Anyone with a modicum of financial savvy is watching the bond market. Those with an Austrian perspective, or just plain common sense, are aghast and are using their most eloquent language to express their horror. Even the talking heads on bubble vision have finally noticed and started using relatively colorful language. For them anyway. So are we nearing the tipping point? Are the horror stories of derivatives catastrophe about to unfold. Is financial Armageddon imminent?

Well in reality, financial Armageddon has been slowly engulfing our monetary system for quite some time. And honest money advocates have been positioned far in advance of this inevitable decline. Decent profits have been booked by playing this slow motion train wreck. The big question is whether or not the tank cars are about to blow. My instincts say yes. And I am tempted to leverage all of my money on a violent end to the false dawn period (False Dawn, 3/7/03). But I am trained in the science of statistics. And I know that accurately predicting the precise timing of any catastrophic event is as rare as the event itself. Unless you count falling on your own sword.

So at times such as these, I try to sit back and relax. And stick to my basic strategy of staying long gold, silver and their shares. And periodically taking profits to acquire other hard assets. Properly playing the one sigma events on a regular basis is much more profitable than trying to leverage into even a two sigma event from time to time. Without an edge, the odds of getting it right are less than 5%. By staying properly positioned, you will profitably participate in these extreme events, as well as achieve consistent gains on the primary trend. Extreme leverage is not required.

I am more curious as to where the money is flowing from this historic sell off in bonds. From what I can tell, and as I expected, much is flowing along the path of least resistance. Back into many of the same asset classes that thrived during peak of the bubble. Stocks in particular. Even the dot cons. Those following this path are likely to be left with only tortured excuses.

But some of the money from the bond debacle seems to be finding its way to precious metals and their shares. And the bond market dwarfs the precious metals market, so an infitesimal portion of these flows could make the gold bugs wildest dreams come true. Conversely, just a bad attitude by just a few of the wise guys in these markets can make idiots of any one of us.

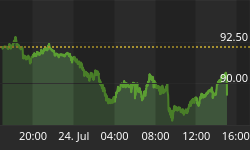

And everyone in the honest money camp seems bullish with gold at 400 by years end considered a certainty, and with 500 to 1000 next year being discussed with increasing confidence. The fundamentals strongly support this view. There is a strong technical floor under gold at this point. Silver appears to have broken out, just as I have become strongly bullish (Revolting, 7/14/03). And any of a vast array of events could act as a wealth trigger for those bullish on honest money. So virtually every pundit is at a bullish extreme.

I am in nearly complete agreement with the consensus. My anxiety over a drop in prices is at its lowest point in the past few years. And this should be scaring me. I remember several violent pull backs during this primary gold bull. And my visceral reaction. Like taking a punch in the gut. And the wise guys have monstrous fists. But the "singing in the bathroom" or the "bragging to the wife" index is not yet pegged out, so perhaps I should continue to enjoy my complacency. But that is not my nature.

So I try to be more analytical at this point. To understand this bond debacle. Both on the surface, assuming free markets of sorts, and with a cynical eye toward the machinations of global financial warfare (False Dawn, 3/7/03). To insure that I do not become collateral damage. And a financial refugee.

There seems to be an increase in the exodus of the proceeds of the sale of bonds from the US. That is, much of this decline is foreign selling. Have the Chinese begun a consistent program to sell US bonds intentionally to stress the US economy? If so we won't see that money in dollars again for many blue moons. And sensing an unstable derivatives position, the retro-Socialists in the Euro camp have fired a howitzer shell into the mortgage market. If I were one of the neo-Keynesian monetary authorities, I would have made sure that the GSEs were shielded with reactive armor. We shall see what happens as this shell impacts.

If my hypothesis regarding the incestuous relationship between the Fed and the GSEs is indeed correct (Housing Cover Clause, 6/2/03), then the GSEs are getting much help from the Fed with advance information on action and policy. That is quite an edge. And their odds of participating in a high sigma event, such as the recent drop in bond yields, are near certain. All in return for being such a wonderful source of liquidity all these years. Even recent Fed commentary seems to be front run (Bondage, 7/21/03).

The GSEs borrow short and lend long, taking a derivatives position to hedge their position. In a most admirable fashion, according to Greenspan. A shift in the direction of interest rates would leave them wrong footed. Or so it would seem.

So are the US monetary authorities in a bind? Or is this a set up? Now if I were engaged in financial warfare against the Euro and the Yuan, I would most certainly set them up. Are the neo-Keynesians in general and the GSEs in particular positioned for an unexpected and dramatic rise in rates? Are the GSEs not just hedging, but speculating? With an edge. Is a six sigma event in the offing? If so, it may be according to some sick plan. So the untenable derivatives positions can either be netted out, or unwound at the expense of the enemy (Refault, 5/10/03).

So call me paranoid. I deserve it. But I intend to survive. So I would not place short term bets on what appears to be the obvious, based upon assumptions of free market economics. I am only investing in the free market outcomes for the long haul. And hardening my stomach for the inevitable counter punch.