007 | Leaders 2-09-2007 | Leaders 2-02-2007 |

Food (Dairy Products) | Auto & Truck (Repl Parts) | Machinery (Automation) |

Chemical (Fertilizers) | Container (Metal/Glass) | Container (Metal/Glass) |

Food (Meat) | Food (Meat) | Steel (Alloy) |

Machinery (Const/Mining) | Retail (Department Stores) | Food (Meat) |

Container (Metal/Glass) | Machinery (Automation) | Building (Residential/Com'l) |

There are now three Petroleum industries in the cellar dwellers.

Mortgage services were hit hard a week ago, but have rebounded enough to have left the cellar dwellers. The others continue in the laggards, with the additional petroleum industry being the drillers. Drillers will actually continue to make money even if the price of oil turns down. This, however, may remove some of the pricing power they have enjoyed of late.

The Industry laggards (ranked 186th-190th out of 190) are:

Laggards 2-16-2007 | Laggards 2-09-2007 | Laggards 2-02-2007 |

Petroleum (Cdn Expl/Prod) | Petroleum (Intl Specialty) | Software (Educ/Entr) |

Petroleum (Drilling) | Financial (Mortgage Svcs) | Electronic (Misc Prod) |

Chemical (Plastics) | Instruments (Control) | Energy (Coal/Other) |

Petroleum (Intl Specialty) | Petroleum (Cdn Expl/Prod) | Petroleum (Cdn Expl/Prod) |

Instruments (Control) | Chemical (Plastics) | Chemical (Plastics) |

Trade Recommendations

We continue to monitor BPT for an entry. It is now getting down to where value investors will become interested in the high dividend payments they will continue to make. We haven't yet had confirmation that the downtrend is completed so we have been cautious about issuing a recommendation for entry. We will monitor the trade and send out an intraday alert as necessary.

We missed our entry on Rogers Corp. but will watch for a light volume pull back this week, if the market shows some weakness.

We are monitoring another long trade for entry. The stock is Dr. Reddy's Lab LTD. (NYSE:RDY). It is an Indian software house and appears to be significantly undervalued at this time, as well as having just completed a bit of a sell off.

Current Portfolio

FDG closed the week at $23.00. As expected, it tested down to but never closed below its 100-day moving average. As stated last week, if the stock holds the $23.00 level, through the consolidation, then it should rebound strongly higher. We did see a close as low as $22.85, but this never broke support, so FDG could be getting ready for another run higher. Stay tuned.

Note: FDG said C$1.00 is available for dividend payment for the most recent quarter. That will likely be paid in late March. We are long FDG.

We covered our short position on CLF for a 2.5% profit.

* Initial stop prices are set to cause us to exit our positions if they close below these levels. You will note they are generally kept pretty tightly the opposite side of the trades we initiate. Historic volatility would imply that intraday price action may trade outside of these values, so that condition is insufficient to cause an exit from an existing position. On significant movement beyond our stop prices, we may issue an intraday message to exit the position or to maintain the position. You may chose to implement an absolute stop below these suggested stop values, but that stop should be wide enough to take care of the daily volatility for the stock in question. You can examine the candlesticks for an idea of intraday price fluctuations.

Entry prices are adjusted to account for dividends paid. The stock price was adjusted by your broker, to reflect the dividend taken out. The non-adjusted entry price reflects the actual entry price, without the adjustment for dividend values.

LVPB Concept: The concept is a Light Volume Pull Back, where a stock's price will pull back to a support level on light volume. Obviously, heavy selling is a sign of weakness, and we would not want to buy on a heavy volume pullback. However, we will occasionally place stocks on the LVPB (Light Volume Pullback List) to indicate a "re-entry" buying opportunity, when we have already entered a position. This should be used to add to existing positions, or to enter a position if you missed the initial entry.

LVPB Portfolio Stocks:

Conclusions

Q3 growth was unexpectedly strong. Q4 growth appears to be coming in around 11% for the S&P-500. Q1 is only expected to show about 5% growth, so this is quite a haircut off of the Q3 and even the Q4 numbers. That slow down in growth may lead investors to take some profits in order to reduce risk. Growth is still growth, and the economy continues to grow, and inflation appears to be continuing to be reduced.

Bonds don't look particularly attractive, with their value moving inverse to interest rates. Since the Fed has made it pretty clear they do not intend to cut rates any time soon, and they have reinforced that they are more likely to raise rates, this means the value of bonds is more likely to move down in the short term.

The biggest concern for the economy is housing and the weak domestic automobile industry. If the housing slump were to spill over further into the economy, this may cause the Fed to act to reduce interest rates. In fact, this is the crux of a new bullish argument why stocks will continue to rise. You have to hand it to the bulls, as they find a slowing economy as the reason to be bullish on stocks and other investors seem to continue to believe in that scenario.

This economic growth and the run-up in stock prices has a lot of parallels to the late nineties. Of course, there is the noted difference that stock prices were trading at much higher multiples, especially the dot come flyers. We actually believe that many of the Dow stocks are trading at significant discounts to their fair value at this time, so this uptrend could actually continue for a very long time. If this run wasn't already a bit long in the tooth, we would probably see more bulls beating the drum. This may be the wall of worry that allows the market to continue climbing into next year.

For those of you who have enjoyed your subscriptions to the Fundamental Trader and who would like to get additional savings off the price of your subscription, you may consider an annual subscription to the service. You can save nearly 20% off of the monthly rate by selecting the annual subscription price. Just click on the link below:

http://www.stockbarometer.com/pagesMFT/learnmore.aspx.

Regards and Good Trading,