The article below was sent to members on Sunday, September 16, 2007. The updated chart on the right is showing that the Euro has already recognized a long awaited target discussed in the update below.

The article below was sent to members on Sunday, September 16, 2007. The updated chart on the right is showing that the Euro has already recognized a long awaited target discussed in the update below.

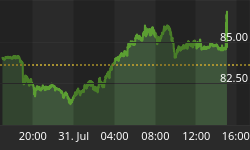

When EUR reversed from the July 138.50 high I kidded Dom that his long standing target of 1.40 was eerily close but maybe the market wouldn't let him get the official print. Well it didn't take long and after a 30 day sell-off that corresponded with a global risk premium correction in credit, equities and carry trades, we are now back staring square at the 1.40 level, trading fractions away Wednesday at a high of 1.3927. That number must be a magnet and if it turns EUR back in a major change in trend, there could be a massive asset allocation shift occurring.

The timing of this move back to the highs is intriguing and maybe even raises the level of its importance considering next week's convergence of US broker/dealer earnings reports, a FOMC meeting on Tuesday and maybe the most important event, the rolling over of approximately $140b in European commercial paper, much of it collateralized by mortgages. According to this Bloomberg article, Bank of America London estimates that 59% of the $230b asset backed paper in Europe comes due this month and that the peak will be Monday 9/17 when the equivalent of $48b matures. Friday we saw a glimpse of the seriousness in this CP roll as British mortgage lender, Northern Rock, could not refi their paper and had to tap the BOE for emergency funds which in turn drove a run on the bank's deposits (reportedly an astounding $2b withdrawn) similar to what transpired at US thrift Countrywide just a few weeks before. NRK stock lost 30% in Friday's trade and is down 65% from the highs in June. The run on deposits adds insult to injury as lenders are forced to replace even more capital in money that was borrowed in CP market and from customer's deposits. If they can't access enough money from central banks or the penalty rate is too high, they may be forced to sell assets at a discount, further eroding book value. Trouble in the European banking system not only poses problems for individual bank's share holders but also a more systemic crisis of confidence in the solvency of the market economy which could ripple across the globe.

When we discussed the price of crude a few weeks ago, we thought that much of the petrodollars were being recycled through European banks which can explain some of the out-performance of euros and sterling v the dollar and yen so naturally we found it ironic that EUR would be pushing the 1.40 level while crude made a new high above $80 this past week. The run on the bank at NRK is very ominous and could spiral into a much larger problem if this 1.40 level is real. The sheiks would be getting nervous if they think their deposits are at risk and we could see a run on banks unlike the global capital markets have ever had to endure. The NY Fed study we cited in our crude article reported, oil export revenues jumped from $535b in 2002 to $1.5t in 2006, a number greater than 10% of US GDP. The same report notes that roughly $480b has gone into the purchase of financial assets. Like Mortimer Duke stressed, "this is not Monopoly money we're playing with" as these vast sums have been one of the main drivers of asset prices for the past five years. It's difficult to handicap where the petrodollars would flow, but the unwinding could be very disruptive to European bourses and credit markets. We will be closely watching the reaction around Dom's multi-year target and if we get a reversal would become very defensive on risk premiums.

As with any important price target left by "the Dead Italian", Dom expects the market to recognize the level by vibrating around, potentially between 1.3969-1.4139, before reversing. A blowoff can see prices rally as high as 1.4600 If we are seeing a major top in EUR there must be something important unfolding in the markets. Failing to print 1.40 on the previous high and knowing how important it was to Dom, kept many of us from becoming too bullish on the greenback as we thought a Fed ease would drive one more flush. We were hoping to simultaneously get our capitulation low in the dollar while finally seeing a 1.40 top print on EUR. That appears to be what is happening with the Fed on deck this week, but just as we thought a major dollar low would result from the de-leveraging of credit, we now must consider the larger ramifications of a major high in EUR and the asset allocation shift that could accompany such a reversal of this long-term trend.

Bottom Line: We may be setting up for a major EUR trend reversal with far reaching implications. We advise all investors to keep an eye on the price action in euros and sterling and their respective LIBOR rates for indications of banking system dislocation.