Lumber prices have skyrocketed in the past 12 months, causing the average price of both new and existing single-family homes to increase. Until now. That bubble appears to have burst, finally.

Mandated lockdowns caused lumber sawmills to halt production while at the same time many Americans, trapped inside due to the stay-at-home orders, rushed to the stores to buy lumber for projects to kill the time.

Those two related things caused lumber inventory to plummet.

As a result, lumber prices have skyrocketed more than 300% since April last year, leading the National Association of Homebuilders to report that the lumber shortage has added at least $36,000 to the cost of a new home.

They estimated that the cost of lumber for building a home hit $70,000, nearly double the cost of building the exact same home last March.

Also, the median sale price of existing homes surged by a record 17% to $329,100 — the highest since the National Association of Realtors began tracking prices in 1999.

However, many experts have been forecasting the end of lumber’s time at the top of the commodity’s price list, though, and they have now been vindicated.

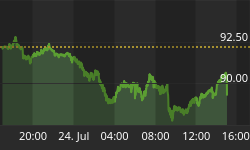

After reaching an all-time high of $1,711 per thousand board feet in early May, the cost of wood is now experiencing a fast descent.

Last week, the price fell some by $700, representing a drop of 41%. Still, even though lumber prices are in free fall, they’re still far above the futures prices of lumber from last March when it was $303.

Two factors initiated the price drop. First, with restrictions easing across the country, sawmills resumed their normal operations while lumber-hoarding DIYers shifted their money and time to travel and entertainment. However, it could still take several weeks for price reductions to take effect in retail home centers.

Dustin Jalbert, an analyst with Fastmarkets, told NPR that prices are probably not going to fall to the levels that they were before the pandemic.

Much like lumber, the prices of new and used cars increased in the last 12 months, as the shortage of microchips has forced many car manufacturers to severely slow production.

With the new vehicle inventory down 25% compared with this same time last year, customers turned to the used cars causing prices to increase 30% on average compared to the last year, and 17% just since January this year.

However, some are predicting that the used cars sector will see its own bubble burst soon enough. As used car prices are getting close to the new car prices, CarMax CEO William Nash believes that later this year the used car prices will fall. "I think we are getting close to that inflection point," he said.

Overall, major consumer prices rose 5% year over year in May, the fastest pace since August 2008, according to the new Labor Department report. Food prices are up 2.2% for the 12-month period, while the gasoline index is up 56.2% over the past year, part of an overall 28.5% increase in energy index.