With economists predicting the rise of mortgage rates in 2019, and with the U.S. housing market looking less than spectacular as of the first quarter of this year, a relatively new concept of “homeownership investment” is gaining traction.

And the offers are increasingly tempting, especially for homeowners who need cash and aren’t ready to go the traditional bank-generated home equity loan because they don’t want to make the monthly payments on principal and interest.

The lure of the “homeownership investment” scheme is that there aren’t any monthly payments to make. Instead, homeowners are letting investors buy equity in their home and make money on the appreciation.

But the lure of short-term easy cash has a long-term risk.

On the surface, it seems relatively simple. Investors give homeowners cash in advance on their home equity, and homeowners pay no monthly payments. When the home is sold, the homeowner repays the equity cash, plus a portion of the profit if the house sells for more than it was worth at the time of the investment.

This is how the investors get their money back—or how they lose on their investment.

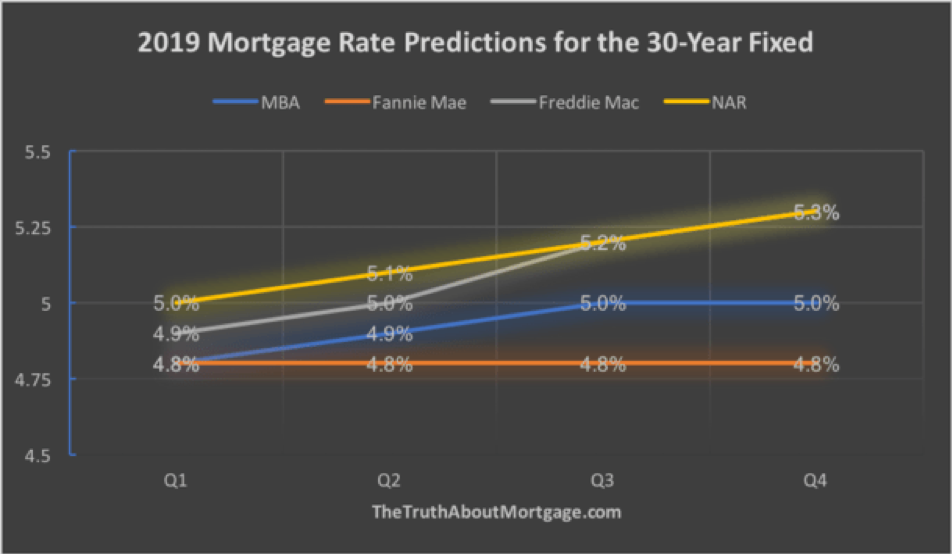

And it’s gaining traction because of tight housing supply and rising home prices, not to mention mortgage rate predictions that are making banks look less attractive:

(Click to enlarge)

Source: TheTruthAboutMorgage.com

According to Federal Reserve data, rising home prices have created record levels of equity for U.S. homeowners, reaching an estimated $15 trillion in December 2018. Related: Is Germany’s New Industrial Strategy Good For Its Economy?

So, who is operating in this space now? The pioneer appears to be San Francisco-based Unison, which has been offering homeowner investments since 2007, in what they call debt-free cash.

That the service is gaining traction is best illustrated by the fact that Unison is claiming 370 percent growth in revenue last year, and a 308-percent increase in customer transactions from the previous year. By the end of 2018, Unison boasted $2.42 billion in co-invested residential real estate in its portfolio.

Naturally, those results have lured others into the space, as well.

But in many ways, it still smacks of desperation on the part of homeowners, and desperation rarely results in a long-term win.

Essentially, homeowners are selling their equity to the investor and the cost of that sale will not be known until the home is sold. It removes any gains you might get from rising home prices, in return for immediate cash. If your home sells for much more than its original appraised value, you’ll end up losing much more than the price of the equity you sold.

And in cases where the deal was a fixed period, and not the sale of the home, if appraised value at the close of the period is higher than when the equity was sold, some homeowners might find themselves forced to sell prematurely just to pay off the investment. And if they don’t want to sell—or can’t sell—it means taking out a loan to pay it off.

It sounds easy and simple—and it is. It also makes sense for investors right now betting on the tight supply and rising prices. But many might also miss the fine print on the transaction cost of this deal, which is about 3.9 percent. It’s not free money; it’s quick cash that means forfeiting future profit.

Related: Scientists Take Rare Look Inside 'Wire Gold' Specimen

In other words, this is a profitable exercise only for investors—not for homeowners. For homeowners, this may be a good replacement for a traditional home equity loan when you need cash and need it now and don’t want to go into debt. This isn’t a loan, after all, which is the genius of it. It’s an investment.

What it does do is offer homeowners some financial flexibility—especially those who need that flexibility right now, to send their kids to college, or retirees, for instance.

Traditional mortgage lenders, though, should feel threatened by what Unison calls the “evolution” in home ownership because it doesn’t end here.

Now, Unison—in partnership with Goldwater Bank--is taking this offer in yet another direction: It’s helping with down payments on homes by allowing homebuyers to put 5 percent down on 80-percent loan-to-value mortgages, while Unison provides 15 percent in return for a share in the appreciation, assuming the home actually appreciates.

By Fred Dunkley for Safehaven.com