It’s been a mixed bag for commodities, and it’s mostly been negative, with oil and gas and agriculture taking huge hits from the pandemic, and gold only humbly rallying on its safe haven laurels, while battery metals can’t catch a break despite production shut-ins.

Overall, the month ended on a sour note, more than anything dragged down by West Texas Intermediate (WTI) oil prices going into negative territory briefly.

For oil, it’s about crippling demand amid a major supply glut that has everyone scrambling for storage, while for agriculture, it’s about major supply chain disruptions.

Last month, the Bloomberg Commodity Index hit its lowest level ever, and for this year, it’s down 25.7%, and on the month, it’s down about 1.6%.

For oil, the June WTI contract settled at $18.84 on Thursday, down 8%. But gasoline futures were up on the month by 22%, likely on hopes of a summer driving season that may or may not happen.

Prices for battery metals such as lithium, cobalt and graphite are taking a hit amid the pandemic, which is crushing demand for EVs and other battery products. And predictions are taking cues from China, where giant Tianqi Lithium’s sudden massive debt problem that’s leading it to try to dump assets to pay it down. Just five years ago, this company was scooping up every lithium-related asset it could get its hands on as Beijing pursued production dominance.

Cobalt supply is expected to fall by 7% in 2020 due COVI-19-related closures, suspensions and operational restrictions. Democratic Republic of Congo (DRC), the world’s biggest cobalt producer, saw exports fall 15% in Q1, while other closures out output cuts are coming out of Morocco, Madagascar and Canada. The shut-ins are doing nothing to boost cobalt prices, however. As of April 21, spot prices for cobalt remain unchanged month-on-month at $13.38/lb.

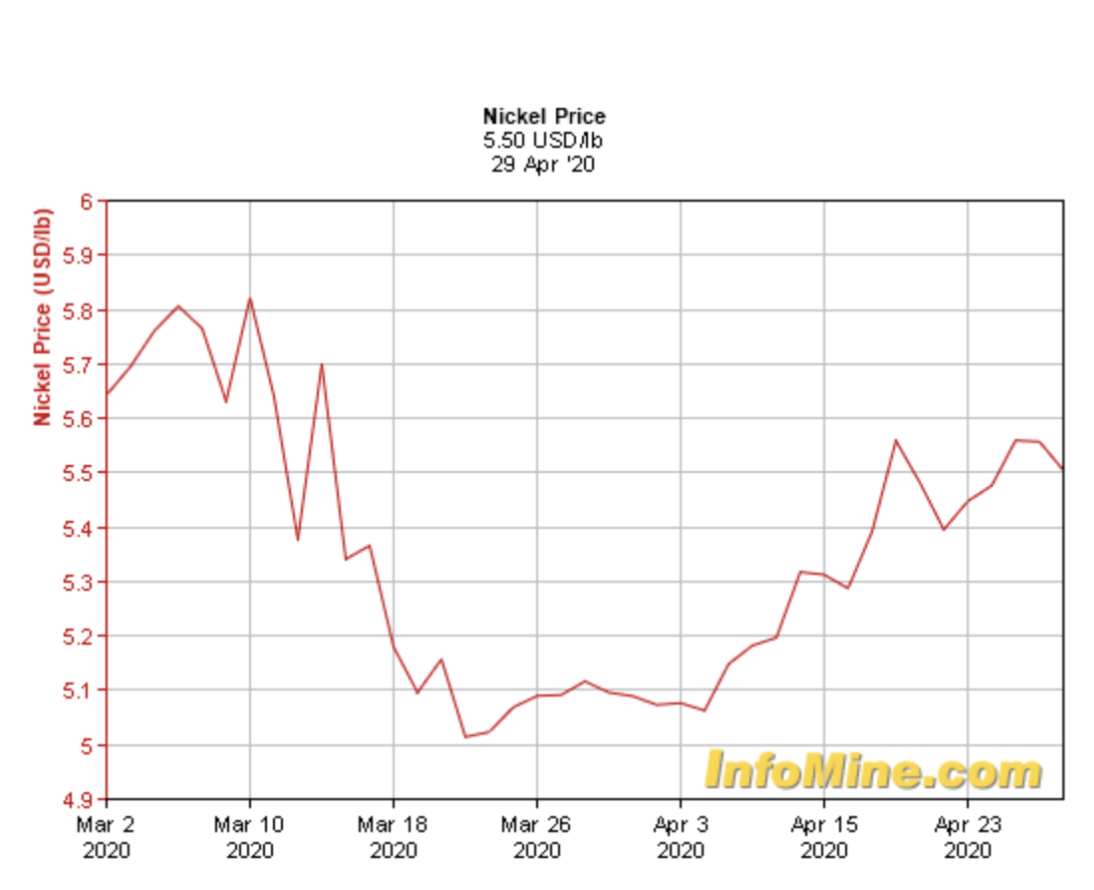

Nickel production is also down by around 30%, with the biggest miners halting some operations, but demand is dismally low. Nonetheless, nickel spot prices were up overall in April.

Analysts predict a surplus for this year of about 150,000 tons of surplus metal or 10% of global supply could accumulate.

While platinum, palladium and rhodium had been enjoying some very good times prior to the pandemic, they are losing some of their lustre because of the auto industry culling. Platinum, palladium and rhodium all have growing applications in the auto industry for catalytic converters. In Europe, where the industry is diesel-heavy, it’s more about platinum, while in the U.S. palladium rules the day.

Last week, gold hit $1,750 an ounce, but has since pared some of those gains, down to $1,677 on Thursday as investors looked at the prospects of economic reopenings, coupled with profit-taking from last week’s rally.

But a number of analysts think we’ll see the turning point because prices have been moving downward for 10 years already.

As John LaForge, head of real asset strategy at Wells Fargo Investment Institute, tells the New York Times, “What we’ve seen in 2020 is just an extension of what’s been happening over the last decade. We’ve gone through the crashing phase of commodities and now we’re probably where prices are pretty close to turning.”

By Tom Kool for Safehaven.com

More Top Reads From Safehaven.com: