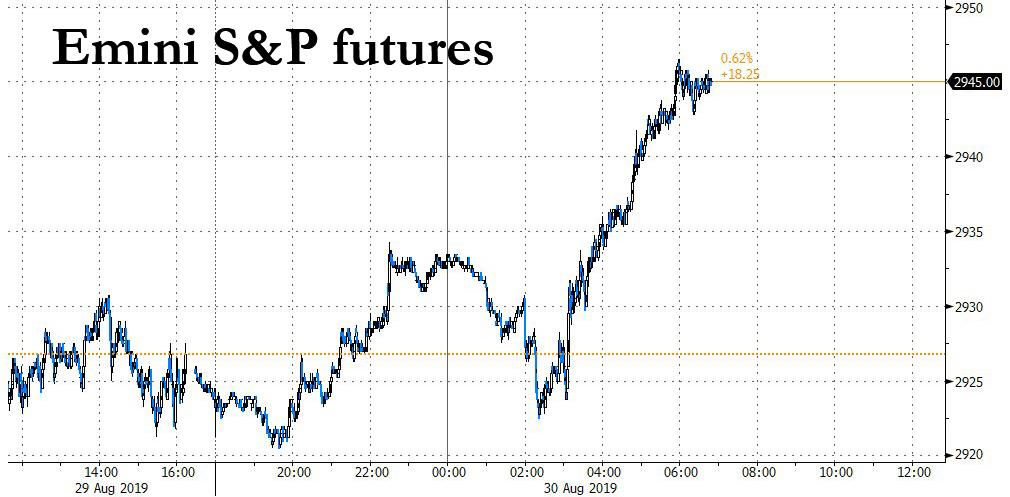

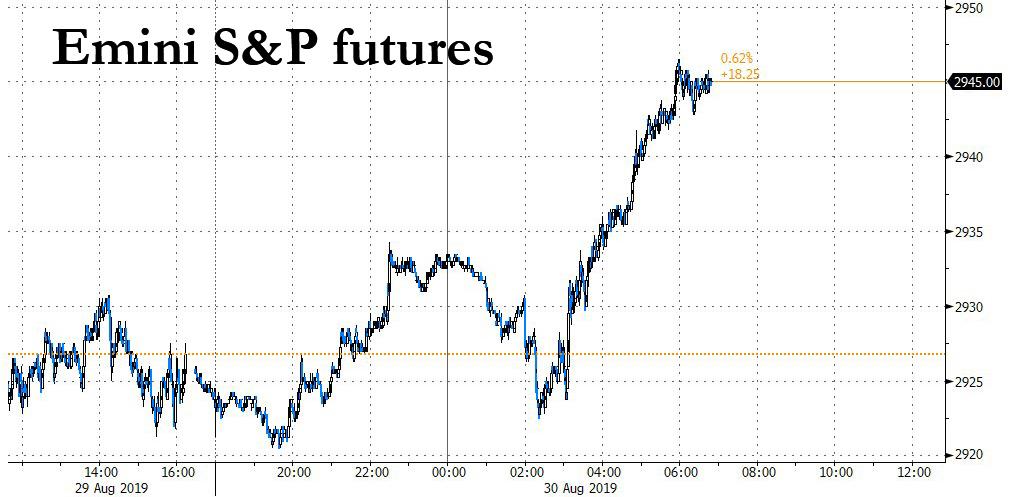

For the second day in a row, global markets and US equity futures are a sea of green with stocks pushing higher as trade headlines bathe algos in a sea of trade optimism ahead of month-end, even as the dollar ascent continued offsetting the weaker Chinese yuan which was on track for its weakest month in 2-1/2 decades.

(Click to enlarge)

On Thursday, the mood lifted after President Donald Trump said some trade discussions were taking place with China on Thursday, with more talks scheduled, even though there has been no subsequent news that any discussions did in fact take place suggesting this was yet another "fake call" report meant to boost stocks. China’s commerce ministry also said a September round of meetings was being discussed by the two sides, but added it was important for Washington to cancel a tariff increase.

There was more of the same on Friday, with US equity futures red ahead of the European open, when China's Foreign Ministry spokesman Geng Shuang said that US and China "are maintaining effective communication,” during a regular briefing Friday in Beijing. He added that "we hope the U.S. can demonstrate good faith and take real action to work in concert with China and find solutions together on the basis of mutual respect."

