The explosion in commodity prices over the last few years has been nothing short of spectacular. After a generation long bear market, all commodities - from base and precious metals to energy -- have soared to multi-year highs while many broad equity market indices are only this year reclaiming highs set in 2000.

The explosion in commodity prices over the last few years has been nothing short of spectacular. After a generation long bear market, all commodities - from base and precious metals to energy -- have soared to multi-year highs while many broad equity market indices are only this year reclaiming highs set in 2000.

Traditionally, commodity markets have been the domain of specialized, higher networth or larger commercial players with the capital and expertise to navigate them. Issues of accessibility, high storage and insurance costs, or simply higher volatility have been long running deterrents for individual investors. But the introduction of exchange-traded funds tracking various commodities has leveled the playing field and facilitated more convenient investment opportunities for retail investors, while also blurring the lines between core and alternative investment classes.

Producers Oppose Commodity-Backed ETFs. Many analysts, and commodity users in particular argue, that each new commodity ETF puts upward pressure on the underlying reference commodity, thereby competing with industrial demand. Is this correct? For purposes of this discussion we will examine only the more applicable grantor trust structure - these are ETFs that are linked to spot commodities, backed by physical holdings. Other commodity ETFs are available that provide futures-based or senior debt exposure. They will be the subjects of discussion in future editions of ETFocus.

The Silver Users Association opposed the creation of a silver ETF lobbying hard with the US Securities and Exchange Commission to oppose the launch. Similarly, the world's largest platinum producers, AngloPlat and Impala Platinum, voiced strong opposition to a proposed platinum ETF (which has since launched in Switzerland and the UK). Financial Times headlines prior to specific commodity ETF launches confirmed their concerns: "ETF talk continues to fuel platinum rise", "Expectations on ETF ruling push silver to 22-year high", or "Platinum up on ETF speculation."

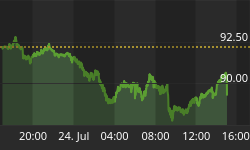

Certainly news of pending ETF launches has attracted speculative capital and sparked short term rallies in the underlying commodity price. Prior to the launch of the silver ETF (AMEX:SLV) prices for the commodity reached 26-year highs. Shortly after the launch however, silver prices proceeded to collapse by over 30%, still not having recovered those highs (see figure 1).

Whether upward adjustments in silver prices prior to the listing were coincidental or driven by speculation, price movements are always explained by more than one variable. And, over the short run, any market can become separated from the underlying fundamentals and temporarily influenced by news or investor sentiment. However, in the longer run, fundamental factors (supply/demand, valuations, etc.) act like anchors, limiting larger divergences from equilibrium price levels. In perhaps his most famous words, Benjamin Graham said "In the short run, the market is a voting machine but in the long run it is a weighing machine." The same holds true for all asset markets, regardless of ETF availability.

If You Build It, Will They Come? Like all business ventures, ETF innovators take risks when launching new products. There is no guarantee the vehicle will attract sufficient demand. Commodity ETFs certainly make accessibility easier, while improving liquidity and market efficiency, and may fill a core asset class for strategic portfolios. But merely providing a more efficient vehicle does not necessarily initiate investment demand.

Consider the arrival of precious metal ETFs. Australia was first to market, listing the first ETF backed by gold bullion in 2003 (AU:GOLD). To date the vehicle has had limited success, accumulating only 12.48 tons of gold as of July 2007. The experience in the US was entirely different. Their first gold ETF (NYSE:GLD - perhaps the most controversial and successful ETF in history) listed at the end of 2004 attracted over USD 500 million in it's first day of trading and currently holds over 500 tons of gold -- a market value of almost USD 11 billion.

To put this number into perspective, world official gold holdings total more than 30,000 tons. So although still representing quite a small amount, the data shows the increasingly important role ETFs are playing. From 2004 to 2006, investment demand increased from 13.5% to over 19% of world demand. Of this investment demand, incremental demand from ETFs increased from 3.8% to 7.7%. Annual global investment demand - which has had a five-year average of 477 tons -- has increased from 470 tons in 2004 to 643 tons in 2006.

It's a longer running adage that investments are sold. And they sell best at price peaks. Recently, the trend in ETF accumulation has reversed along with declining gold prices. In fact, world gold ETFs saw net outflows during Q2 2007, even while investment demand was strong in other retail products (bullion bars, official coins, medals, etc.). Whether a continuing development or not, it calls into question the concept of a successive "feedback loop" of ETF vehicles creating their own ever-increasing demand.

There are many triggers that can reverse these inflows. And, crucially, can the inflows not equally be reversed when the tide turns? Substitution also plays a role. When ETF flows are increasing, investors may be diverting holdings from physical holdings to the more easily managed ETFs, diminishing other forms of investment demand.

Commodity ETFs may even decrease systemic volatility, as they are likely to have a more solid investor base than investors in the volatile and speculative futures markets as an example. Investment in both gold and silver ETFs has remained stable in the last year, even as gold and silver have both witnessed significant price corrections.

Small-Cap ETF Phenomenon Questionable. Commodity ETFs are not the only ETFs thought to have created their own demand. Some analysts have attributed small capitalization stock outperfomance (versus larger capitalization equities) over the last seven years to the growing availability of small-cap ETFs, creating "price-insensitive" buying in this area. To an extent, this may be true. A large influx of capital into a particular asset class and the resulting increase in prices can encourage its own demand temporarily. Unfortunately, performance chasing leading to higher prices (and the inevitable decline) is a hallmark of investor psychology. But this holds true for many investment vehicles, including mutual funds and other pooled instruments that must purchase the underlying asset.

Reviewing the figures, US small-cap equity ETF assets hold only approximately USD 30 billion in assets - not even 2% of the total US small-cap market capitalization. Other factors must have transpired that had a larger impact on small-cap performance. Most notably, the private equity boom of the last few years has bid up share prices of small-cap firms seen as possible takeover candidates. Of course, this could not have happened without easy access to cheap credit -- conditions unrelated to small-cap ETF availability.

Similarly, leveraged investors have relied on abundant cheap capital and may be responsible for much of the rise in commodity prices (the hedge fund community now approaches USD 2.6 trillion as of second quarter 2007 according to statistics supplied by www.hedgefund.net). Many analysts point out that speculators, more interested in momentum than underlying economics, now account for a significant price premium in most listed commodities. Recent disruptions in liquidity, however, show how quickly these premiums can be removed.

Commodities as an Investable Asset Class? The commodity bull market also highlights a wider issue -- the role direct commodities should play in investor portfolios. Traditionally, commodities have been labeled "flow" items versus an "investment" item on the balance sheet. Much has changed in this decade. Once a peripheral investment class at best, they have moved to centre stage, showcased as a "core" holding for investors.

With the backdrop of sagging equity markets earlier this decade, investors were seeking alternative-type asset classes with low or negative correlation features. Commodities fit that mandate. Spurred on by the initial run up in commodity prices (and by consultants armed with a plethora of academic papers citing the benefits of commodities as a core asset class), even large institutions have jumped in with both feet.

In an industry known for its cyclicality, investors are advised to exercise caution. Knowledge of these markets is essential as corrections can be abrupt and additional factors such as weather, growing patterns and seasonal tendencies are present. With slowing US economic growth and rumblings in global credit markets, many commodity markets -- particularly industrial metals -- are vulnerable to sharp downside movements.

Conclusion. ETFs have introduced market instruments that meet longer-term asset allocation needs for investors. From fixed income transparency to low-cost equity exposure, direct commodity ETFs bring similar benefits - lower cost, liquidity and ease of use. But as is true for all investments, including ETFs, an in-depth knowledge of the underlying fundamentals is paramount before jumping in.