It’s Q3 earnings time, with big banks up first, followed by a couple of tech giants and that streaming beast, Netflix, plus Coca-Cola and United Airlines.

The trade war is still calling the shots, even though the market can’t quite decide from one moment to the next whether a deal has actually been struck and the global economy can breathe easy, or whether it’s all smoke and mirrors and we’ve been duped again.

By some accounts, the S&P 500 is destined to see at least a 3-percent drop in profits this quarter, but it’s defied similar expectations before.

The elephant in the room is, again, the trade war and how much it’s hurting company profits, as well as what this week’s retail sales figures have in store for us.

First up is JPMorgan, Citigroup, Wells Fargo, BlackRock and Goldman Sachs--all on Tuesday, along with United Airlines. On Wednesday, we’ve got IBM, Honeywell and Alcoa, followed by Coca-Cola on Friday.

None of our picks are on the list of earnings set to come out this week. Our top three for this earnings season are just slightly further out.

#1 Brookfield Asset Management (NYSE:BAM)

(Click to enlarge)

BAM is a Berkshire Hathaway company focus on alternative asset management. It’s beat estimates for the past three quarters. Q3 earnings are scheduled for November 13th, and out of nine analyst ratings, all of them are ‘BUY’.

It’s hard to find a better long-term buy than this expertly managed company whose guidance has plan value going from $68.9 billion to $149 billion in five years. This is a great company for increasing shareholder value.

It’s comparable to Blackstone, another alternative asset management heavyweight, but we like BAM better. BAM also directly invests in its sponsored private equity funds and actively manages the businesses it controls. In other words, it’s got a ton of skin in this game, pumping over $44 billion into these investments through its four partnerships with Brookfield Property Partners, Brookfield Infrastructure Partners, Brookfield Renewable Partners and Brookfield Business Partners.

Some figures to keep in mind are the $1.1 billion in fee-related income BAM took in last year, plus the $1.7 billion in dividends. After interest and taxes, BAM saw $2.4 billion in free cash in 2018. That will potentially reach $4 billion within 5 years, or, $60 billion in 10 years.

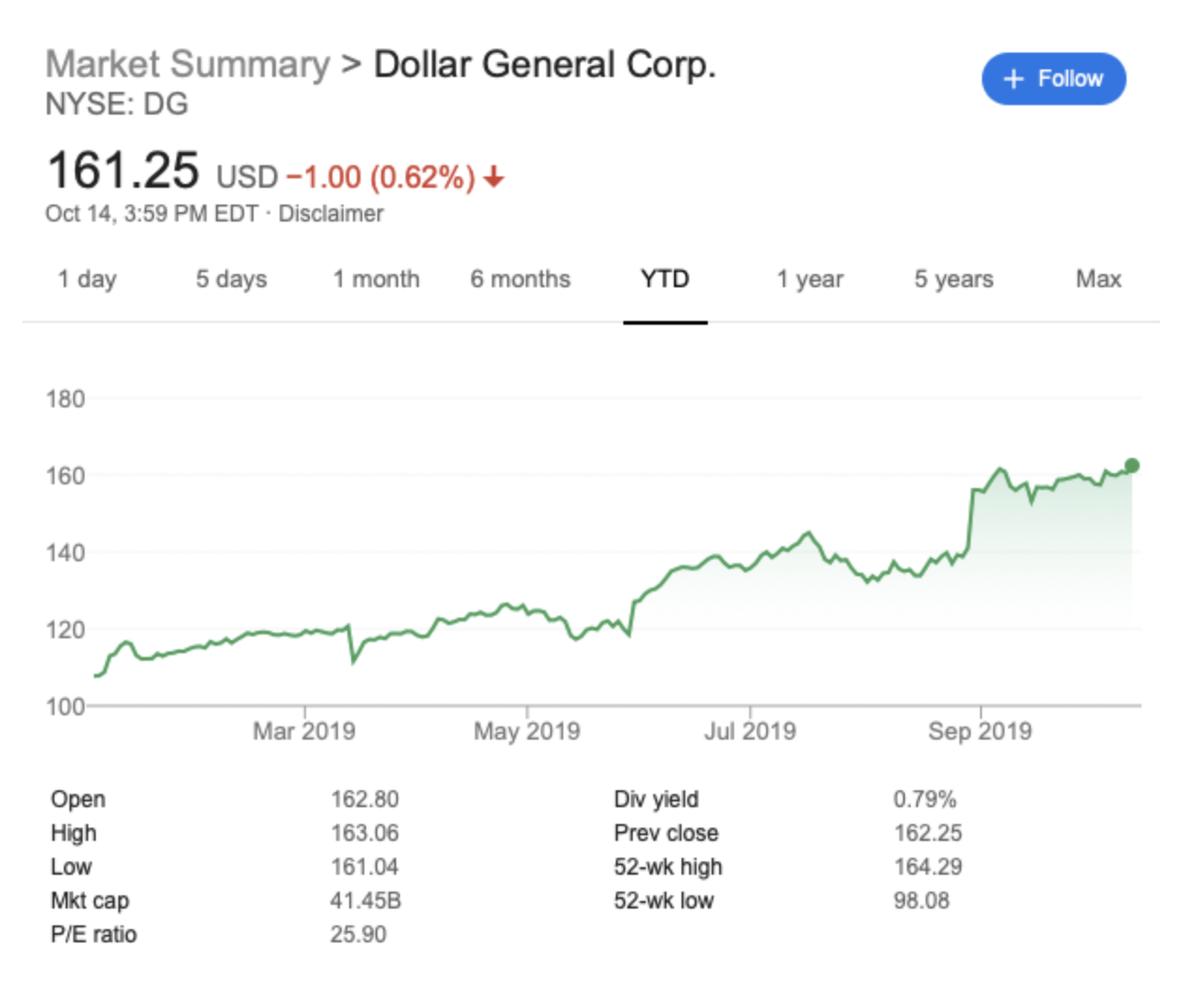

#2 Dollar General Corp. (NYSE:DG)

(Click to enlarge)

It’s probably not your favorite place to shop but in the dying world of brick-and-mortar retail, Dollar General is the new king, thanks to a 50-percent spike in its share price year-to-date.

Related: SoftBank Reeling After Questionable WeWork Investment

So can there still be more upside? Yes, we think so. It’s still opening new stores while everyone else is closing down in a veritable retail apocalypse. And the new openings are real--and covering real demand, apparently.

DG is also working on major product expansion and remodeling, including a ‘Fresh” initiative for more refrigerated products.

And next up, self-checkout, which is already in progress.

If there’s a recession, nothing will hit this stock. In fact, it might get even better. It’s a sound bet all the way around and in multiple scenarios.

DG’s Q3 earnings are scheduled for December 2nd.

#3 Shopify (NYSE:SHOP)

(Click to enlarge)

Earnings are out for Shopify on October 29th, and as of the time of writing we’re looking at a share price of $344 on a market cap of over $37 billion. This is the power of e-commerce, and believe it or not, it’s not all about Amazon and eBay.

Shopify (Canadian) is growing because it gives e-commerce companies a way to build their own online stores. So we’re looking for more good news this quarter, keeping in mind that in Q2 SHOP posted a 48-percent year-over-year increase in revenue. And it’s still in major expansion mode with a recent warehouse fulfillment acquisition that cost $450 million and includes everything SHOP needs to take this is the next Amazon-bound direction.

By Fred Dunkley for Safehaven.com