Last year proved to be a gold speculator and investor’s dream after gold prices rallied hard to hit historical highs thanks to a perfect storm of a global pandemic, massive government stimulus packages, a weakening dollar and a stock market bull run that was finally running out of gas. The torrid rally represented the sharpest gain the metal has mustered in more than a decade.

Unfortunately, the rally has run out of steam, with gold prices pulling back sharply since its all-time high of $2,075 per ounce.

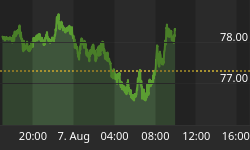

Gold futures have once again slumped below $1,800/oz., posting their biggest one-day loss in seven months on Thursday after the Federal Reserve sped up its expected pace of policy tightening.

On Wednesday, Fed Chairman Jerome Powell said during his post-decision press conference that rising inflation is due to mostly "transitory" factors, but also admitted that inflation may be more persistent than they currently expect. "If we see inflation moving materially above what we see as consistent to our goals and persistently so, the Fed would act to bring it down.’’

The markets did not like the Fed’s doublespeak, with the dollar rising but gold, commodities and stocks falling.

August Comex gold (XAUUSD:CUR) tumbled 4.1% to trade at $1,784/oz., which would represent the biggest one-day drop since last November according to FactSet data, while July silver(XAGUSD:CUR) fell 5.5% to $26.27/oz.

Not surprisingly, gold mining stocks have not been spared.

The VanEck Vectors Gold Miners ETF (GDX) fell 5.5% on Thursday and another 1.6% on Friday for a total 10.2% loss over the past five trading sessions. GDX has a -4.47% YTD return.

VanEck Vectors Junior Gold Miners ETF (GDXJ) lost 4.74% on Thursday’s session and 9.47% over the last five trading sessions. GDXJ is down 11.2% YTD.

This has come as a major disappointment for gold bulls, with some Wall Street hedge funds having been extremely bullish on gold, with some eyeing prices of $3,000 and even $5,000 per ounce.

Summers are usually a quiet time for the markets, especially for gold. But some Wall Street punters such as OANDA senior market analyst Edward Moya have been saying this time it could be different. Moya previously said this volatility could be excellent news as the precious metal gears up to make a run towards $1,900.

But now he has been forced to change his tune:

"The Fed's hawkish pivot is a major buzzkill for gold bulls that could see some momentum selling over the short-term. Short-term Treasury yields will continue to rise and that should provide some underlying support for the dollar, which will keep commodities vulnerable."

At this juncture, we believe the gold outlook is a mixed bag. Here’s why:

Vaccine optimism

On the opposite side of the spectrum, a successful vaccination campaign and reopening of the global economy is bearish for gold.

A big reason why the gold bears have lately been gaining an upperhand is due to growing optimism that the global Covid-19 vaccine rollout will help many economies return to a semblance of normalcy sooner than expected.

For instance, in its April update of the World Economic Outlook, the IMF upgraded its forecast for global GDP growth for 2021 and 2022 to +6% and +4.4%, respectively, thanks mainly to the country's the countrys’ swift vaccine rollout and hefty stimulus packages. That is a big turnaround from a contraction of 3.3% in 2020 when the world was hit by the pandemic.

The United States has so far unveiled the world’s fastest vaccine rollout as per Bloomberg, placing itself in a good position for a full re-opening of the economy.

Generally, the global rollout is progressing at an adequate clip despite the presence of numerous hiccups such as a major second wave in India and Brazil.

With the pandemic risk becoming increasingly subdued, safe haven investors have been losing interest in gold.

Sluggish labor markets

Back in March, the Fed set an inflation target at 2.4% with the hopes that an overheated economy would ultimately drive workers back into the labor market. With the U.S. returning to full employment, the Fed expected that at that point we would resolve the rampant shortages and supply chain issues thus helping the so-called transitory price hikes to normalize.

But as things stand right now, it could be another 12-14 more months before we come anywhere near full employment, meaning inflation will run hotter for longer than we anticipated.

An environment of "stagflation" tends to favor safe havens such as gold and silver.