Stocks were trading up early on Friday and then mixed later in the afternoon, but one thing most analysts agree on is that expectations are high for this earnings season.

Bank earnings started the market off on an optimistic note and a view of the bottom, with JPMorgan Chase & Co. reporting a 35-percent increase in first-quarter profits, but then seeing its stock fall 2.6 percent in afternoon trading.

But now this is about to circle back to a story about true fundamentals, rather than Tweets about things that aren’t really happening.

Fundamentals means earnings, and analysts are expecting a strong first-quarter showing. In fact, they expect some of the strongest earnings and revenue growth in years. Why? Part of it is psychological: Everyone’s looking for justification right now that the market isn’t overvalued after all.

Whether it will truly be the strongest earnings season since the Great Recession, as some believe, we’re not so sure, but here are 3 stocks worth watching as we get back to the fundamentals:

#1 Netflix (NASDAQ:NFLX)

(Click to enlarge)

Online streaming giant Netflix is up 61 percent year-to-date, and it has a track record of surprising us with earnings that beat expectations, pretty consistently. Many think there’s no reason to think they won’t do it again. Of course, it’s hardly a contrarian thought, so we risk losing out of great expectations: When too many expect a stock to beat earnings expectations, if they hit but don’t go over, it may be considered a loss. It all depends how sentiment was going in. But earnings are scheduled for April 16, so you won’t have to wait long to find out.

For the most part, Wall Street analysts are expecting to see Q1 EPS of $0.64 for Netflix with revenue of $3.69 billion. That would mean massive year-on-year growth if it happens. So expectations are already high.

What do the analysts say?

“While there is certainly a bullish sentiment surrounding the stock, we think that many investors still underestimate the Netflix story particularly with respect to the penetration opportunity around the world,” according to Rob Sanderson of MKM Partners. “We think that continued subscriber momentum, both domestic and international will lead to a rethinking of earnings power.” Sanderson’s price target? $320. Related: Wells Fargo Faces Record $1B Fine In Lending Scandal

Todd Gordon of TradiingAnalysis.com concurs with that price target, watching the charts. Gordon told CNBC’s Trading Nation that “it looks like we should be able to retest at least $320 and possibly the old highs of around $340 if we have a good earnings report”.

(Click to enlarge)

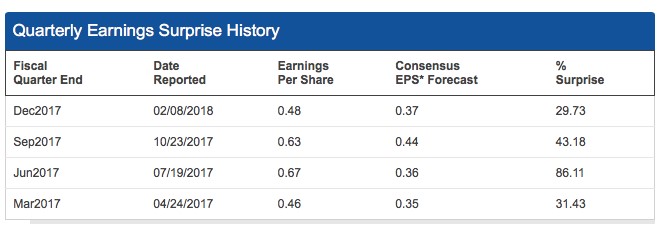

#2 T-Mobile US, Inc (NYSE:TMUS)

T-Mobile is the third-largest carrier in the U.S. and it’s been an aggressive bull against the competition this year. When it comes to growth, it’s a clear leader for years running. And while earnings are anxiously awaited, there’s another major story moving this one: Merger talks with Sprint have restarted.

(Click to enlarge)

While rival AT&T is caught up on a lawsuit over its merger plans with Time Warner, T-Mobile has swooped in to capitalize on that with Sprint. A combined T-Mobile and Sprint would be a crazy powerhouse that would outdo AT&T in size and catapult T-Mobile to No. 2 position, right behind Verizon. Any hints about regulatory approval for this merger will be a major stock mover; and so far, sentiments seems to be that the authorities aren’t going to have qualms about this one.

Q1 earnings are also expected to shine.

“We expect TMUS to deliver upbeat financial results following its better balance of sub growth and margins,” Oppenheimer analyst Timothy Horan told Investorplace, who “expects TMUS to capture the majority of the postpaid phone flow share in the quarter at ~100% down from ~400 percent Y/Y, as the company better balances FCF with growth and competition has been muted.”

Related: China Ups Pressure In Artificial Intelligence Race

His price target on the stock is $75, a 25-percent increase.

On Monday, Deutsche Bank increased their price target on TMUS to $72.00, with a “buy” rating.

Earnings will be on April 23, and the analyst consensus is ‘buy’.

(Click to enlarge)

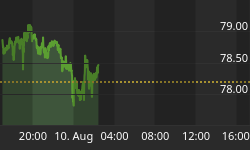

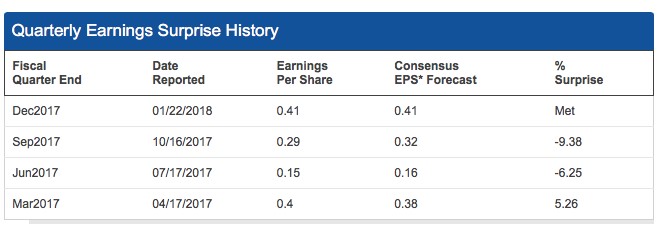

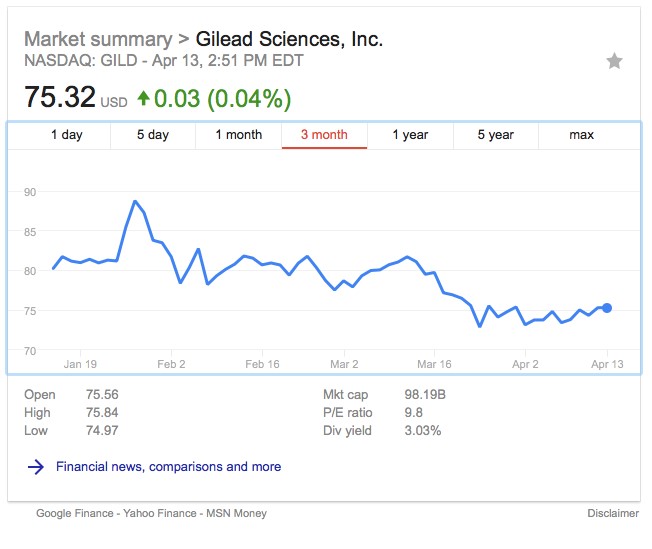

#3 Gilead Sciences Inc (NASDAQ:GILD)

Everyone’s been glued to the screen on tech given the wild ride for the sector’s stocks this quarter, and for the first time in a while, biotech has been sidelined. Then there’s Gilead, which has been suffering lately because of a major hit to revenues for its key hepatitis franchise. The stock lost half of its share price from its high of $120 in 2015. Now, the argument is that it’s undervalued and its hepatitis revenue losses have already been factored in.

(Click to enlarge)

Last year, Gilead transformed their business model and made an $11.9-billion foray into cell therapy with the acquisition of Kite Pharma, a developer of CAR-T. What this move did was diversify Gilead beyond its hepatitis C and HIV focuses. And some also expect the company’s HIV franchise to make a strong showing in Q1.

RBC Capital’s Brian Abrahams expects a strong quarter “as the mix shift of HIV revenues continues to track more favorably for GILD’s long-term life cycle.” He’s got a $94 price target on the stock, or 26-percent upside.

Earnings are scheduled for May 1, and Zach’s 7-analyst consensus EPS forecast is $1.59 for the quarter, compared with $2.2 for Q1 2017. Will there be any surprise this time around? Possibly, but a positive surprise might also wait until Q2.

(Click to enlarge)

By Tom Kool for Safehaven.com

More Top Reads From Safehaven.com: