Gold prices fell further on Wednesday as the US dollar strengthened, while a strong rebound in the nation’s manufacturing sector fuelled hopes of a recovery in the coronavirus-hit economy.

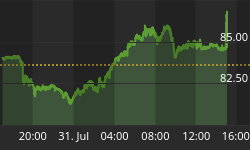

Spot gold fell 1.5% to $1,940.09 per ounce by 12:10 p.m. EDT despite hitting an intraday high of $1,973.25 earlier in the session. US gold futures also declined 1.5% to $1,948.00 per ounce on the Comex.

“The dollar index is rallying and the euro currency is selling off because the inflation data was negative in Europe,” Phillip Streible, chief market strategist at Blue Line Futures in Chicago, told Reuters.

On Tuesday, US manufacturing data showed activity accelerated to a near two-year high during the month of August, increasing optimism about an imminent recovery of the economy.

“As far as the economy is concerned, you are going to get this small bounce in economic data but you are not going to get any significant change in the economy what so ever, not for a long time,” Streible warned.

Bullion prices have surged 28% so far this year after the covid-19 pandemic upended economies, forcing global central banks to provide massive stimulus. The metal is widely considered a hedge against inflation and a safe-haven asset during times of economic uncertainty.

Although inflation could serve as an indicator of gold price movements, it may not be the case the other way round. Bank of England policymaker Gertjan Vlieghe warned UK lawmakers on Wednesday that it may be a “terrible idea” to look at gold prices as a predictor of inflation.

“If you look at previous episodes where the gold price is very elevated, you realize very quickly that gold is a terrible predictor of inflation,” Vlieghe said.

By Mining.com

More Top Reads From Safehaven.com: