The home price declines in Silicon Valley are anything but hidden for most people trying to sell their homes, but it doesn't seem to show up in monthly and weekly reports that show slight YoY gains in the median prices. I have used Santa Clara County as a proxy for Silicon Valley and it is also a good proxy for the SF Bay Area except that Santa Clara County has held up better than most other parts of the Bay Area.

There are two sources of data that I have used - DataQuick, which reports on all home sales, SFHs (single family homes) and condos, new and resales, and sales on MLS, reported by California Association of Realtors (CAR), which reports SFHs and condos separately and most of the detail break down are for SFHs. San Jose Mercury News, the main paper in the area, publishes weekly data from DataQuick with break down by zip codes and that is my source for the DataQuick reports.

My objective is to present an explanative model and factual data that unambiguously show why the price declines are not showing up in the reported data. Let us start with a simplified model of what is happening in the real world shown in Table 1.

| Table 1: | Hypothetical Volume & Price Mix of SFHs Sold In Santa Clara County | ||

| A Year Ago | Present | ||

| Volume | Price | Volume | Price |

| $2M & Above | 1.8M & Above | ||

| 200 | 1$.5M | 225 | $1.35M |

| 200 | $1M | 250 | $900K |

| 300 | $800K | 200 | $720K |

| 200 | $600K | 150 | $540K |

| 100 | $500K & Lower | 75 | $450K & Lower |

| Total | Median | Total | Median |

| 1000 | $800K | 900 | $900K |

What you will see from Table 1 is that despite drops in volume and price there can be a gain in the median price if the mix of home sales changes significantly from a year ago in favor of the high-priced areas. This very much seems to be the case based on reports to-date as well as a report from the field on the current activity (sales initiated in March and April that will show up in reports for April and May).

Let us start with fundamentals of supply and demand to see where the pressure for the price declines is coming from. From the most recent reports the demand for SHF resales for the county is down 20%, YoY. Fig. 1 shows that the supply is up 40%, YoY, and the YoY percentage increase has gone up from 20% to 40% over the past two months and this trend is likely to continue.

The combination of 40% increase in supply and 20% decline in sales, YoY, means that over the past 12 months the supply-demand has deteriorated by 75% (1.4/0.8 = 1.75), i.e., the supply is up 75% relative to the demand. Now, let us see what is happening to the prices.

Fig. 2 above shows the median listing price of SFHs listed on MLS (the listings that are pending sale are excluded). The 13.5% decline does over-estimate the actual decline in prices, or price pressure, because currently the median price of sales is 5-10% higher than the median listing price while a year ago it was 5-10% lower. This is strictly due to significantly higher level of sales in the high-priced areas and much lower level of sales in lower-priced areas. This will result in fewer active listings in the higher-priced areas and mounting listings in the lower-priced areas, thus depressing the median listing price.

Now, I need to provide evidence that indeed there are higher levels of sales in high-priced areas and lower levels of sales in lower-priced areas compared to a year ago. Table 2 below is sorted by median price for zip codes and show YoY volume change, both averaged over the last 6 DataQuick/SJM weekly reports (each report gives sales for the preceding four weeks). The vast majority of these sales were initiated in January and February.

| Table 2: | Price Versus YoY Change In Sales Volume Averaged Over the Last 6 Weekly Reports For Various Zip Codes, Santa Clara Co. Data Source: DataQuick/ San Jose Mercury News | ||

| Median Price | YoY Volume | ||

| $1,770,417 | -9.7% | ||

| $1,641,375 | -10.6% | ||

| $1,622,417 | 39.2% | ||

| $1,556,250 | 20.2% | ||

| $1,319,000 | 11.2% | ||

| $1,147,875 | 34.7% | ||

| $1,059,515 | -15.3% | ||

| $1,006,333 | -14.4% | ||

| $981,125 | 35.5% | ||

| $896,667 | 118.8% | ||

| $896,167 | 20.3% | ||

| $871,958 | -9.2% | ||

| $823,750 | 53.9% | ||

| $815,083 | 31.3% | ||

| … | … | ||

| $655,750 | -27.1% | ||

| $647,917 | -48.6% | ||

| $644,125 | -40.2% | ||

| $642,458 | -28.4% | ||

| $638,167 | -25.9% | ||

| $634,250 | -10.9% | ||

| $627,417 | 20.3% | ||

| $619,417 | -43.0% | ||

| $617,167 | -20.3% | ||

| $614,000 | -17.5% | ||

| $605,833 | -27.8% | ||

| $599,583 | -19.3% | ||

| $592,833 | 21.0% | ||

| $588,500 | -21.1% | ||

| $582,167 | 10.5% | ||

| $565,208 | -31.0% | ||

| $558,417 | -33.9% | ||

| $546,208 | -30.5% | ||

| $536,417 | -24.3% | ||

| $426,125 | -39.2% | ||

| Median of Top 14 | 20.3% | ||

| Median of Bottom 20 | -26.5% | ||

Even though there is lot of noise in the data in Table 2 due to relatively small number of sales for a zip code for a 4-week period the signal is loud and clear and not suppressed by the noise (estimation and detection were my areas of specialty during my Ph.D. work). The trend of sales that were initiated in January and February, favoring sales in high-priced areas, has only accelerated based on recent reports. Here are comments by Richard Calhoun, REALTOR, Creekside Realty: "The high level of sales also includes Mt View, Sunnyvale, Cupertino, Santa Clara, Campbell, Cambrian and Almaden Valley [high-priced areas]. But this is contrast to other areas such as East Valley, South County, Evergreen, South San Jose, Central San Jose, Santa Teresa and Blossom Valley." According to Mr. Calhoun, Los Altos (excluding Los Altos Hills) and Palo Alto have seen very high levels of activity in recent weeks and a low level of supply. What I have noticed in the past week is that in these two townships there are 2.5 new listings and 0.25 price reductions for every sale (assuming that all the active listings that disappear are sales). Therefore, the low supply was purely a seasonal factor and the supply will catch up with the demand as the season picks up steam. The pressure on prices will be great during July-August as listings mount at much higher rate than the sales.

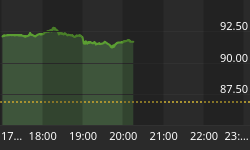

What is happening to prices in the high-priced areas? There is a bull (SVB) who lives in Los Altos zip code of 94022 and constantly posts bullish housing news in his area and taunts me for my bearish views despite lot of evidence that the bubble has burst and data show price declines in his zip code. Fig. 3 shows price data for 94022 as reported by DataQuick/SJM (I don't have data for the missing period).

I wouldn't be surprised if the YoY median price gains in SFH resales for Santa Clara County during Mar-Jun show 10-15% increases. That is how much the shift has taken place in sales in the high-priced areas compared to the low-priced areas of Silicon Valley this year. What explains it? The ""silly" money." Silicon Valley, like Manhattan, is a poster for America becoming a nation of Haves and Have-nots. People in Silicon Valley have forgotten the short depression of 2001-02 (more than 20% decline in total employment qualifies for a depression by anyone's definition) and home price declines that took place. What saved Silicon Valley from the continued depression, or deep recession, was that the housing bubble in the rest of California and many parts of the nation arrived there in late 2003 early 2004 led by "toxic mortgages." It so happens that the "toxic mortgages" affected the lower-priced areas much more than the higher-priced areas.

There are at least 10% of those who were employed in 2000 and have dropped out of the labor force due to lack of "suitable" jobs since who still live in Santa Clara County. Therefore, the unemployment rate that is reported grossly underreports the actual unemployment rate. How have these unemployed managed to live there? Home equity withdrawal. If there were to be a 20%+ decline in home prices these people will be forced to sell their homes and move to cheaper areas. This will further exacerbate the price decline. The people who claim that home prices in Silicon Valley CANNOT decline by more than 20% are the same people that said that the leading local tech stocks in 2000 couldn't decline by more than 50%. My prediction of 93.9% decline in CSCO fell short by 3.8% (the actual decline was only 90.1%).

Is what is being observed in Santa Clara County, in terms of bias of sales towards high-priced zip codes, applicable to other areas and at a broader scale? My best guess is yes, especially, in L.A. County and Southern California as a whole. Needless to say that it applies to New York City area because the dynamics are the same. There is another form of bias that shows bigger price gains (or hides the price declines) than the true price changes taking place in any area. For example, widely followed OFHEO HPI is very heavily distorted because it looks at price changes in the homes that are sold more than once by comparing with the prices during the previous sales of the same properties. The problem is that home that are sold are far more "modernized" than the homes that are not sold! This is particularly true during price bubbles. I read stories of homes in Palo Alto that are practically ripped apart for the purpose of selling (spending $0.8-1.0M for listing price of $2.5M). What do you suppose are changes in homes that have been sold 3 times in 30 years versus the home never sold during the same 30 years?

The problem with any data series, like with many real world issues, is: The Devil IS in the Details. According to a historian, general history is useless and correct lesions can only be learned from detailed history. In a fast food society busy accumulating "the crap that we don't need" who has the time?