Briefly: Gold is likely to plunge below $1,000 this year and we’ve been writing about it for months. This article provides a list of critical long-term factors that one should be aware of if they want to invest in or trade gold, silver, and/or mining stocks. We include links to our previous premium analyses and we just made these analyses available to everyone.

But first, a quick short-term update.

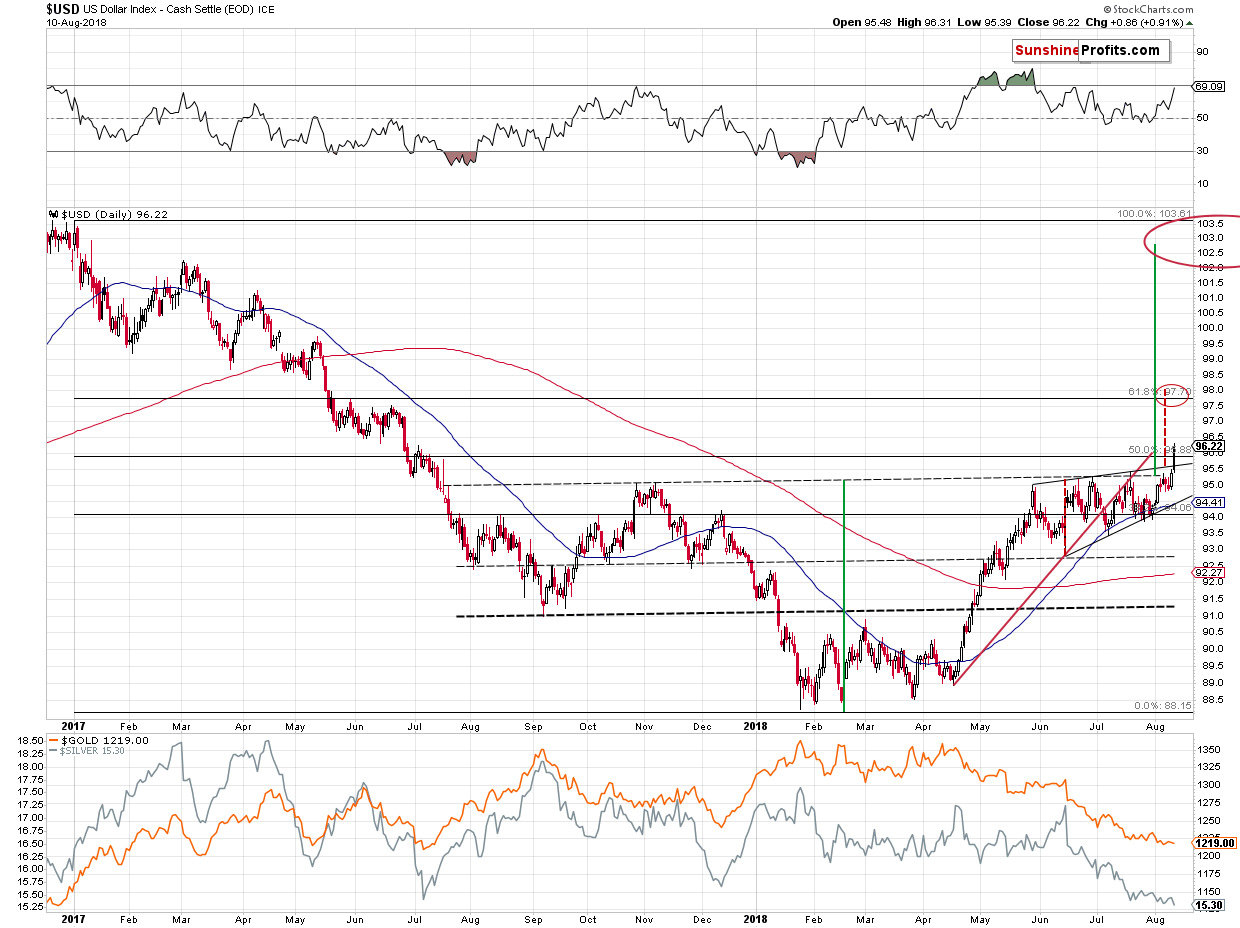

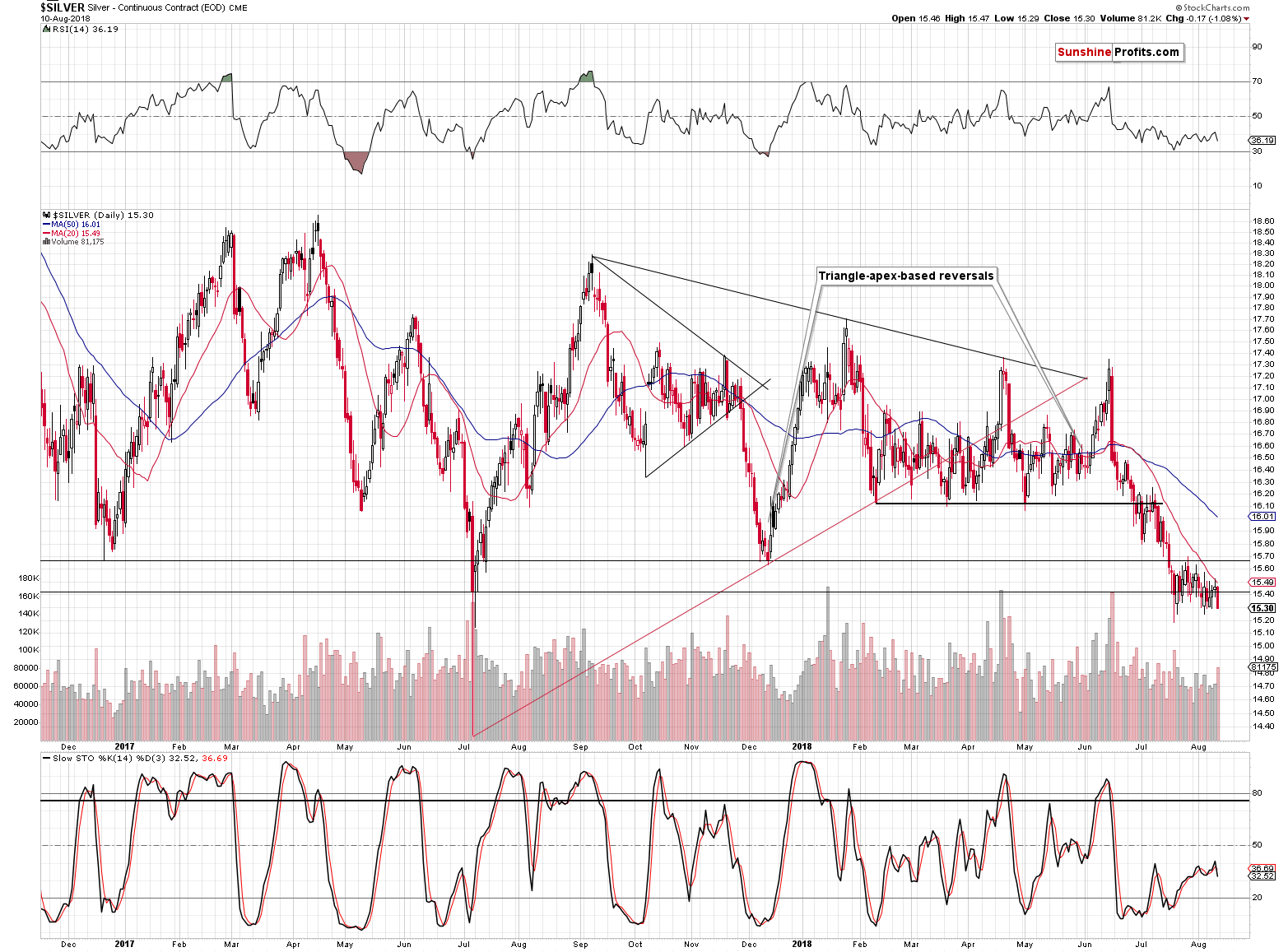

There were a few important technical details that took place on Friday that confirmed what we had written previously. The USD Index broke above the rising wedge pattern and the medium-term reverse head-and-shoulders pattern, while silver closed (the daily and weekly close) below its July 2017 lows.

(Click to enlarge)

That’s a major breakout in the USDX and its likely to be followed by much higher price levels. The implications for the precious metals market are clearly bearish.

(Click to enlarge)

The same goes for silver’s crystal-clear breakdown in terms of weekly closing prices and another breakdown in daily prices. The volume on which silver declined was big on a relative basis and the white metal continues to move lower in today’s pre-market trading, which means that the breakdown is very likely to be confirmed. The implications are already bearish.

But, the overall implications were extremely bearish previously, so nothing really changed. Consequently, our previous comments and the current investment / trading positions remain up-to-date. Therefore, instead of repeating what we wrote on Friday, we decided to do something different today. Related: Google Accepts Chinese Censorship For Big Payout

The inspiration came after explaining the USD Index’s outlook along with some PM details. We were asked: “So is there anything else pointing to lower PM prices other than the USD Index?” Our initial reply was that there were multiple very important reasons but for some reason we couldn’t recall more than a few of them. It turns out that when so many things are explained and written down, they seem obvious and they are removed from the active part of one’s memory (for the same reason, if you can’t sleep at night because you have so many things on your mind, writing them down to deal with them on the next day actually helps).

But, that’s not how it should be in the case of one’s investments. The prudent investor should always be aware of what the situation is along with the reasons for it being this way. Unless it’s clear what justifies a certain opinion, it might be an emotional view, not a logical justification. So, why do we really think that the precious metals sector is about to decline? There are indeed numerous important reasons and we gathered them in the following list. We discussed some of them recently, but some of them seemed “too obvious” to discuss them in the past few weeks. In some cases, we haven’t discussed a given issue in months.

Key Factors for Gold & Silver Investors

In today’s analysis, we will provide a list of key factors that are likely to result in lower precious metals prices in the coming weeks and months. Naturally, we’ll not discuss them from scratch, as that would imply writing a book. Instead, we will provide you with a list of links that includes the most important details that are important from today’s point of view and we’ll provide very brief summaries of each point. Let’s start with the big picture.

- The shape of gold’s decline since 2011 is very similar to the way in which gold declined in the 1980s. This is a huge deal, because it implies that gold is likely to move to new lows. We commented on it in great detail in March 2018 and these comments remain up-to-date also today.

Another extremely important factor for the precious metals market is the long-term situation in the USD Index. And by “long-term situation,” we don’t just mean the last couple of years. There’s a massive and classically confirmed breakout in the case of the USD Index that’s perfectly visible on the 47-year chart and it has profound implications for both the USD Index, and the entire precious metals sector, because it suggests further rallies in the USD Index and some kind of major turnaround in the final part of 2018.

We covered both issues: gold’s 1980-2011 link and the USD’s long-term breakout on March 6, 2018.

- The next very important issue that remains in place is the link between the 2012-2013 decline and the current move lower in gold. On July 2, 2018, we explained that June 2018 appeared analogous to February 2013. We wrote that gold was likely to rally for about 2 weeks in the first half of July and then to decline, with the powerful decline taking place in August. That’s exactly what has happened so far and these comments definitely remain up-to-date.

- On January 29, 2018, we discussed the extreme signs from the volume readings in terms of weeks. On February 1st, 2018, we commented on the record-breaking monthly volume levels. The implications are bearish in both cases and they are of a medium-term nature. Consequently, they may contribute to lower gold prices in the future.

- Speaking of key analogies, let’s not forget the oddly clear analogy in silver between 2008 and the last few years. The analogy is not present in terms of time, but it’s shockingly accurate in terms of prices. The price levels to which the white metal rallied and to which it declined in 2008 are remarkably similar to where it has moved since early 2016. The implications are very bearish. You can read the details in our April 28, 2017 analysis and you will find the updated version of it in our February 26, 2018 commentary. The latter also includes a long-term analysis of the HUI Index and the HUI to gold and HUI to S&P 500 ratios.

- Since we’re talking about ratios, we absolutely have to address the gold to silver ratio - the key ratio in the precious metals sector. You have probably read numerous analyses about the ratio reaching its long-term resistance at about 80. Well, there is some truth to it, but all these analyses made this level seem like some ultimate go-to point. It’s not. The real long-term resistance in the gold to silver ratio is at about 100. Not only does it appear much rounder (it may appear surprising that it’s important but round numbers tend to carry more weight, technically speaking), but it’s actually the level at which the ratio really reversed from the long-term point of view. It turns out that from the very long-term perspective, the 80 level is just a local top and the real resistance is higher. You will find more details on the gold to silver ratio in our January 23, 2018 analysis. This article also includes important comments on the gold to S&P 500 ratio.

- The thing that doesn’t point to any specific price or time target, but that remains to be an important bearish factor is the way gold reacted to very positive fundamental news this year and in the previous years. The point is that it didn’t. Sure, there were some short-term rallies, a few of them even got investors excited, but none of them stood the test of time. No single fundamental news managed to trigger gold’s rally above the $1,350 -$1,450 barrier. We had Russia taking over Crimea, we had trade wars, we had nuclear threats regarding North Korea and multiple other threats. Gold should have rallied on just one of them, not to mention all of them taking place over the years. It didn’t, which shows that this market is not ready to rally just yet - it needs to really bottom first. This is connected with one of the questions that we are often asked - “What needs to happen for gold to decline?” The answer is that absolutely nothing needs to happen and you can find the detailed explanation in our April 3, 2018 analysis.

- If you’ve been following our analyses for some time and made a lot of money this year, you know that technicals matter a lot. But if you haven’t, you might be wondering why one should care about all this “chart voodoo” instead of just “looking at the real world” - gold’s demand and supply analysis, interest rates, geopolitical situation, and so on. The answer is that technical analysis of the precious metals market is clearly justified from the fundamental point of view. Yes, that’s right. Fundamental analysis on its own points to the need to use technical means to truly gain the edge in the case of precious metals investment and trading. You can read more in our April 27, 2018 analysis.

- The important part of the entire analysis is the currency sector. One thing that theoretically should drive currency prices are the interest rates. In practice, the reaction can be delayed. We discussed it in detail in our October 12, 2017 analysis. The bottom line is that after a few rate hikes, the USD Index was likely to start a powerful rally that would last for about a year or so. The rally started in early 2018, so it seems that we have more room for higher USDX values in the following months. This has bearish implications for the precious metals prices. The technical details definitely support this scenario and you can find more medium-term details in our April 30, 2018 analysis. We covered the key technical development of long-term significance in the first point of this list, though.

- Apart from the USD Index itself, one should be concerned with its part that is particularly connected with the price of gold - the Japanese yen. It’s after a major breakdown, which has profoundly bearish implications for the PM market. You will find details on the yen in our July 13, 2018 analysis.

- There’s more to the Japanese implications than just the above - the Nikkei 225 Index is also quite significantly correlated with gold. The correlation is negative. While correlation does not necessarily imply causation, we might still view moves in the Japanese stock market as a kind of indication of what’s likely to happen in the PMs. The link is of a medium-term nature and doesn’t necessarily work in the short run. It currently continues to imply higher Nikkei values and lower gold prices. You will find more details in our October 16, 2017 analysis.

Now, moving to the critical questions: When and at what price is gold likely to bottom?

You will find the best explanation of the up-to-date (as of August 13, 2018) gold’s price and time target in our January 22, 2018 analysis . The $890 / late-Sep - early-Oct target is marked with the red ellipse and if you ever wonder if this target is up-to-date, please take a look at gold’s long-term chart in one of the recent analyses - the up-to-date price-time combination will be marked with a red ellipse. Of course, if there are any major changes, we’ll comment on that in addition to making changes on the chart.

Related: Baltics Want to Pull The Plug On Russian Power

And as far as the most recent price developments are concerned, we can say the following regarding (please use the links to access the details):

- the analogies in the USD Index and its outlook

- the breakdowns in silver and gold stocks

Moreover, we prepared a list of “boomerang questions” along with our detailed replies (in the linked analyses):

- Did gold form a U-shaped bottom from mid-2013 to early 2018? No - there was no breakout above the key resistance, so there is no U-shaped bottom pattern to speak of yet. You will find details in our February 9, 2018 analysis.

- Are we seeing a reversal head-and-shoulders pattern in gold? Shouldn’t we buy based on it? No pattern is important until it is completed and analysts who make calls based on incomplete patterns without a good reason are making a serious logical mistake (they might actually be gold promoters, not analysts). You have been warned. You will find details in our September 11, 2017 analysis.

- S. stocks are extremely overbought and they are about to plunge - and if they do so, gold will soar! No, it’s not likely to happen. To clarify – while stocks could decline, one shouldn’t bet on any meaningful rally in gold just because of that. You will find details in our January 31, 2018 analysis.

- But the CoT report! - This legendary CoT report was very useful before 2010 (especially before the 2008 slide) but a lot has changed since that time. It’s now a short- to medium-term signal with efficiency a bit worse than the RSI indicator (the latter provides more signals). The RSI can work based on the weekly prices and can provide more long-term oriented signals, but the CoT numbers don’t have this option. You will find the details regarding the limited CoT efficiency in the case of big price moves in our July 25, 2018 analysis.

- Right – the RSI – it’s close to 30 in gold, so shouldn’t gold rally? Not if gold is in a medium-term decline – and it is. You will find the details regarding the limited usefulness of the RSI indicator in our July 16, 2018 analysis. Interestingly, when we wrote the above the RSI was close to 30 and gold was at about $1,244. Less than a month later, at the moment of writing these words, gold is at $1,203. It wasn’t so crazy to be shorting gold back then after all – it was profitable.

The reason behind the limited usefulness of the CoT signals and the ones coming from the RSI is also the reason why many short-term- and even some medium-term oriented techniques are likely to provide false signals at this time. The current and upcoming decline is a huge, long-term development and it’s not likely to be stopped by short-term factors. Unless one looks at the really big picture (we provided multiple links above to make it easier), there’s no difference between the current decline and the December 2017 downswing or the July 2017 one. Therefore, applying the same techniques that would have been useful back then seems to make sense. But there are so many signs that point to a huge move lower that it’s not correct to compare the current slide with the previous medium- or short-term slides. It’s not going to work because that means using a wrong tool to certain job. If you put a big truck (significant barrier) in front of a speeding motorcycle, it’s very likely to stop the motorcycle (a short-term price move). But, if you put the big truck in front of a train that goes at its full speed (big, long-term price move), it won’t do much. The train will go right through the truck without stopping. The key is knowing if the price move that one is looking at is a motorcycle or a train and the point of this quite significant commentary is to show that the current decline in the precious metals market really is the latter.

Summary

Summing up, there are multiple very meaningful reasons due to which the precious metals sector is likely to move lower in the following weeks and months. The USD’s major breakout and the breakdowns in the precious metals sector serve as confirmations that a big slide in the PMs is already underway. In other words, it seems that our sizable profits on the short positions are going to become even bigger shortly. We may have a local bottom later this month, though, and we’ll our subscribers informed regarding the possibility of seeing a bigger turnaround.

Does the above make us perma-bears? Absolutely not. We’re long-term “gold and silver bulls” who simply think that there will be a much better opportunity to enter the market than the current situation. Consequently, we are not in the precious metals market at this time with the long-term investment capital (you can read what we mean by this kind of capital and learn more about our approach in our report on gold portfolio structuring), but we are waiting for the opportunity to enter it once again, as we think that fundamentals and the very long-term trend favor MUCH higher precious metals prices. The odds are, however, that we’re going to see a big price slide first.

By Przemyslaw Radomski via Sunshine Profits

More Top Reads From Safehaven.com