A report by Fitch Solutions states that global gold mine production growth is expected to rebound in the coming years underpinned by higher gold prices and mergers between major mining firms.

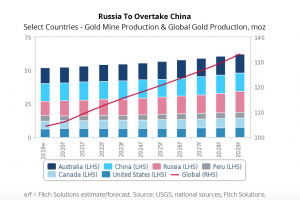

“We forecast global gold production to increase from 106moz in 2020 to 133moz by 2029, averaging 2.5% annual growth,” the document states. “This would be an acceleration from the average growth of just 1.2% over 2016-2019.”

Putting the spotlight on Russia, Fitch predicts that the eastern European giant is set to overtake China a decade from now, growing from 11.3moz in 2020 to 15.5moz in 2029. This would represent average annual growth of 3.7% during the period and would see Russia accounting for 11.6% of global output by 2029, compared to 10.6% in 2020.

In the market analyst’s view, Russia’s increase in gold production is being fueled by the ongoing and expanding US sanctions.

“The rising risk of Russian state banks being frozen out of dealing in dollar-denominated assets all together as bilateral relations remain strained is pushing the Russian central bank to increase its holdings of gold. As long as tensions with the US remain, domestic demand for gold is set to remain,” the report reads.

Australia, on the other hand, is set to see a 2.2% average annual growth production over the coming years but close to that of China, increasing from 11.7moz in 2020 to 14.2moz by 2029.

One of the major driving forces behind Australia’s growth is OZ Minerals’ development at its A$916-million Carrapateena copper-gold project, one of the largest mines being built in the country.

Carrapateena will be a 4.25mnt per annum copper-gold underground operation, with an estimated life of 20 years. Life-of-mine average annual production is expected to be 65kt of copper and 67koz of gold.

Both Russia and Australia represent important competitors for China when it comes to global production. Related: Copper Glut Continues To Grow

This is particularly the case taking into account that Chinese gold output has been challenged by strict environmental regulations on solid waste from gold prospecting, which have led to a wave of gold mine closures and output declines in major producing provinces, including Shandong, Jiangxi and Hunan.

At the same time, years of intensive gold mining has also resulted in falling reserves and production halts in several areas, including Qinghai and Gansu.

“We forecast China’s gold production to remain roughly stagnant during 2020-2029, with an average annual growth rate of 0.2%. This marks a notable slowdown compared with the average annual growth of 3.1% over the previous 10-year period,” Fitch’s report states. “Nonetheless, the country will remain the largest global producer of gold ore by a significant margin.”

The latter assertion is based on the fact that Chinese firms are ramping up investment in foreign gold mines, as the country’s gold demand growth far outpaces that of production.

“Key deals in recent years have included Chinese firm Shandong Gold’s purchase of a 50% stake in the Veladero mine in Argentina from Barrick Gold for $960 million. The firms will also work together on exploration activities in the area,” Fitch highlights. “In 2017, Zijin Mining produced 1.2moz of gold, reportedly accounting for 10.2% of China’s total output.”

By Mining.com

More Top Reads From Safehaven.com: