After several months on a fabulous run, Bitcoin has been hit hard over the past week, and it’s not just Elon Musk causing the carnage.

Two other major developments coming out of the US and China have impacted our favorite crypto, sending it into freefall.

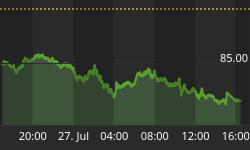

The price of Bitcoin fell below $34,000 for the first time in three months after China imposed new rules on crypto currencies.

On Wednesday, the People’s Bank of China announced that financial services companies and payment services are being banned from pricing or conducting business in virtual currencies, citing zero protection for consumers should they incur any losses from crypto transactions.

“Recently, cryptocurrency prices have skyrocketed and plummeted, and speculative trading of cryptocurrency has rebounded, seriously infringing on the safety of people’s property and disrupting the normal economic and financial order,” the regulator’s statement, issued on Wednesday, said. Chinese Vice Premier Liu He also said that tighter crypto regulation was needed to protect the financial system.

In order to curb money laundering, cryptocurrency trading has been illegal in China since 2019. The Chinese authorities issued similar bans in 2013, and in 2017.

However, even with the latest crackdown on crypto, Chinese individuals can still buy bitcoin and other cryptocurrencies and trade them on overseas exchanges.

That blast to crypto follows mounting price pressure emanating from the apparent ‘God of Crypto’, Elon Musk, whose tweets spark huge movements in bitcoin prices.

Musk suspended plans to let Tesla customers pay for cars in bitcoin due to environmental concerns about the energy required to mine them saying that it contradicts the ethos of the electric car market.

Still, Musk says that Tesla has not sold off any bitcoin it owns. In February, when Musk said that Tesla would start accepting bitcoin as a payment for EVs, the company announced in an SEC filing that it had bought $1.5 billion worth of bitcoin.

Yet another setback for bitcoin is the U.S. Treasury’s new report calling for stricter cryptocurrency compliance with the IRS.

The Biden administration proposal to strengthen tax enforcement also includes additional resources for the IRS to address crypto reporting. Under the proposal, crypto companies would have to record and report crypto transactions above $10,000, just as banks are required to.

“Cryptocurrency already poses a significant detection problem by facilitating illegal activity broadly including tax evasion,” the report said. Reporting of the crypto transfers would be set to begin in 2023.

The U.S. Financial Crimes Enforcement Network (FinCEN) has also proposed a new rule that would require cryptocurrency wallets not hosted by financial institutions in the U.S. to be tied to verified identities.

By Michael Kern for Safehaven.com