That little snippet was enough for algos to ignite momentum and lift the US some 20 points higher...

(Click to enlarge)

... even ignoring hawkish commentary from the ECB's Executive Board member Sabine Lautenschlaeger who said in an interview with MNI that "I don’t see the need for a re-start of the asset purchase program", adding that QE "should only be used if you have a deflation risk and a deflation risk is nowhere to be seen now."

As a result, the MSCI All-Country World Index climbed 0.3% but is on track for a near 3% decline in August - only the second month the benchmark has spent in the red this year. It was set to be the weakest August for the index since 2015.

Taking their cue from US equity future optimism, European stocks on Friday extended the previous session’s gains, with the European STOXX 600 index up 0.3% to trade at a fresh one-month high. “The trade war seesaw has certainly moved back in favor of riskier assets for now, with Trump and China supposedly holding a call yesterday,” said Deutsche Bank strategist Jim Reid, although as noted above, there has yet to be confirmation of this. The DAX outperformed (+1%), with gains helped by a surge in German real estate firms which saw the country’s DAX index add 0.7%. Related: Should The Central Bank Get Political?

Earlier in the session, the picture was more mixed in Asia, where Chinese and Hong Kong stock markets dipped in and out of the red. Arrests or detentions of pro-democracy activists in Hong Kong added to investor jitters, with the Chinese-ruled territory facing its first recession in a decade. Most Asian stocks did advance, however, led by energy producers and technology firms, after Beijing took a softer tone on possible trade talks with Washington. Almost all markets in the region were up, with South Korea and Taiwan leading gains. The Topix added 1.5%, buoyed by SoftBank Group, Sony and Takeda Pharmaceutical. Japan’s industrial output rebounded in July following the worst decline in more than a year. The Shanghai Composite Index slipped 0.2%, dragged down by Shenzhen Goodix Technology and Industrial & Commercial Bank. China’s state-backed funds added positions in high-end manufacturing industries. India’s Sensex climbed 0.3%, with HDFC Bank and Housing Development Finance among the biggest boosts. Data due Friday is expected to show the nation’s gross domestic product growth slowed for a fifth straight quarter.

Also overnight, the global Times tweeted China is unswervingly tethered to its non-stop opening-up drive and reforming its economic system, even when the country is forced into a battle of tit-for-tat tariffs with the US on a massive, unprecedented magnitude.

Meanwhile, Hong Kong rejected the appeal against the protest ban on Saturday, while it was also reported that Hong Kong arrested prominent activists Joshua Wong, Andy Chan and Agnes Chow. Subsequent reports indicate that Wong and Chow have been released

Rates markets took a breather on Friday, at the end of a stellar month that has seen prices rally and borrowing costs push deeper and deeper into negative territory. U.S. Treasury yields nudged higher overnight, with the benchmark 10-year Treasury climbing to 1.5214% from a three-year low of 1.443% touched earlier this week. And despite the 2s10s curve briefly uninverted, the 10Y yield was once again below two-year yields at 1.538%.

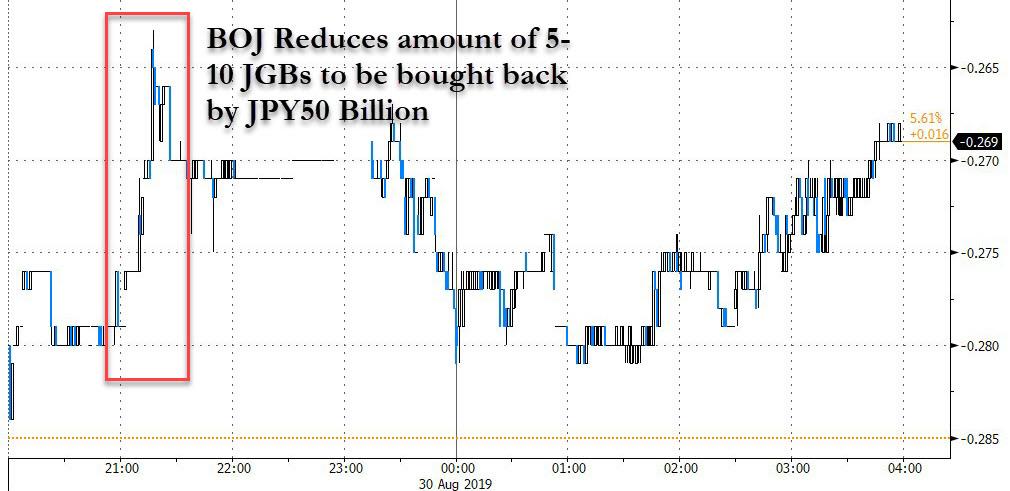

Japanese yields popped higher early in the session, after the BOJ trimmed the amount of debt it would purchase in the 5-10 year bucket for the second time in 2 weeks, this time reducing the purchase amount from 450BN to 400BN.

(Click to enlarge)

Euro zone government bond yields were steady near record lows as data showed the bloc’s inflation remained low at 1.0% in August, well below the ECB's target and bolstering expectations for European Central Bank stimulus in September. Bunds reversed early losses to trade little changed below 179.00, brushing off hawkish commentary and preliminary Eurozone inflation data that remains stuck below ECB’s target. German and US curves are marginally steeper however overall activity is muted in European hours. Italy bucks the spread-widening trend in Europe to tighten ~1bp against German 10y.

In FX, the Bloomberg dollar index was initially stronger for a fifth straight day although gains fizzled and it has since dipped into the red; SEK lags G-10 peers; ZAR leads in EM FX. The pound struggled for direction as lawmakers lost a bid to block Prime Minister Boris Johnson’s plan to suspend parliament. Elsewhere, the euro plunged to a one-month low against the dollar, as investors looked for aggressive easing by the European Central Bank and ignored doubts by some policymakers about the need for more stimulus.

Fresh trade optimism failed to inspire China’s yuan, which resumed its decline with spot yuan at 7.1462 against the dollar. The currency is on track for its weakest month since Beijing’s currency reform in 1994 after it broke through the key 7 to the dollar level earlier in August. Curiously, while both the yuan and US stocks got hit last Friday when Trump re-escalated the trade war, since then the CNH has remained deeply underwater, while the S&P has managed to recover all losses.

(Click to enlarge)

“The yuan move back to 7 and beyond has been a distinct possibility for months. It is clearly down due to the tariffs,” said Neil Mellor, senior FX strategist at BNY Mellon in London. “It does help them to some extent to absorb the tariff costs - it is one of the few options they have. The fiscal option is limited after years of excess, and the monetary stimulus has already been unprecedented this year.”

The Australian dollar, often seen as a proxy bet on the Chinese economy, slipped towards a 10-year trough.

In commodities, WTI slipped 57 cents to $56.14 a barrel while Brent fell 30 cents to $60.78 a barrel. Iron ore futures rally about 5% to conclude a torrid month, nickel rallies on supply concerns. Spot gold came off recent highs to trade at $1,526 an ounce. Silver was at $18.37 an ounce after hitting its highest level in more than two years.

Investors were focused on a string of economic releases due over the weekend including China’s official manufacturing survey, which would provide a good gauge of the real impact from the Sino-U.S. trade war.

Economic data include personal income and spending, MNI Chicago business barometer

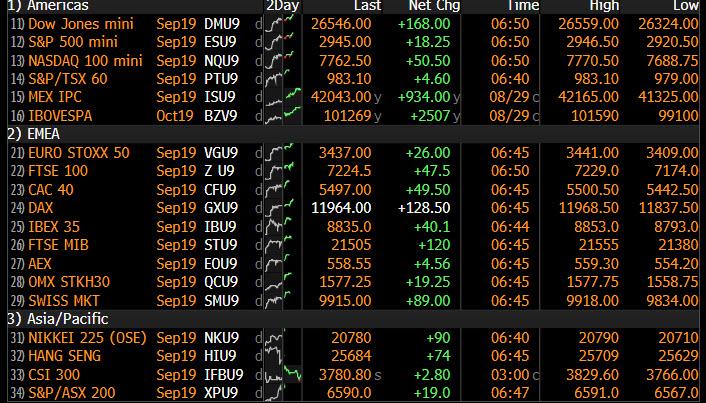

Market Snapshot

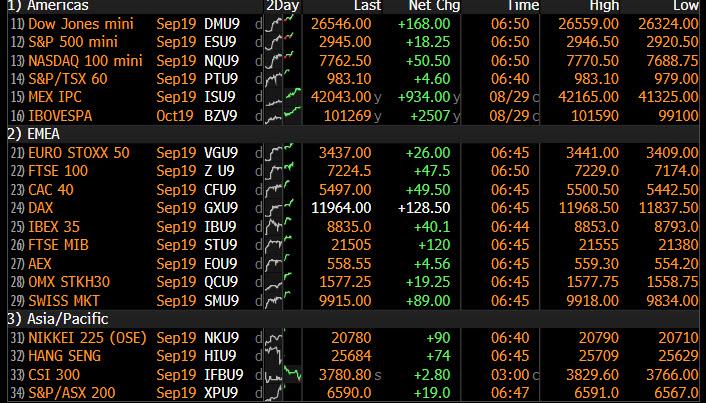

- S&P 500 futures up 0.6% to 2,942.50

- STOXX Europe 600 up 0.7% to 379.37

- MXAP up 1.2% to 152.79

- MXAPJ up 1.1% to 493.71

- Nikkei up 1.2% to 20,704.37

- Topix up 1.5% to 1,511.86

- Hang Seng Index up 0.08% to 25,724.73

- Shanghai Composite down 0.2% to 2,886.24

- Sensex up 0.4% to 37,208.51

- Australia S&P/ASX 200 up 1.5% to 6,604.22

- Kospi up 1.8% to 1,967.79

- German 10Y yield fell 0.5 bps to -0.697%

- Euro down 0.1% to $1.1042

- Brent Futures down 0.5% to $60.78/bbl

- Italian 10Y yield fell 6.0 bps to 0.642%

- Spanish 10Y yield rose 0.9 bps to 0.112%

- Brent Futures down 0.5% to $60.78/bbl

- Gold spot down 0.2% to $1,524.85

- U.S. Dollar Index up 0.05% to 98.55

Top Headline News from Bloomberg

- European Central Bank policy makers wary of ever-more monetary stimulus have fired the first warning shots two weeks before they meet to discuss bolstering the economy

- A Scottish judge refused to block Boris Johnson’s plan to suspend Parliament, dealing a blow to lawmakers who argued that there isn’t enough time to thwart a no-deal Brexit; Johnson’s Brexit team will meet with EU officials at least twice a week in September as he seeks to break the current impasse and ward off a rebellion in his own party

- President Donald Trump said Thursday that the U.S. and China are scheduled to have a conversation about trade today without giving details. His comments followed signs from China that it wouldn’t immediately retaliate against the latest U.S. tariff increase

- Hong Kong police arrested prominent opposition figures including Joshua Wong a day after banning a mass protest planned for this weekend as authorities seek to quell pro- democracy demonstrations that have raged for nearly three months; China rejected HK’s Chief Executive Carrie Lam’s plan to appease protesters, Reuters reported on Friday

- Argentina’s bonds extended declines as S&P Global Ratings cut the South American nation’s foreign- and local-currency credit ratings to “selective default” after it said it would delay payments on as much as $101 billion of debt.

Asian equity markets headed into month-end higher across the board after the tumultuous US-China trade saga took a positive turn following comments from Mofcom spurred that hopes regarding talks in September and indicated that China doesn't plan to immediately retaliate against President Trump’s latest tariff hikes. ASX 200 (+1.5%) and Nikkei 225 (+1.2%) advanced from the open with notable strength seen in Australia’s trade-sensitive sectors and as earnings continued to trickle in, while Tokyo trade was buoyant with focus on a slew of mixed data in which Industrial Production significantly topped estimates and amid reports that Japan permitted the first exports of hydrogen fluoride to South Korea since curbs were enacted. Hang Seng (+0.1%) and Shanghai Comp. (-0.1%) were underpinned by the trade hopes after Mofcom stated that both sides are discussing the September talks and that the sides have been in touch, while it also suggested that China wants to settle the dispute calmly and avoid further escalation. Furthermore, earnings have also been a driving force with firm gains in China’s largest bank ICBC, as well as oil majors CNOOC and PetroChina following their results, although upside in the broader market was contained given the looming additional tariffs and after continued PBoC inaction resulted to a consecutive weekly net liquidity drain. Finally, 10yr JGBs were lower with safe-haven demand sapped by the positive risk tone and after the BoJ reduced its purchases in 5yr-10yr JGBs to JPY 400bln from JPY 450bln for today’s Rinban operation.

Top Asian News

- China Had Rejected Lam Plan to Appease H.K. Protesters: Reuters

- BOJ Paves Way to Buy Fewer Bonds in September as Yields Slide

- China, U.S. Maintaining Effective Trade Communication: Geng

- Samsung Heir’s Retrial Spotlights Moon’s Coddling of Korea Inc.

Major European indices are firmer this morning [Euro Stoxx 50 +0.8%] as markets look to round a volatile week and month off on a positive tone, ahead of next month’s Central Bank infused slate. European bourses positivity follows on from the relatively strong performance seen in the Asia-Pac session, as sentiment received a boost on US-China updates; although, trade newsflow has been light in European hours. In terms of sectors the STXX Housing Sector (+2.2%) is outperforming on the back of reports that the rent freeze in Berlin may not be as strict as was initially feared/reported. Reports which have led to Deutsche Wohnen (+12.9%) topping the Stoxx 600, with Vonovia (+5.8%) not far behind. Elsewhere, other notable movers include Daimler (+2.3%) after being upgraded to buy at Kepler Chevreux, which has helped the auto sector more broadly (+1.7%). Separately, Deutsche Bank (+0.1%) are lagging the DAX (+0.6%) after reports that the Co. are examining the closure of local branches and are likely to begin an equity derivatives book auction in September. More broadly, the Banking index (+0.7%) remains in positive territory but is towards the bottom of the index pile, which may be partially explained by S&P downgrading Argentina’s credit rating to ‘Selective Default’ from ‘B-‘ after the country stated it would be delaying debt payments.

Top European News

- EU Concerned on U.K. Democracy After ‘Strange’ Parliament Move

- Merkel Might Be in Real Trouble If German Populists Win Sunday

- Equinor Signals Potential Early Start for Oil Giant Sverdrup

In FX, the Euro is edging closer to ytd lows vs the Dollar at 1.1027 following more dire German data (retail sales), and despite ECB’s Lautenschlaeger adding her hawkish views to those of Knot and Weidmann ahead of September’s policy meeting. Month end rebalancing flows are not providing traction/support this time as light Usd sales are touted against all G10s bar the Euro, while even the usual RHS flows/orders in Eur/Gbp seem to be conspicuously absent or relatively small given that the cross remains capped ahead of 0.9100 and the Pound is hardly firm in its own right. In terms of fundamentals, the ECB is still widely expected to deliver some form of stimulus next month even if not the big bazooka favoured by Rehn and other doves perhaps. However, hefty option expiry interest at 1.1050 (1.9 bn) could be cushioning Eur/Usd vs smaller size at the 1.1000 strike (1 bn), albeit amply backed up by barrier defences.

- USD - Notwithstanding the mostly bearish portfolio models noted above, the Greenback is only really softer vs the Yen in major markets, and the DXY has probed above resistance ahead of the 2019 peak, though remains some way below at 98.609 vs 98.932. Looming US data/surveys could give the index further impetus, but direction looks more contingent on broader risk sentiment and US-China trade developments with repercussions for Treasury yields and the curve alongside the Euro’s ability to evade further weakness.

- JPY - Bucking the overall trend, but marginally the Yen is holding a tight line around 106.50 vs the Buck following a raft of mixed Japanese data overnight and with plenty flanking the headline pair either side of the range. 1.4 bn expiries reside between 106.00-15 and the 21 DMA is only a fraction above at 106.17, while exporter supply is said to be layered from 106.70 right up to and through 107.00 at 107.10.

- CHF - In contrast to its fellow safe-haven, the Franc has retreated towards 0.9900 vs the Dollar and below 1.0900 against the Euro even though Switzerland’s KOF index was better than expected, and it appears evident that latest SNB warnings about action to curb excessive Chf demand are being heeded.

- GBP/CAD/NZD/AUD - All narrowly mixed against the Greenback, with Cable deriving some traction above 1.2150 and the 21 DMA (1.2154) to retest offers/resistance around 1.2200, while the Loonie continues to straddle 1.3300, but could finally break out of its shackles if Canadian GDP is outside consensus. Elsewhere, the Kiwi and Aussie are still top heavy on a mixture of dovish RBNZ/RBA and downbeat economic indicators not to mention negative input from RBA’s Debelle, with Aud/Usd only just hovering above 0.6700 and Nzd/Usd struggling to keep tabs on 0.6300.

- SEK/NOK - The Scandi Crowns are mixed vs the Euro, but both looking technically weak as the crosses trade above 10.8000 and 10.0000 respectively. However, the Sek is underperforming ahead of next week’s Riksbank policy meeting that could culminate in a dovish tweak to forward guidance via the timing of the likely next rate hike and/or a flatter repo path.

In commodities, WTI and Brent are in negative in territory and failing to benefit from the strong performance in stocks thus far; with WTI retreating somewhat from yesterday’s weekly high of USD 56.86/bbl and Brent painting a similar picture. In terms of catalysts there have been no fundamental updates for the complex, though its worth nothing that today is Brent’s Oct’19 future expiry which, alongside month-end flows, may be playing a role in today’s price action. Turning to metals, where spot gold has slipped somewhat on the strength in stocks and the USD’s strength this morning; as such the yellow metal looks set to finish the week just a few dollars away from its Monday open at USD 1527/oz. Separately, UBS note that iron ore prices have had a very volatile H1, and the metal is now being afflicted by slower production and supply lifts which may push it below the USD 80.0/t mark.

US Event Calendar

- 8:30am: Personal Income, est. 0.3%, prior 0.4%; Personal Spending, est. 0.5%, prior 0.3%

- 8:30am: PCE Deflator MoM, est. 0.2%, prior 0.1%; PCE Deflator YoY, est. 1.4%, prior 1.4%; PCE Core Deflator YoY, est. 1.6%, prior 1.6%;

- 9:45am: MNI Chicago PMI, est. 47.5, prior 44.4

- 10am: U. of Mich. Sentiment, est. 92.3, prior 92.1; Current Conditions, prior 107.4; Expectations, prior 82.3

DB's Jim Reid concludes the overnight wrap

elcome to the last business day of August and with it the last of the meteorological Summer (or Winter depending on where you’re reading this). Since I’ve got back from holiday it’s been dark writing the EMR again which is a little depressing! Roll on next April. We’ll do our usual full performance review on Monday but August has been a trying month for markets. However the reality is that the full range for the S&P 500 was put in place in the first 5 days of the month and although we’ve got to the bottom of that range a couple of times since we haven’t broken through and markets have bounced back off the ropes three times this month now.

Indeed that’s what’s happened this week as we’ve now had three out of four strong days since Monday including a +1.27% gain yesterday meaning that the S&P 500 is back above last Friday’s closing level which is impressive given that all the talk over the weekend was about how bad Monday’s open would be after renewed trade escalations. The trade-war seesaw has certainly moved back in favour of riskier assets for now, with Trump and China supposedly holding a call yesterday, at least according to Trump earlier in the day. However, neither side had confirmed this as we go to print. Meanwhile, risk assets were already getting a boost from the news that China doesn’t intend to immediately retaliate on tariffs, following comments out of the Ministry of Commerce just as European markets were opening. The NASDAQ (+1.48%) and DOW (+1.25%) also closed higher along with the STOXX 600 (+1.04%) as cyclical sectors led the advance. After lagging earlier this week, large-cap tech stocks outperformed, with the NYFANG index +2.15% higher.

Similarly, high yield credit spreads were also -5.5bps tighter in Europe and -4.5bps tighter in the US. As for bonds, in Europe yields ebbed and flowed as we heard comments from the ECB (more on that shortly) before bonds eventually closed weaker. Bunds and OATs both ended +2.1bps higher, while BTPs rallied another -6.1bps which saw them close below 1% for the first time ever at 0.984% while the spread to Bunds compressed to 167.6bps. Across the pond 10-year Treasuries ended +1.2bps higher (up a further +2bps this morning), though 30-year yields fell -1.2bps (but are back up +1.4bps in Asia) after press reporting (Bloomberg) suggested that the Treasury Borrowing Advisory will argue against ultra-long bonds. The 2s10s yield curve flattened another -0.8bps to -3.5bps (at -2.1bps this morning) after nearly getting back to flat as Europe went home.

Just on those ECB comments, it’s significant that these were the first public comments from Lagarde on monetary policy since being given the ECB job, which she’ll take up in November. That was enough of a reason for the market to react (albeit modestly), however the actual substance was not particularly ground-breaking. Lagarde said that the ECB hasn’t hit the lower bound on interest rates and that the latest decisions of the ECB including forward guidance “are in my view correctly aimed at preserving the very accommodative financing conditions for firms and households”. The comments felt almost Draghi-esque and hinted at continuity more than anything else, rather than suggesting any preconceived conclusions. That said, it does seem like Lagarde is likely to be at least marginally more sensitive to the adverse side-effects of negative interest rates, saying "it is clear that low rates have implications for the banking sector."

Later in the day we also heard from the ECB’s Knot. The initial headline that popped up quoted Knot as saying that “there is no need to resume QE right now”. Knot also said that “market expectations are overdone” and that “I would be reluctant to back tiering for negative rates”. Yields and the euro spiked on the news however it’s worth noting that Knot is already one of the more hawkish council members but importantly not a member of the executive board, commentary from which will ultimately be more important. That being said recent comments from the ECB do suggest a wide range of views and an elevated level of uncertainty around what policy package will be unveiled next month.

This morning in Asia markets are following Wall Street’s lead with the Nikkei (+1.30%), Hang Seng (+0.69%), Shanghai Comp (+0.23%) and Kospi (+1.87%) all up. As for FX, all G-10 currencies are trading weak this morning (c. -0.1% - -0.2%) while, the onshore Chinese yuan is trading down -0.11% at 7.1521. The South Korean won is trading up +0.68% as the country’s central bank shied away from cutting rates at today’s monetary policy meeting. Elsewhere, Futures on the S&P 500 are up +0.20%. In terms of overnight data releases, we saw Japan’s July retail sales come in at -2.0% yoy (vs. -0.7% yoy expected) while preliminary July industrial production came in at +0.7% yoy (vs. -0.6% yoy expected). In other news, the BoJ reduced purchases of bonds in the key 5-10 year maturity zone for a second time this month as the country’s benchmark yield dropped to near record lows. The central bank offered to buy JPY 400bn of 5-10 year bonds today (vs. JPY 450bn at its previous regular operation). 10Y JGB yields rose after this and are currently up +1.4bps to -0.283%.

Meanwhile, here in the UK, Bloomberg reported overnight that PM Johnson’s envoy, David Frost, has asked the EU to intensify Brexit talks at a meeting with European Commission officials in Brussels on Wednesday. The report went on to add that David Frost will meet with EU officials at least twice a week in September to break the Brexit impasse.

In other news, the data in the US yesterday included the second revision to Q2 GDP however there were no great surprises with growth revised down a tenth as expected to +2.0% yoy. The details did show a significant upgrade to consumption of four-tenths to +4.7% however core PCE was revised down a tenth to +1.7%. It’s worth noting that we’ll get the July PCE data today where the consensus expects a +0.2% mom reading. All in all though, not much to change Fed expectations from the latest data. As a side point it’s worth also noting that corporate profits made a big jump in Q2 having dropped in Q1, with profits up +2.7% yoy. These have historically led the trend in GDP, so a modest positive.

As far as the rest of the data was concerned, the advance goods trade deficit in July narrowed to $72.3bn and a bit more than expected, while wholesale inventories climbed +0.2% mom as expected last month. Initial jobless claims printed at 215k and further indicate the resilience of the labour market, while pending home sales in July fell -2.5% mom.

In Europe the main talking point from the data was a soft German inflation print. Indeed CPI printed at -0.1% mom in August which lowered the annual rate to +1.0% yoy and the lowest since November 2016. The details showed that the core was weak which raises downside risks to the Euro Area core reading today. Elsewhere, in France Q2 GDP was revised up a tenth to +0.3% qoq.

To the day ahead now, where this morning the main focus will be on the August CPI reports for the Euro Area, France and Italy. We’ll also get the final revisions to Q2 GDP in Italy and July money and credit aggregates data in the UK. Inflation data should be the main focus in the US too with the July PCE report and personal income and spending numbers. We’ll also get the August Chicago PMI number and final August University of Michigan consumer sentiment survey revisions. Away from that, the ECB’s Rehn speaks in Finland this morning

By Zerohedge.com

More Top Reads From Safehaven.com:

{kind=link}

{kind=link}

{kind=link}

{kind=link}