It’s now just over a year since Canada legalized recreational use of marijuana, and Wall Street is thoroughly disappointed.

What was supposed to have been a massive killing in one of the hottest new markets has been worse than lackluster.

It’s not that Canadians aren’t smoking enough pot, and it’s probably not that there’s too much supply: Instead, it’s more likely that the new companies in this business, and the government strategy in this case, aren’t doing the fledgling industry any favors.

A much clearer, if not dire picture emerges with the culling of cannabis stocks following Q3 earnings releases.

The disastrous results show a lineup of companies who haven’t been able to come up with a good strategy for growing, packaging and distributing. They haven’t been able to make legal weed more attractive than illegal weed. Perhaps it was a bit presumptuous to simply think that making it legal would bring all weed smokers to their doorsteps.

It’s hard to sell when there’s nowhere to sell. The Canadian province of Ontario, for instance, is the largest and has only 25 cannabis stores.

But it’s not all total doom and gloom.

Here’s what happened to the cannabis darlings for Q3:

#1 Canopy Growth (NYSE:CGC)

(Click to enlarge)

Investors have severely punished Canopy Growth, and anyone left holding the bag will have lost quite a bit. That’s bad when this is the largest player on the market, making it a barometer of sorts.

CGC shares had shed 29% by the end of last week, with a 45% loss in shareholder value year-to date. Based on fiscal Q2 earnings, CGC showed losses of 81 cents per share on revenues of $57.78 million. That was far worse than Wall Street estimates, which had losses at 31 cents on sales of $75.42 million.

CGC missed the mark by a margin that’s sent shareholders running.

Does it mean that investors should be ditching CGC entirely? Not in our opinion. What it means is that now is a good time to get these stocks on the cheap. The great cannabis rollout didn’t happen as quickly as it should have but it will happen, and there will be other positive developments.

CGC has a partnership with Constellation Brands (NYSE:STZ) for cannabis-based drinks, and eventually, the provinces will sort out the sales points so it makes sense and brings customers off the streets.

CGC is also gearing up to roll out its cannabis derivative products next month.

#2 Aurora Cannabis (NYSE:ACB)

(Click to enlarge)

For Aurora, it was another disastrous earnings report, with net sales at CAD$75.2 million, consumer cannabis sales down 33% and wholesale revenues almost cut in half. Operating expenses were up and losses compounding, and the new strategy to cut costs will mean that Aurora’s plan to hit production of 625,000 kilos by the end of June next year won’t make it.

It’s planning to reduce CAPEX and delay the construction of its Aurora Nordic 2 and Aurora Sun facilities.

#3 Aphria (NYSE:APHA)

(Click to enlarge)

Aphria actually broke the mold here with a stronger earnings showing, but that hasn’t helped the stock much because everyone’s down on cannabis across the board.

Part of the reason Aphria is faring better is because it’s focused mostly on the medical marijuana market. Still, Aphria managed net revenue growth of 8% for adult-use cannabis. Likewise, Aphria’s adjusted EBITDA saw a four-fold increase, and it’s got nearly $500 million in cash and marketable securities.

APHA has also just received its cultivation license from Health Canada for its Aphria Diamond subsidiary, which will have an annual production capacity of 255,000 kilograms when fully operational.

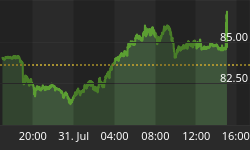

#4 Cronos (NASDAQ:CRON)

(Click to enlarge) While also disastrous, Cronos, by default, seemed better off than Canopy or Aurora after the earnings culling. It’s net sales only just missed Wall Street’s expectations, coming in at CAD$12.7 million. And that was up from Q2. It looks like Cronos actually defied the norm and posted a quarterly profit of CAD$788 million; however, that was really an accounting trick connected to Altria Group’s equity investment.

Related: Lack Of Funding Could Lead To Battery Metal Supply Shortage

Still, the picture isn’t great. The numbers still show sales prices sliced in half. That will mean lower output for Cronos, too as operating expenses get slashed.

#5 Tilray (NASDAQ:TLRY)

(Click to enlarge)

Tilray saw its shares have lost less than any others in this space.

That’s not to say that Tilray’s earnings report was great. It wasn’t. It wasn’t even good. It was just better than the others, and the only thing that made it so was its acquisition in Q1 of Manitoba Harvest, a leading hemp foods industry player. Manitoba is actually profitable and helped Tilray generated $120 million in revenue in the first 9 months of this year.

While the cannabis side of Tilroy saw $35.5 million in sales and $27.5 million in operating losses, the hemp food side saw $4.2 million in profits on $15.6 million in sales.

Bottom Line: Black Market Is Still King

Cannabis companies need to be hedging their bets and bit more widely in this transition phase. Tilroy is the only one that’s doing that with mild success at this point, but the jury isn’t out on this definitively.

The underlying problem is structural for this industry in Canada. Canadians are still buying illegally, according to a National Cannabis Survey from Q2. Over 40% said they buy at least some of their pot from an illegal source. That’s largely because opening up a legal shop is still too cumbersome and restricted a process--unless you’re a former cop or politician, it would seem.

By Anes Alic for Safehaven.com

More Top Reads From Safehaven.com: