The U.S. dollar has fallen rather sharply over the past year or so, despite ongoing Fed rate hikes. This persistent dollar weakness has really boosted gold. There’s a fascinating interplay between these two currencies and futures speculators’ expectations for Fed rate hikes. These traders hang on every word from top Fed officials, which greatly influences their trading. So, these relationships are important to understand.

In late December 2016, the venerable U.S. Dollar Index surged to an incredible 14.0-year secular high. That was just a couple weeks after the Federal Reserve’s second interest-rate increase of this hiking cycle. Top Fed officials were forecasting three more rate hikes in 2017, fueling euphoric sentiment in this top reserve currency. Everyone believed higher prevailing interest rates would prove very bullish for the dollar.

Their logic was simple. The more the Fed raised its benchmark federal-funds rate, the more general rates would rise. That would boost the yields of dollar-denominated bonds led by US Treasuries. The higher yields went, the more attractive the dollar would look compared to other major currencies. Thus, global investors would flock back to the U.S. dollar as the Fed hiked, further extending the mighty dollar bull.

That very week I wrote an essay taking an unpopular contrary stance on the euphoric US dollar. In it I warned, “Traders are overwhelmingly betting the dollar’s strong upside will continue. But this greed-drenched currency looks very toppy and ready to fall, which is very bullish for gold.” That generated a lot of flak, but it’s usually the right decision to be bearish when everyone else is bullish near major secular highs.

Shocking traders, late 2016’s epically-overcrowded long-dollar trade indeed collapsed in 2017. That was despite the Fed actually carrying through on hiking three more times as expected. From that euphoric dollar peak in late December 2016 to the recent low, the USDX plunged 14.2 percent over 13.2 months! By world-reserve-currency standards that’s massive. This helped gold surge 18.1 percent higher over that same span.

Clearly the usual higher-rates-are-great-for-the-dollar arguments everyone believed in late 2016 weren’t correct. Nevertheless, futures speculators continue to trade based on that faulty premise almost every week. They rush to buy US-dollar futures and sell gold futures whenever something seems hawkish and implies more or faster Fed rate hikes. Once you start watching for this phenomenon, the examples seem endless.

The triggering catalysts are often comments from top Fed officials, official statements released after their policy-setting FOMC meetings, those meetings’ projections for future federal-funds-rate levels, and any major U.S. economic data that surprises to the upside. Anything from these sources considered hawkish is used as an excuse to aggressively buy the dollar, which in turn convinces gold-futures speculators to sell.

These elite futures speculators still fervently believe higher yields driven by Fed rate hikes will boost the dollar. For many years now most sizable daily dollar rallies and gold selloffs have emerged from more-hawkish perceptions on Fed rate hikes. But while the basic logic sounds reasonable, this ever-popular thesis is torpedoed by market history. Futures speculators would do way better if they understood this.

This first chart takes a multi-decade view of that U.S. Dollar Index and the Fed’s benchmark federal-funds rate. The FFR is actually a free-market interest rate the Fed can’t directly control. Banks are required to maintain reserves at the Fed, which they can borrow or lend overnight if they have temporary deficits or surpluses. This is the federal-funds market. The FOMC actually sets a target for the federal-funds rate.

(Click to enlarge)

For a decade now, this target has been a quarter-point FFR range. The FOMC’s latest target from its late-January meeting is 1.25 percent to 1.50 percent. The Fed uses open-market operations to attempt to bully the actual FFR into its target range. This chart shows the midpoint of the Fed’s target range. It’s not only far less volatile than the real FFR, but the Fed rate hikes so enthralling futures speculators are target-range changes.

Because of the extreme leverage inherent in futures trading, speculators necessarily have an ultra-short-term time horizon. They can’t afford to be wrong for long at 25x or greater leverage. So, these guys are often making trades they intend to hold for mere hours or days, maybe a couple weeks on the outside. They are so deep in the ultra-short-term weeds that they can’t see the forest for the trees on Fed rate hikes.

The Fed’s current rate-hike cycle, which is actually the 12th since the early 1970s, was born in December 2015. That initial hike was highly anticipated, as the Fed hadn’t boosted its FFR target for fully 9.5 years! The Fed began to prepare the markets for a new tightening cycle back in mid-2014. The FOMC started to talk hawkish after long years of its zero-interest-rate policy implemented during 2008’s extreme stock panic.

On mere rate-hike hopes, the USDX skyrocketed 25.6 percent higher over 8.4 months between late June 2014 and mid-March 2015! That was truly epic, the USDX’s second biggest and fastest rally ever witnessed. It was only exceeded by a blistering 22.6 percent USDX rally in just 4.2 months during that 2008 stock panic on colossal safe-haven buying. Dollar speculators were unbelievably bullish on the coming Fed rate hikes.

Since this 12th Fed-rate-hike cycle began in late 2015, the Fed has indeed hiked 5 times totaling 125 basis points. That’s not trivial coming off ZIRP, representing a gargantuan 11x increase in the midpoint of the FFR target range! In absolute-percentage terms that’s history’s most-extreme hiking cycle since it started from such a low base. So, the resulting higher yields should’ve driven the USDX much higher, right?

But that’s not what happened. Even at late-December 2016’s extreme 14.0-year secular high, the USDX was only 5.2 percent above its levels from the day before this cycle’s maiden rate hike just over a year earlier. And over this entire 12th rate-hike cycle’s 26.5-month span, the USDX has actually slumped 7.7 percent lower! Obviously Fed rate hikes aren’t as bullish for the US dollar as futures speculators continue to widely believe.

That’s no anomaly either. The previous Fed-rate-hike cycle, the 11th of the modern era, ran from June 2004 to June 2006. And unlike our current one, the USDX entered that last one near major secular lows. It also saw far-more-relentless Fed hiking, many more hikes faster. The FOMC raised its FFR target every meeting for 17 in a row! These 17 rate hikes totaled 425 basis points, dwarfing the current cycle’s 125 to date.

If there was ever a recipe for a strong USDX bull, that was it. But instead of soaring on higher yields as traders assume happens, the best the dollar could muster was a sideways grind. Over that hiking cycle’s entire span, the USDX actually drifted 3.8 percent lower! The Fed’s higher interest rates indeed drove higher yields, but they didn’t convince global investors to flock back to the dollar. So, it gradually slumped in that cycle.

Maybe it’s high-rate stability the dollar needs. But in the 14.7 months after that last Fed-rate-hike cycle as the Fed’s FFR target stayed way up at 5.25 percent continuously, the USDX actually slid a sharp 8.0 percent! There needs to be hard historical evidence that Fed rate hikes are bullish for the US dollar. This belief driving so much big intraday trading shouldn’t be held on mere blind faith. The USDX hasn’t thrived in higher rates!

The other side of this coin is lower rates must hurt the dollar. There’s some support for that at least, as the USDX plunged to an all-time low in mid-April 2008 following the FOMC slashing rates. In just 6.0 months the FOMC sliced the FFR more than in half from 5.25 percent to 2.25 percent! Yet despite the FFR target plunging further to a 0.0 percent-to-0.25 percent ZIRP range in December 2008 during the stock panic, the USDX soared. Related: Trump’s Tariffs: “Trade Wars Are Good”

The big down days in that first stock panic in 101 years became more frequent and larger from July to November 2008. So, traders increasingly dumped stocks to hold cash. That safe-haven demand again blasted the USDX an astounding 22.6 percent higher in just 4.2 months! Yet over that span the FFR target was cut in half from 2.0 percent to 1.0 percent. So, falling yields courtesy of the Fed certainly didn’t negate dollar panic buying.

And if lower yields are so bearish for the US dollar as the Fed-hawkishness-is-bullish arguments imply, the USDX should’ve plummeted during the ZIRP years. Yet the dollar instead largely ground sideways near lows. From the day before the Fed went ZIRP in December 2008 to late June 2014 just before that sharp rate-hike-anticipation rally erupted, the USDX merely edged 2.8 percent lower over a long 5.5-year ZIRP span.

See the glaring disconnect here? The only places where Fed rate hikes are bullish for the US dollar and rate cuts are bearish is in futures speculators’ minds! They hold this belief so strongly that they managed to bid the USDX sharply higher in anticipation of a new Fed-rate-hike cycle from mid-2014 to early 2015. But during times of actual Fed rate hikes and cuts, the USDX hasn’t bothered following this model at all.

This hard-historical precedent of U.S.-dollar trading action compared to FOMC FFR target changes ought to dispel futures speculators’ false beliefs. Yet as evidenced by their collective trading they continue to fervently believe this fantasy they have concocted. This is utterly baffling, as these elite traders running such extreme leverage can’t risk having emotions cloud real probabilities. That can spark big and fast losses.

Yet just watch. Like clockwork the next time some Fed-hawkish news catalyst arises, the U.S. dollar will surge on heavy futures buying. It could be Fedspeak, an FOMC statement, its accompanying dot plot once a quarter, or a sizable upside surprise on major U.S. economic data. Traders will again rush to buy dollar futures on their groupthink assumption that higher yields from Fed rate hikes will boost the U.S. dollar.

While the psychological pathology here truly lies in the U.S.-dollar speculators, their kneejerk behavior has a big impact on gold. The world gold market is pretty opaque, with hard fundamental supply-and-demand data mostly only reported quarterly or monthly at best. So gold-futures speculators with their ultra-short-term outlooks necessitated by extreme leverage must find something else to watch for their own trading cues.

And their metric of choice is the U.S. dollar’s trading action. That sounds logical as well. The U.S. dollar and gold are both currencies, mediums of exchange. Though gold isn’t used much as a currency today in practical terms, it played that role exceedingly well for millennia all over the world. So, it’s intuitive to view the dollar gold price as an exchange rate, much like the dollar-euro and dollar-yen prices widely quoted.

So regardless of the U.S. dollar’s drivers, gold-futures speculators tend to do the opposite when sizable intraday moves arise. When the USDX surges they generally sell gold futures, driving its price lower. And often the reason the dollar rallies sharply is some hawkish-sounding news that suggests the Fed may have to speed up the pace of this rate-hike cycle. So gold is effectively hostage to this rate-hike outlook.

Thus, gold prices and USDX levels are generally negatively correlated. There are certainly exceptions that occur, because gold-futures trading isn’t gold’s only primary driver. When investors are flooding back into gold, their vastly-larger pools of capital easily drown out whatever the futures speculators are up to. So, gold most often disconnects from the dollar when investors are buying or selling gold at high rates.

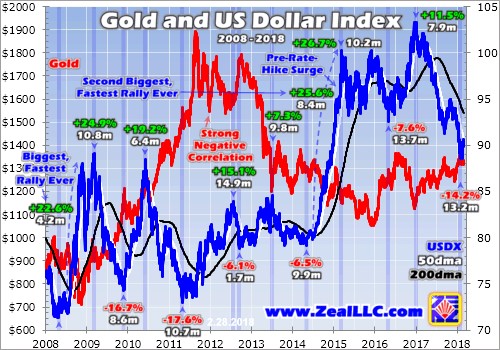

This next chart compares gold and the USDX over the past decade or so, since that stock-panic year in 2008. The dollar’s meanderings are divided between major uplegs and downlegs, with their starting and ending points highlighted with light-blue lines. The USDX’s gain or loss in each major swing is noted, along with the time it took. From a major-dollar-swing perspective, gold is definitely negatively correlated.

(Click to enlarge)

For the most part, gold rallies when the dollar weakens and vice versa. Over most of these spans with major dollar rallies or selloffs, gold usually did the opposite. That’s this dollar-driving-gold dynamic in action. The red gold line often roughly inversely mirrors the price action of the blue USDX line. This has even happened at times when investors are very active in gold, proving how influential dollar levels are on gold.

As a professional speculator and newsletter guy, I’m blessed to watch the market action in real-time all day every day. After decades of doing that, it’s amazing how often sizable gold action on daily, weekly, monthly, and even longer scales simply does the opposite of what’s going on in the US dollar. The lion’s share of the times gold is moving, it can be explained by a contrary USDX move. The dollar is a big gold driver!

Naturally the gold-futures speculators fueling most of gold’s minute-by-minute price action not only watch US-dollar futures, but understand what motivates the dollar traders to buy and sell. With this dynamic so deeply ingrained for so many years now, the gold-futures guys now watch for the same catalysts implying more or less future Fed rate hikes. So they buy gold on Fed-dovish catalysts, and sell it on Fed-hawkish ones.

The gold-futures speculators are zeroing in on what is going to motivate dollar traders to buy and sell and acting on it immediately. Doing this instead of waiting for the dollar guys before reacting really seems to intensify the gold-price impact from news that could alter the FFR’s likely path. That effectively slaves the gold price to Fed-rate-hike projections, unless investment capital flows overshadow gold-futures trading.

And not surprisingly when a Fed-rate-hike cycle is actively underway, traders are much more focused on its probable trajectory. That makes those news catalysts that can alter Fed-rate-hike expectations way more potent in driving gold price action. When futures speculators see something they perceive as hawkish, they are going to aggressively buy the US dollar while aggressively selling gold. This is really frustrating.

Just as Fed-rate-hike cycles haven’t proven bullish historically for the USDX, they haven’t proven bearish for gold! I’ve done a lot of research work on this front, starting back in late 2015. Prior to the Fed’s initial hike of this 12th cycle, gold was hammered on enormous selling. The gold-futures speculators traded as if they were utterly convinced higher yields would greatly retard gold demand and weigh heavily on its price.

Related: Europe’s Newest Tax Haven

Trading theses are fine, but they should always be backchecked with historical data to see if they have proven valid. So, I looked at gold’s performance during every Fed-rate-hike cycle of the modern era since 1971. I last updated this important research about a year ago. Contrary to popular belief, gold has actually thrived during Fed-rate-hike cycles! Similar to the USDX, there’s a persistent myth that the opposite is true.

During the exact spans of all 11 previous hiking cycles since 1971, gold averaged strong gains of 26.9 percent. That’s nearly an order of magnitude greater than the stock markets’ gains in the same spans. Gold rose during 6 of these cycles and slumped during 5. Its average gains in the majority where gold rallied were a whopping 61.0 percent! And its average losses in the minority where it fell were an asymmetrically-small 13.9 percent.

Gold tended to perform best if it entered a Fed-rate-hike cycle relatively low compared to recent years and the Fed hiking was gradual. Both have certainly proven true in our current 12th cycle, where gold has powered 24.2 percent higher since the day before the initial hike! Go back and read nearly any commentary on gold in December 2015 other than my super-contrary bullish forecasts, and everyone was wildly bearish.

During that 11th rate-hike cycle between June 2004 to June 2006 where the Fed hiked 17 times in a row for 425 basis points, gold actually surged 49.6 percent higher in its exact span! That was despite the Fed more than quintupling its FFR target to 5.25 percent, far more extreme in both magnitude and level compared to the current 12th rate-hike cycle. Fed rate hikes certainly haven’t crushed gold at all, history has proven the opposite!

So next week or next month when some news inevitably arises that is interpreted as threatening four more Fed rate hikes in 2018 instead of three, don’t worry. When futures speculators predictably react in their usual historically-wrong kneejerk fashion, relax. They will bid up the dollar hard for a short spell, and hammer gold. We’ve seen this boring old movie play out countless times, and it’s not worth fretting about.

Instead of freaking out about largely-meaningless short-term market noise, keep the big picture in focus. Gold has powered 26.9 percent higher on average in all 11 past modern Fed-rate-hike cycles. It blasted up 49.6 percent in the last monster 425bp one in the mid-2000s when the USDX retreated 3.8 percent. And gold is still up 24.2 percent cycle-to-date in our current 12th cycle, while the USDX has fallen a rather-sharp 7.7 percent so far.

For all investors and speculators, it’s absolutely imperative to understand the real relationships between Fed hikes, the dollar, and gold. Actual Fed rate hikes haven’t proven bullish for the dollar nor bearish for gold for decades! Futures speculators aggressively trade as if their opposing mythology on this was true, which can move the dollar and gold on Fed-rate-hike expectations. But these emotional anomalies are short-lived.

In our current Fed-rate-hike cycle, the USDX may very well keep grinding lower until it reaches its strong secular support down in the low 80s. And before the FOMC finishes hiking, gold will almost certainly see cycle gains well eclipsing that 61.0 percent historical average in Fed-rate-hike cycles where it rallies. So being long gold and the stocks of its miners which leverage its gains are great trades while the Fed keeps hiking.

The bottom line is Fed rate hikes haven’t proven bullish for the U.S. dollar nor bearish for gold, despite the widespread belief. History has actually shown just the opposite over recent decades. Gold tends to rally during Fed-rate-hike cycles, while the dollar tends to slump. Futures speculators seem to be willingly ignorant of this strong historical precedent, deluding themselves with groupthink into believing the opposite.

So whenever news arises that these guys interpret as supporting more Fed rate hikes faster, they are quick to aggressively buy the dollar while dumping gold. Their collective trading action temporarily bends reality to their fervently-held myth. But these short-term futures-driven anomalies are nothing to fear, as they soon unwind. If you want to thrive in this Fed-rate-hike cycle, bet with hard history instead of herd sentiment.

By Adam Hamilton

More Top Reads From Safehaven.com: