On Friday the United States made good on its threat to ratchet up the trade war against China, after the two parties failed, after weeks of negotiations, to reach a deal.

The Trump administration hiked tariffs on $200 billion worth of Chinese imports to 25% from 10%, adding to the $50 billion in goods already being taxed at that level. The tariff hikes went into effect at midnight on Thursday.

The negotiations appeared to be going well up until a couple of days ago, when Treasury Secretary Steven Mnuchin and Trade Representative Robert Lighthizer accused the Chinese of reneging on earlier commitments.

Nobody outside the trade delegations knows what went on behind closed doors in Washington, but it appears to us that the American team just got played. Dealing with China, or other Asian nations for that matter, is different from negotiating with fellow North Americans, or Europeans. It’s important to come across as respectful, and calm. Shrewdness is valued. Bluster and strong-arming are frowned upon.

Chinese negotiators will seldom agree to the first draft of a deal; the more common practice is to go back on what was discussed and amend the agreement, knowing full well that the other side won’t accept. But that’s ok. Like a chess game, the Chinese delegation was likely awaiting the next US move. Instead, the American delegation slammed its fist on the chess board, immediately ending the game.

Now comes the punishment for not agreeing quickly enough to US demands. But anyone who knows Asian culture, understands that “losing face” is a big deal. They can’t, and won’t, give in to threats, for this shows weakness. Instead China’s commerce ministry said it would impose “necessary countermeasures” without giving any details.

President Trump said he’s in no rush to reach a deal - although in reality, his deadline is the 2020 presidential campaign - but he also remarked “the process has begun” to slap 25% tariffs on the remaining $325 billion in goods from China – which would raise the total value of Chinese goods being penalized, to $540 billion!

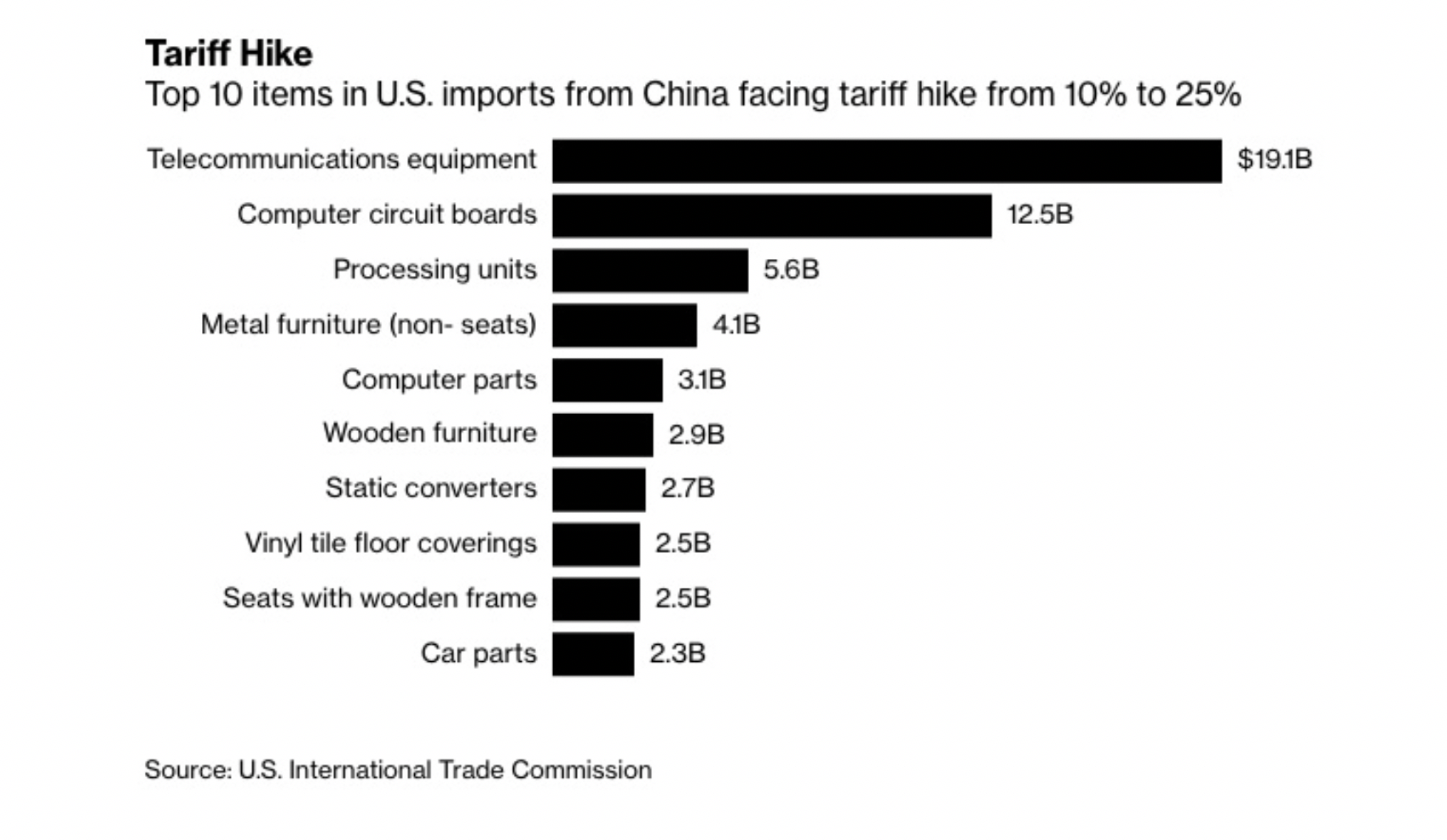

(Click to enlarge)

It’s worth noting that, with $250 billion of $540 billion worth of total Chinese imports to the US now under tariff, the States has a lot more room to the negotiate than China, which has levied import duties on all but $10 billion of the total $120 billion worth of US exports to the country.

So far this trade dispute has not seriously hurt either nation - although going by GDP numbers, the US is winning (agriculture, tech and automobiles are most affected).

The US Gross Domestic Product is at a healthy 3.2%, inflation is under 2%, the number of jobless is at a record low, and wages are even rising. China, on the other hand, is still bumping along at 6.4% GDP growth in the first quarter, the same as the last three months of 2018.

(Click to enlarge)

The bilateral trade deficit - something Trump has railed against for years - is narrowing, due to US businesses and consumers buying less from China and exporting more. In November 2018, the latest month available, the trade deficit fell US$2.8 billion to $35.4 billion, a fall of 7.3%, South China Morning Post reported.

Trade figures released on Jan. 14 showed China’s December exports to the US slowed to $221.24 billion, 4.4% less than December 2017.

“We find strong evidence that the 25 percent tariff on US$50 billion of imports from China [imposed in July and August last year] is having a significant negative impact on prices and volumes,” the Hong Kong-based news outlet quoted the Institute of International Finance, in an analysis of the tariffs’ impact.

US negotiators shouldn’t feel too emboldened by those figures, however. The China delegation has plenty of ammunition to fire at the US team should negotiations continue to stall. We know that Beijing must retaliate, in order to save face. Light punishments could include selling some US Treasuries, not participating in future US debt sales, devaluing the yuan, in order to make exports cheaper and entice US consumers to buy more Chinese products, or stop buying US soybeans, the US leading export to China.

All this is possible and will make stock markets roil, but we at Ahead of the Herd are thinking further ahead. We wonder what could happen if the aggro between China and the US escalates, and the two sides start looking at sectors to embargo.

This article looks at two of America’s most import-dependent commodities - rare earths and lithium - to get a sense of what could happen if China, due to the trade war, stops supplying US companies with these crucial technology metals.

Two aces in the hole

Most people don’t know it, but the US is dependent on foreign countries for over 20 critical metals, including battery metals used in electronic devices like cell phones and electric vehicles.

Without a reliable supply chain, a country must depend on outsiders. This gives foreign suppliers incredible leverage over the United States. There is always the possibility of slowed flows or bans on strategic materials, due to politics or trade disputes, such as the ongoing trade war with China.

If China were to suddenly refuse the sale of any of the 20 out of 23 metals the US deems critical to the economy or defense of the nation, the US economy would be in serious trouble.

The Trump administration recognized this when the president issued an executive order in December 2017, instructing his people to devise “a strategy to reduce the Nation’s reliance on critical minerals” that are largely imported.

“The United States must not remain reliant on foreign competitors like Russia and China for the critical minerals needed to keep our economy and our country safe,” Reuters quoted President Trump saying. The directive was a response to the USGS’ first assessment of US critical minerals since 1973. Its report concluded that the US relies on China for sourcing 20 out of the 23 minerals deemed critical for US national security and the economy.

Included on that list are the building blocks of the new electrified economy, including lithium and rare earths. China has a stranglehold on both of these metals, meaning it can use them as a cudgel in trade talks with the United States.

Rare earths

The United States was once the largest producer of permanent magnets, used in dozens of industrial applications including electric vehicle motors and for wind turbines. Permanent magnets are built from the rare earths neodymium, praseodymium and dysprosium.

That was until the mid-1990s, when the US ceded control to China, which now has a monopoly, either mining or processing over 90% of the 17 elements on the Periodic Table, used in everything from smartphones to weaponry.

Without a domestic supply, the US must rely on Chinese rare earths and technology to build “made in America” military and space equipment. (For the fascinating story on how this happened, read Magnequench Has Left the Building and How the US Lost the Plot on Rare Earths)

For example, permanent magnets made from Chinese rare earths are used in the Joint Strike Fighter, the Pentagon’s answer to a one-size-fits-all warplane. Rare earth metals, alloys and magnets needed by US defense contractors come either directly or indirectly from mostly China. Related: Stocks Slip As Trump Ramps Up Trade Deal Rhetoric

The US doesn’t want to do that, but China has pretty much cornered the market on rare earths. Sure, there are a handful of other countries that mine and produce them, but the process is so difficult, costly and harmful to the environment, if done wrongly, that few attempt it.

The only US rare earths mine, Mountain Pass in California, was sold a few years ago to a US-led consortium. The rare earth concentrate is shipped to China for processing by the Chinese company in the group.

The other significant non-Chinese producer, Australia’s Lynas, had its refinery in Malaysia shut down; it will not re-open until Lynas removes its radioactive waste.

For years, China has been the world’s largest rare earths exporter, shipping over 53,000 tonnes in 2018, 4% more than 2017.

It’s all part of China’s plan to produce more rare earths for internal consumption than for export, which is in line with the country’s ambitions in the global clean energy trade. China is already the world’s largest solar power producer and sells the most electric vehicles. By 2020, the Chinese government wants its battery makers to double their capacity (BYD is the largest electric vehicle battery company in the world) and start investing in production facilities overseas.

Here’s Scientific American on how China is investing in rare earths in order to monopolize clean energy, at the expense of non-Chinese companies and the US:

Already, more than 80 percent of the world’s rare-earth elements are extracted in China. But the Chinese government isn’t done—they have higher ambitions for REEs. By 2020, China wants to increase domestic REE production by 15 percent annually while also decreasing the proportion of primary raw materials meant to be exported from 57 percent down to 30 percent. Beijing’s intention to control the outward flow of REEs would create bottlenecks limiting the ability of non-Chinese companies to manufacture their products outside of China.

While China has been barreling ahead in its quest to dominate REEs, the United States has only become more dependent on REE imports—rare earths were not mined at all in the U.S. in 2017, with China supplying 78 percent of imports in between 2013 and 2016. These elements are necessary to manufacture not only wind turbines and solar panels, but also cruise missiles and stealth aircrafts.

Molycorp get played

In 2009 the Chinese government imposed export controls on its rare earths, meaning a 40% drop in exports. Beijing said it had to implement quotas to protect the environment, but critics saw them as naked protectionism.

China was about to play Molycorp like an erhu, a Chinese violin.

A year later, an international incident sent rare earth oxide prices into the stratosphere. In September 2010 a Japanese naval vessel interdicted a Chinese fishing boat near the Senkaku Islands, which Japan and China both claim ownership of, and detained the captain. The Chinese decided to ban all rare earth exports to Japan, then an industrial powerhouse and China’s largest REE customer. The rare earths market panicked, and within months, all of the rare earth oxides gained in price.

The result was the re-opening of the Mountain Pass Mine, including a $130 million investment by Japanese conglomerate Sumitomo to upgrade the mine. By 2014 it was producing 4,700 tons of rare earths a year.

While the spike in rare earths prices was good for miners like Molycorp and the numerous exploration companies that sprang up in search for them, buyers of products made from rare earths balked and pressured governments to do something about it. The US, European Union and Japan brought a case to the World Trade Organization to try and settle the dispute and get China to lift the restrictions.

In 2015 it did, resulting in a torrent of Chinese rare earth exports into the market and the inevitable collapse in prices. The move caught Molycorp off-guard. The company had just spent over a billion dollars on another upgrade at Mountain Pass but within months, the company fell deeply in debt and went bankrupt.

The mine was put on care and maintenance and eventually sold at auction in the summer of 2017 for a shocking $20.5 million - a fraction of its previous worth. The new owner is MP Mine Operations LLC, an American-led consortium, with Chinese rare earths miner Leshan Shenghe Rare Earth Co. holding a minority interest. Mountain Pass currently ships rare earths concentrate for refining in China, although the owners say they plan to build processing capacity in the US. Related: Stocks Slip As Trump Ramps Up Trade Deal Rhetoric

At the time, China was using its rare earths monopoly to either choke or flood the market with rare earth oxides, as best benefited them. Now, imagine that Beijing decided to go for the jugular, and embargo rare earth oxides to the United States. All the rare earth end users - buyers of rare earth powders and metals used in high-tech applications such as smartphones, catalysts and LED screens - would be scrambling to find another source.

One key point: while the US is dependent on foreign suppliers of rare earths, it depends 100% on China for rare metals that have been processed into a final, usable form.

Victoria Bruce, the author of ‘Sellout: How Washington Gave Away America’s Technological Soul’ agrees that “China holds a secret weapon that could cripple us instantly. Let’s call it, Trade War Option “57 – 71”.

Bruce points to America’s military vulnerabilities, should China ever exercise its full power over the world’s rare earth elements. Here’s Victoria Bruce, writing a column in The Hill:

Rare earth metals are so critical and in so many defense components for guided missiles, smart bombs, targeting lasers, sonar, radar, night vision and high-temperature resistant metals for military jet engines, that if China cut us off, the U.S. could not replace or build most of our advanced weapon systems.

These materials are also found in smartphones, small electric motors, sensors and catalysts in automobiles, computers, commercial aircraft and most green technology. If China embargoed these materials the U.S. would be forced to shut down all or most of our nation’s technology manufacturing assembly lines.

This single category of imports, with a global resource value of about $3 billion, becomes an essential input to about $7 trillion in value-added goods on a global basis. The U.S. controls zero.

How did we get into this precarious position?

The most recent 2016 Government Accounting Office (GAO) report called China’s monopoly on rare earths a “bedrock national security issue,” and back in 2010, the GAO warned Congress that it could take up to 15 years for the U.S. to re-develop its own rare earth supply chain. Still, Congress failed to act.

In fact, Congress is taking action, though it’s too late to prevent any trade retaliation from China. Last year, an amendment to the National Defense Authorization Act (NDAA), that would facilitate streamlined permitting for critical and strategic minerals, passed the floor of the House of Representatives on a bipartisan vote of 229-183.

A press release from the Congressional Western Caucus revealed some interesting tidbits regarding US dependence on rare earth imports, including:

- The U.S. Department of Defense uses as much as 750,000 ton of minerals each year.

- A non-classified defense study recently found that failure to have a reliable supply chain for at least 16 of the 35 critical minerals has already caused significant weapon system production delays for the Department of Defense.

- According to the USGS, the gear of one U.S. Navy SEAL contains at least 23 mineral commodities, for which the United States relies on its imports.

A Chinese embargo on rare earths would be equally devastating to US industry, especially considering that their use in permanent magnets - necessary for electric vehicles and wind turbines, two of the most important technologies to wean Americans off of fossil fuels.

Among the US companies that would be most badly hurt either from export restrictions on rare earths or, outright bans, are Apple, Tesla, General Electric, Western Digital, Seagate and Cree, Inc.

An iPhone has nine of the 17 rare earth elements, such as lanthanum, found in the phone’s circuitry. Praseodymium and neodymium are in the ear buds, and rare earth elements are used to make the vivid colors that light up the phone’s LED screen.

Tesla’s Model X and Model 3 contained induction motors that did not require REEs, but the electric car maker has switched to a magnetic motor that uses neodymium in its Model 3 Long Range. Permanent magnets are also in the Nissan Leaf, Chevy Volt and BMW i3.

Demand for neodymium is so strong that in 2017 it outpaced supply by 10%.

Iconic American company General Electric is also beholden to rare earths, having gotten into the wind turbine market in a big way; GE is one of the world’s leading wind turbine suppliers at about 35,000 installed throughout the world. A typical wind turbine contains 350 kilograms of rare earths - primarily neodymium in the permanent magnets.

Finally, the neodymium-iron-boron magnet is an indispensable component for hard disk drives made by Western Digital and Seagate, the two main suppliers of HDDs. Praseodymium and erbium are also used to produce high-strength glass substrates, which optimize HDDs by improving their strength, chemical stability, and adhesion to a magnetic recording layer, Robert Castellano writes in Seeking Alpha. Cerium is employed as a polishing slurry in these glass disks, which are rapidly replacing aluminum disks.

“If a rare earth embargo were to be enacted, it would damage the competitiveness of U.S. companies,” Castellano concludes.

Lithium

According to the latest data from the USGS (United States Geological Survey), Australia cranked out 18,700 tonnes of lithium in 2017, with Chile coming close at 14,100 tonnes. Argentina was a distant third at 5,500 tonnes. The global market for lithium carbonate equivalent (LCE), as the mined product is measured, was 284,839 tonnes last year.

Up until a few years ago, there wasn’t much buyers’ competition for lithium, since it was a relatively small market that supplied lithium-ion batteries for electronics and power tools, mostly. Since the electric vehicle began to penetrate the internal combustion engine (ICE) car market, however, lithium has become the commodity to secure.

The International Energy Agency is predicting 24% growth in EVs every year until 2030. A Reuters analysis shows that automakers are planning on spending a combined $300 billion on electrification in the next decade. Related: Ireland Declares Climate Emergency

Volkswagen has said it will invest $800 million to construct a new electric vehicle – likely an SUV - at its plant in Chattanooga, Tennessee, starting in 2022.

GM is planning to sell its first EV this year, a 2020 Cadillac SUV, built in Spring Hill, Tennessee, in a move designed to challenge Tesla.

Meanwhile, more battery factories are being built, driven by the demand for lithium-ion batteries which is forecast to grow at a CAGR of over 13% by 2023.

There are 68 lithium-ion battery mega-factories already in the planning or construction stage.

In December Korean company SK Innovation said it will invest US$1.6 billion in the first electric vehicle battery plant in the United States, and is considering plowing an additional $5 billion into the project, planned for Jackson County, Georgia.

All of this explosive growth in battery plants and EVs will mean an unprecedented demand for the metals that go into them. This includes lithium cobalt, rare earths, graphite, nickel and copper.

So, the need for lithium is going through the roof, but the United States produces very little of the white metal.

The United States has just one lithium brine operation, the Silver Peak Mine in Nevada, but it’s been operating since the 1960s and its grades are said to be declining. Silver Peaks lithium is processed into lithium hydroxide and shipped to Asia.

China doesn’t produce much lithium either, about 3,000 tonnes compared to Australia’s 18,700 and Chile’s 14,100.

But China has made up for its lack of production capacity, by becoming the dominant player in processing the stuff, and by inking offtake agreements with overseas lithium miners.

In December, China’s Tianqi Lithium paid $4.1 billion to become the second-largest shareholder in SQM, Chile’s state lithium miner. The mega-deal effectively gives Tianqi control over half the world’s lithium production. The company already owned 51% of the largest hard-rock lithium mine, Greenbushes in Australia.

Chinese entities also control 60% of the world’s electric battery production, and the majority of lithium hydroxide, the high-grade lithium product that goes into Tesla’s lithium ion EV batteries, for example.

This has put the United States in a vulnerable position with respect to securing the lithium it will need for current and future electric vehicle production.

If China were to embargo all the lithium it mines or processes, destined for the United States, the result would be a serious setback for the country, just as it is taking steps to become a player in the lithium space.

The Diplomat reported in February that “Miners are pushing to sharply boost lithium output in the United States, as automakers in the world’s third biggest electric vehicle market are eager to cut their dependence on China for the critical battery ingredient and find more local sources.

“In North Carolina, Nevada and half a dozen other states, miners are working to revive the U.S. lithium industry, once the world’s largest until it fell off in the 1990s… Miners are betting U.S. expansion will pay off with orders from battery and vehicle manufacturers who are wary of relying too much on China, which is home to the majority of the world’s lithium processing facilities and sucks up most output of top producer Australia.”

And Reuters said in April that “U.S. government officials plan to meet with executives from automakers and lithium miners in early May as part of a first-of-its-kind effort to launch a national electric vehicle supply chain strategy, according to three sources familiar with the matter.

While Volkswagen AG, Tesla Inc and other electric-focused automakers and battery manufacturers are expanding in the United States and investing billions in the new technology, they are reliant on mineral imports without a major push to develop more domestic mines and processing facilities.

China already dominates the electric vehicle supply chain. It produces nearly two-thirds of the world’s lithium-ion batteries - compared to 5 percent for the United States - and controls most of the world’s lithium processing facilities, according to data from Benchmark Minerals Intelligence, which tracks prices for lithium and other commodities and is organizing the Washington, D.C., event.

U.S. imports of lithium have nearly doubled since 2014 due in part to rising demand from Tesla, SK Innovation Co and others building battery plants in the country, according to the U.S. Geological Survey.

Conclusion

The US government under the direction of Donald Trump has either blundered into a dangerous escalation of the trade war with China, by aggressively hiking tariffs on $200 billion worth of imports, or executed a brilliant offensive maneuver. We should know which very soon, when China announces its counter strike.

I say brilliant because, while the Trump administration’s brash negotiating style represents everything the Chinese dislike about America, it could get results. So far, as a negotiating tactic, the tariffs appear to be working in the US’s favor - just look at how well the economy is doing. We know the last relatively high GDP number reported is due, mostly, to the hundreds of billions of repatriated profits and share buybacks artificially goosing corporate earnings and the stock market. Along with a frenzy of debt-fueled consumer spending.

Meanwhile Chinese growth has flatlined and some believe the country is on the cusp of an ugly debt crisis. In these circumstances, it seems reasonable that the strong US economy could outlast China’s weakening one in a trade war.

The latter could embolden Trump to stick to his guns, but this article has been about China upping the ante. The secret weapon that could cripple the United States and force it into making a major concession(s), is an embargo on rare earths, lithium or both, plus other strategic metals the US doesn’t have.

We don’t know what will happen, but we do have a historical precedent. When China restricted rare earth exports in 2010 rare earth oxide prices went ballistic. Imagine what kind of an effect an embargo could have on prices…

By Richard Mills

More Top Reads From Safehaven.com: